collated and compiled by the Collective on Geoeconomics

12/04/24

INTRODUCTION

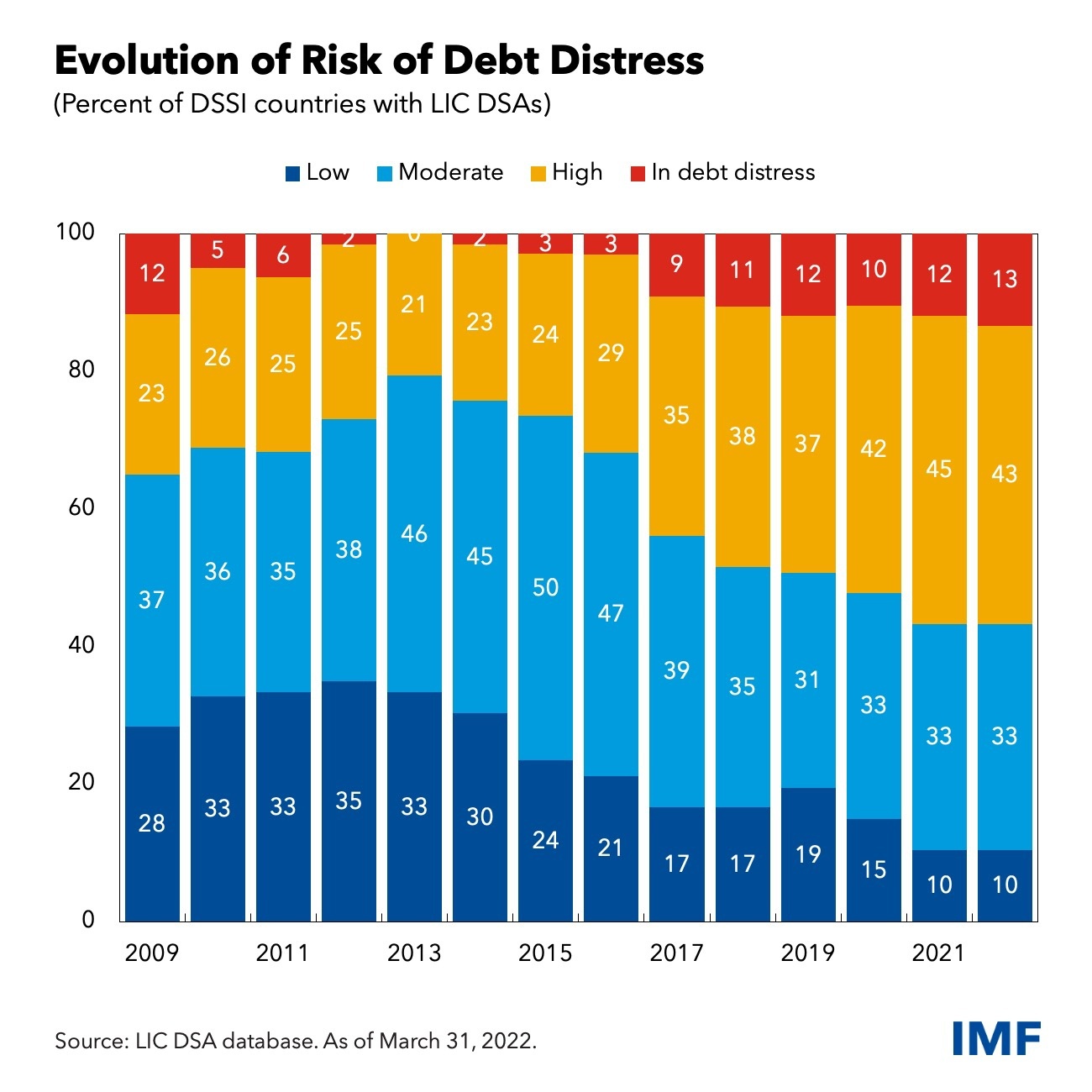

KS Jomo and Ngongo have expressed that since the 2008 global financial crisis, developing nations have to borrow massively from private finance – at exorbitant interest rates – to scale funding up ‘from billions to trillions’. Indeed, servicing external debt now blocks progress whereby governments have cut back spending in line with conditions or advice from powerful foreign economic agencies as such. Onset with the global debt crisis in 1979 the transition and developing Global South economies had paid cumulative US$7.673 trillion in external debt service, seePaulo Nakatani and Rémy Herrera.

In fact, the external debts of developing and transition countries reached 29% of their GDP in 2019. The short-term debts rose to more than one-quarter of the total external debts alone.

The Global South debt even then during the same period has increased from US$618 billion in 1980 to US$3.150 trillion in 2006, according to figures published by the International Monetary Fund (IMF). The external debt of this group of countries, comprising 145 member states, will continue to grow throughout 2007, according to the IMF, to more than US$3.350 trillion. The debt of the Asian developing countries alone could rise to US$955 billion, even though they have already repaid, in interest and capital, far more than the original amount due in 1980!

Malaysia 2019 external debt was RM$231225.9 million, (Asia Development Bank, External Debt Outstanding in Asia and the Pacific, Asian Development Outlook, April 2020).

According to a report to the Asian Development Bank, in September 2020, by Donghyun Park, Arief Ramayandi, Shu Tian stating inter alia that borrowing heavily for fiscal stimulus packages to support growth and provide relief for vulnerable groups whilst at the same time, private companies and households may be forced to borrow more to survive the economic impact of COVID-19…..In addition, the economic downturn challenges their capacity to service their existing debts. Therefore, despite widespread concerns about the current escalation of public debt and its sustainability, we should not lose sight of the potential risk from possible surges of private debt…..

Coupled with a weakening economy, already, as late as July 2023, a IMF Report has projected that under its baseline forecast, growth will slow from last year’s 3.5 percent to 3 percent this year and next – a 0.2 percentage points. Our MIDF Research data have maintained its forecast that Malaysia’s GDP growth would moderate at 4.2% in 2023 (2022: 8.7%), weighed down by uninspiring external trade performance as real export of goods is predicted to contract by 2.8% (2022: +11.1), reflecting weakness in regional and global demand.

Furthermore, the national household debt-to-Gross Domestic Product (GDP) ratio had already surged to a new peak of 93.3% as at December 2020 from its previous record high of 87.5% in June 2020, according to Bank Negara Malaysia (BNM).

Malaysia National Government Debt reached 255.4 USD bn in Dec 2023, compared with 246.4 USD bn in the previous quarter. Malaysia Government debt accounted for 64.3 % of the country’s Nominal GDP in Dec 2023, compared with the ratio of 63.8 % in the previous quarter; seecsloh, Destined to Debts.

We shall define the Global debt as borrowing by governments, businesses and people. Presently, it is at dangerously high levels. In 2021, global debt reached a record US$303 trillion, a further jump from what was record global debt in 2020 of US$226 trillion, as reported by the International Monetary Fund (IMF) in its Global Debt Database,21 Dec 2023.

The IMF must do more to support low-income countries and fragile states, Managing Director Kristalina Georgievasaid on Tuesday at the Center for Global Development (CGD).

Speaking with Masood Ahmed, CGD President, Georgieva called for the Fund to be more representative of the global economy, with a better balance between advanced economies and the voices of emerging and developing countries. She also expressed the need to help countries build resilience to a more shock-prone world.

Georgieva said she sees two equally important tasks for the Fund: “To ensure that we have the financial capacity to operate, and support vulnerable middle-income countries and low-income countries……And to bring our membership together….Despite all the difficulties in cooperation, we will work towards consensus on those issues on which the future of our children and grandchildren depend,” Georgieva said. She also explained the IMF’s role in its work on climate.

During a subsequent conversation with World Bank Group President Ajay Banga at an event on support for low-income countries, Georgieva shared more of the Fund’s thinking. For low-income countries to reduce vulnerabilities and achieve a sustainable and meaningful rise in income levels quickly, it will take the countries themselves to do more to build the strength of their economies, and the international community to be a reliable partner, she said.

“We see that those [countries] that are doing better are countries with strong institutions, rule of law, transparency, and less corruption, and building those strengths is something no one but the countries can take on.”

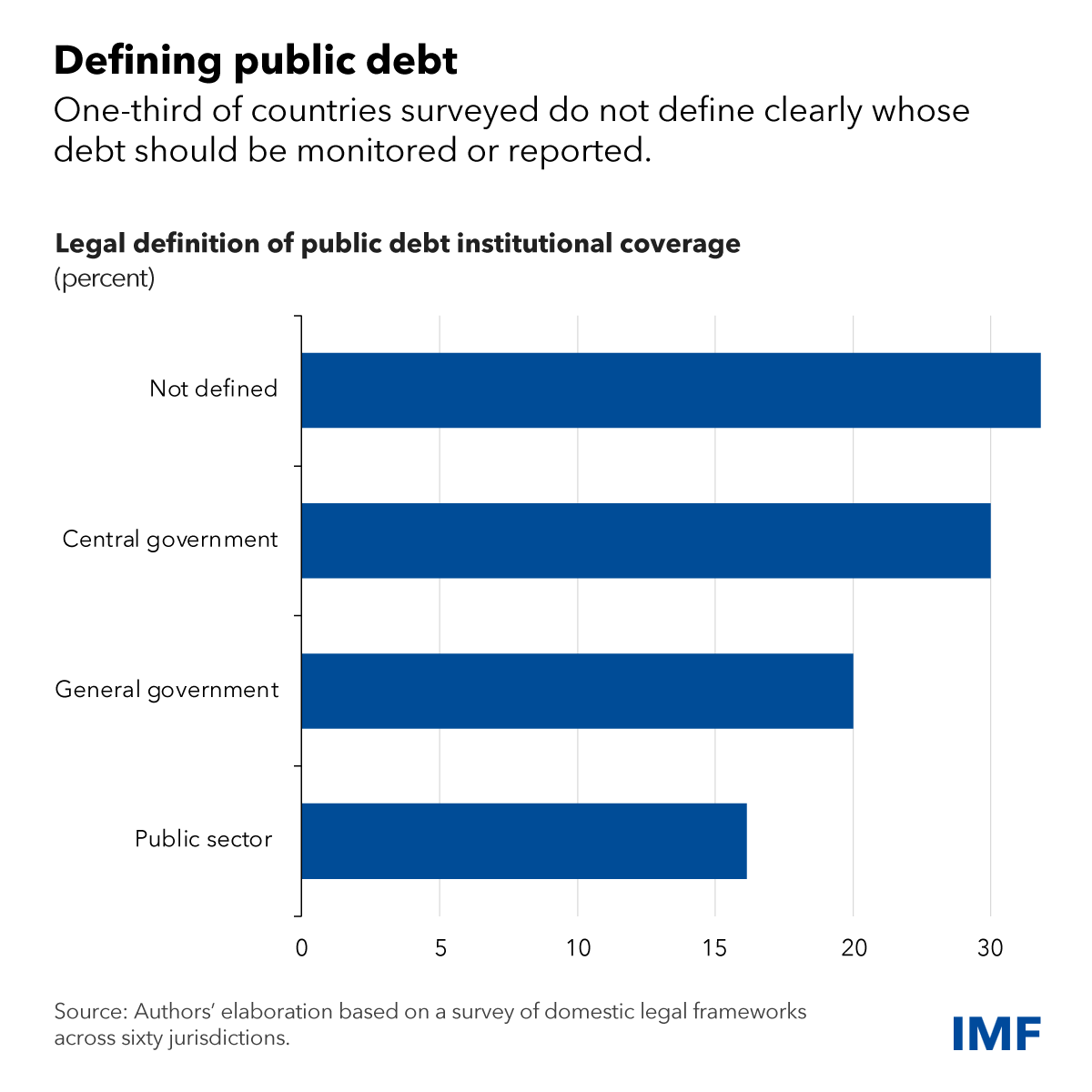

Domestic laws need updating to ensure that public obligations are transparent

April 2, 2024

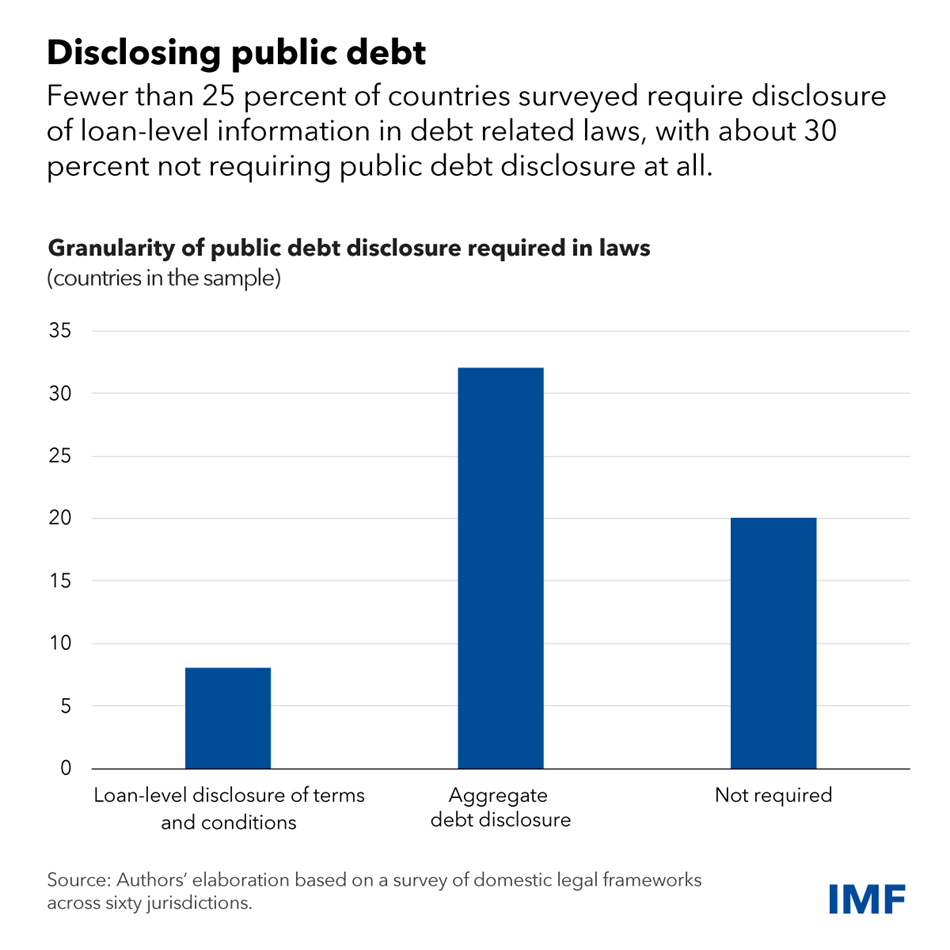

If efforts to address record global public debt are to leave no stone unturned, then weak disclosure laws warrant deep scrutiny. Hidden debt is borrowing for which a government is liable, but which is not disclosed to its citizens or to other creditors. And while this debt—by its nature—is often kept off the official government balance-sheet, it is very real, reaching $1 trillion globally by some estimates.

While these undisclosed obligations are not large when compared to global public debt topping $91 trillion, they pose a growing threat to low-income countries, already highly in debt with annual refinancing needs that have tripled in recent years. The problem is even more pressing amid higher interest rates and weaker economic growth. Accountability, too, is imperiled without accurate information about the extent of borrowing, which heightens the risk of corruption.

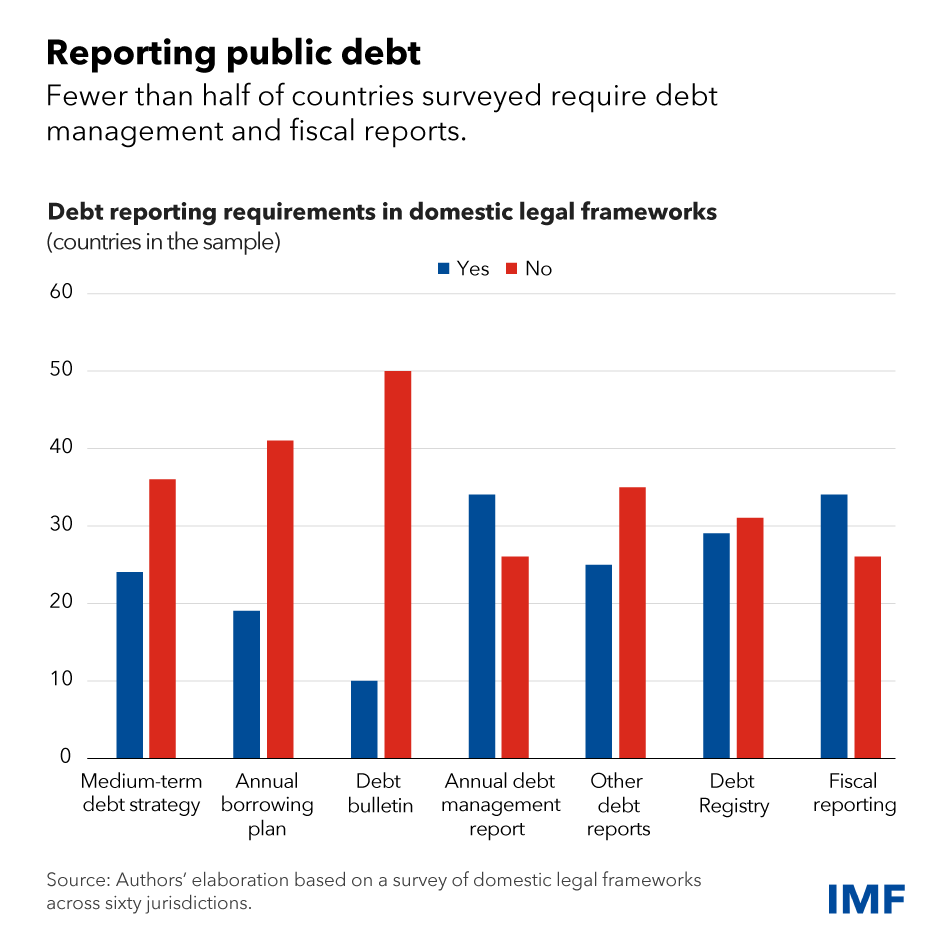

Building on a July 2023 paper, our new research shows that fewer than half the countries surveyed have laws that require debt management and fiscal reports, while less than a quarter require disclosure of loan-level information—key legal features for facilitating transparency. We also identify four noteworthy vulnerabilities in domestic laws that enable debt to be hidden: a narrow definition of public debt, inadequate legal requirements for disclosure, confidentiality clauses in public debt contracts, and ineffective oversight.

Definition

In many countries, a narrow definition of public debt, in one or in multiple laws, permits some forms of sovereign debt to escape oversight. We recommend that the definition of public debt be broad and comprehensive, meaning that it should capture arrears, derivatives and swaps, suppliers’ credit, and assumptions of guarantees as well as loans and securities. The definition should also cover extra budgetary funds, public trust funds (pension funds, for example), and special purpose vehicles.

A good example is found in Ecuador, which pursued legal reform in 2020 to ensure that short-term financing instruments—such as securities or treasury paper with terms of less than one year—were included in debt calculations and statistics. Other good examples include the legal definitions used in Ghana, Jamaica, Rwanda, Thailand and Vietnam, all of which encompass multiple types of debt instruments.

Disclosure

Second, across the globe, legal requirements for debt disclosure are inadequate. A strong legal basis is crucial to signal that there is a clear requirement to report debt data in a manner that is both timely and relevant for policy analysis, transparency and accountability. Strong reporting laws are found in in Benin, Kenya and Rwanda, which define both public debt reporting requirements and the timeframes for these reports.

Confidentiality

Confidentiality in public debt contracts directly hinders transparency. Across the globe, few laws regulate (and limit) the confidentiality of public debt, which hands policymakers wide discretion to label such contracts confidential for national security or other reasons. This is exacerbated by the fact that current debt-related international standards and guidelines provide limited guidance on how to tackle confidentiality issues.

We recommend that the law tightly define exceptions to disclosure and the scope of confidentiality agreements. Legislative oversight and other safeguard mechanisms such as administrative or judicial remedies should also be spelled out in the applicable legal provisions. Laws in Japan, Moldova and Poland are among the few that authorize legislative or parliamentary oversight of confidential information.

Oversight

The disclosure of public debt may also be inhibited where there is ineffective oversight governance by legislatures and supreme audit institutions (national government audit institutions), which are all important guarantors of accountability. Legislative bodies must be able to monitor and scrutinize public debt on behalf of the people, and they need to have staff able to read and grasp highly technical reports.

Several legislatures have a committee system—such as committees on the budget and public accounts—which allows for specialization among legislators. An example is in the United States, where the Treasury Secretary is required by law to send the annual public debt report not to Congress as a whole, but to two specific committees—House Ways and Means and Senate Finance. We also recommend that laws provide supreme audit institutions with the authority and the necessary powers to monitor and audit government debt and debt operations.

IMF role

Debt transparency not only benefits countries directly, but it is also essential for the work of the IMF. Hidden and otherwise opaque forms of debt make it more difficult for the Fund to fulfill its core mandate in a number of ways. For example, collateralized loans, novel and complex forms of financing, and confidentiality agreements make it difficult for the IMF to accurately assess a country’s debt and help bring its economy back on track.

Thus, the Fund works to bring the benefits of debt transparency to countries directly through technical assistance and also addresses the issue in our program engagements.

Well-designed laws make it harder to hide debt. But there are not enough of these laws on the books, despite their demonstrated benefits. Given the critical importance of getting transparency right, countries and their international partners must push for reforms to improve domestic legal frameworks, which in turn benefits both borrowers, legitimate creditors, and the system more broadly. Turning stones has never been more important.

— Kika Alex-Okoh contributed to this blog.

ADDENDUM

By way of confronting China with the peak paradigm by dispelling “Peak China” myths and affirming China’s development trajectory (john ross; Habib al Badawi; the diplomat; CfR; The East is Rising, the West is Declining {东升西降}) is much a discourse that China only wants to export its labour, that China only wants to grab the world’s resources, etc., and is engaged in debt diplomacy suppressing emerging economies in their development endeavours. The Johns Hopkins University’s China-Africa Research Initiative website has exceedingly valuable statistics and reports and blogs about this matter; this site also has a discussion on the China Trap Diplomacy whereas PRC firms are being told to reduce their financial exposures in overseas jurisdictions that could move to seize assets; and there is a good roadmap since the seizures of Russian assets after the invasion of Ukraine; readCounter Sanction Strategies that China Can Learn from Russia,Ding Yifan; Countering Western Sanctions, Yi Yan.

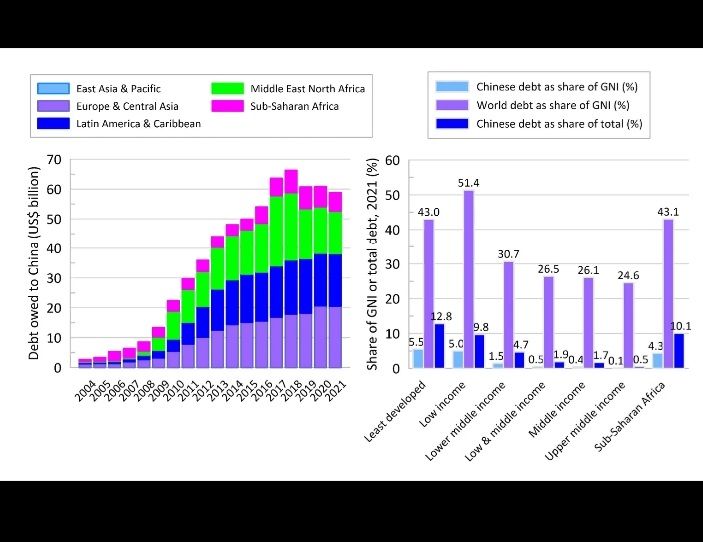

Looking at the chart below:

This chart actually plots Chinese credit, so it’s the debt of the rest of the world, the developing world, to China. And the chart on the left simply indicates the way in which debt owed to China has, of course, increased over the course of time as a result of Chinese development assistance and China’s lending, especially to parts of the Global South; readRISE OF CHINA AND DEMISE OF CAPITALIST WORLD ECONOMY.

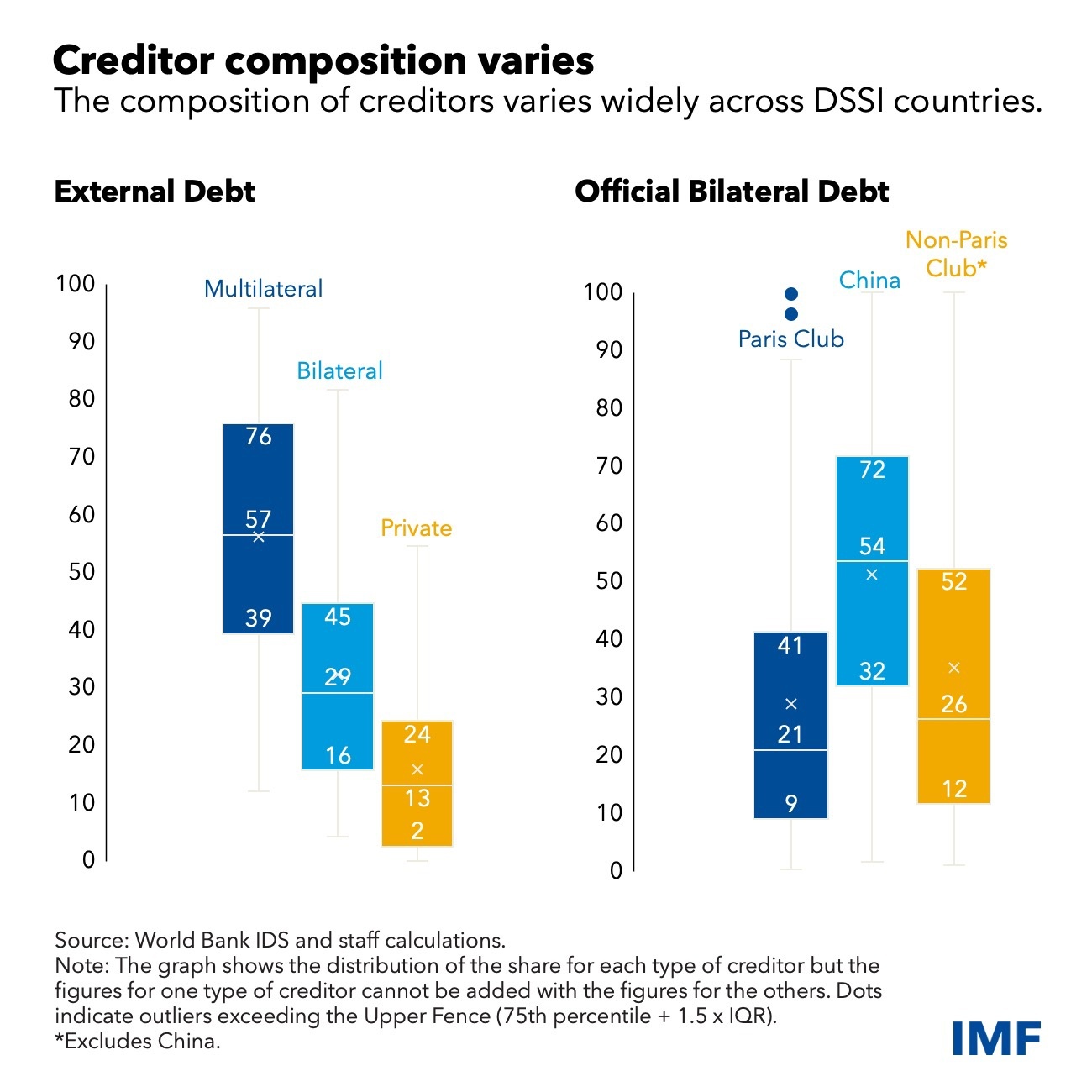

One of the very striking things about China is that a large share of its lending is, in fact, to very low income countries. It lends more to the least developed countries in the world than do the multilateral institutions and do the OECD group.

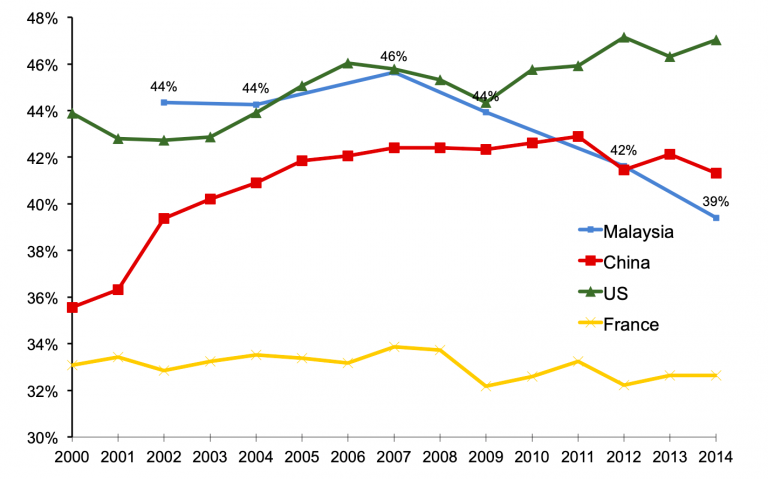

If you see the least developed countries, their total debt to the rest of the world is 43% of their gross national income, which is, nearly one half, a very substantial share. Of that debt, the share owed to China is only 5.5%. And Chinese debt amounts to 12.8% of the total.

China’s share of GNI is 4.3%, and its share of the total debt of sub-Saharan Africa is 10%. So these claims about a debt trap are, in a sense, simply do not stand up empirically.

Malaysia is at a juncture in its politico-economic path crashing into fractious politics headlong on an inequity route with an expanding B40 lower-income class, (mef.org 2023). The socio-economic situations are becoming precarious. This is because of a stagflation risk arising amid sharp slowdown in growth that is accompanied by an accelerated inflation runaway globally, (World Bank, Global Economic Prospects, June 7, 2022) as confirmed by the Bank of International Settlements in its Annual Economic Report, 26 June 2022, and amid subdued external demand could only edge up to 4.3% GDP in 2024 (World BankMalaysia Economic Monitor 2023), though Standard Chartered gave a favourable 4.8% of GDP; while the Madani Malaysia model is trekking slowly along an uneven economic development track that is strewn with global geoeconomic uncertainties and internal socio-economic instability.

Could and would the enlargement, and deepening, of the infrastructural platforms accompanying an artificial intelligence regime therein salvage the state of a nation or the adoption of such advance technology savages the country with further neo-imperial penetrative wounds while accompanying digitalised colonisation process?

I] INTRODUCTION

Standing at a crossroads of techno-capitalism and neo-imperialism, artificial intelligence (AI), with its potential promise though has profound existential problems to the Global South because advances in AI originated in wealthy nations of the Global North — developed in those countries for local users, using local data. Over the past several years, Columbia’sDanielBjörkegren and Berkeley’s JoshuaBlumenstock for Finance & Development have conducted research with partners in low-income nations, working on AI applications for these countries, users, and data. However, AI systems require investment in knowledge infrastructure, especially in emerging and developing economies, where data gaps persist and the poor are often, if not, always digitally underrepresented. Besides, developing nations typically ill-afford such expensive large-scale deep neural networks infrastructure using expensive AI-driven application software.

Afterall, Artificial Intelligence (AI) leverages computers and digital machines to mimic the problem-solving and decision-making capabilities of the human mind.

Frequently, the techno-optimism in the advanced economies (GoldmanSach 2023; and, according to a Bloomberg’s PwC Report, AI would boost the global GDP to US$15.7 trillion by 2030) is at odd with Global South economic development outcomes, (Daron Acemoglu Simon, IMF); where AI technology is in likelihood to destroying jobs and displacing workers, (Andrew Berg Chris, IMF); or where the building block for AI governance is weak (Ian Bremmer, Mustafa, IMF) on system design, project implementation and subsequent operational processes. Indeed, Artificial Intelligence could well widen the gap between rich and poor nations, (Alonso, Kothari and Rehman, IMF Blog Dec 2, 2020; IMF 2018).

Then, on this understanding, to duly acknowledge that in emerging markets such as India, where agriculture plays a dominant role, less than 30 percent of employment is exposed to AI. Brazil and South Africa are closer to 40 percent. In these countries, the immediate risk from AI may be reduced, but on the other hand, there may also be fewer opportunities for AI-driven productivity boosts, (Gopinath, Harnessing AI for global good).

Secondly, Silicon Valley corporations are taking over the digital economy in the Global South with little notice, or for those encouraged by the World Bank – but short-circuiting the rakyat2 – as in Malaysia,(WB 2021; MEM 2023), the domestic infrastructural platform ecosystems are already consolidated by the Global North monopoly-capital Big Tech, (STORM 2023). In case country South Africa, Google and Facebook dominate the online advertising industry, and are considered an existential threat to local media. Uber has captured so much of the traditional taxi industry that drivers have been petrol bombed in the “South African taxi wars”. Similar battles have broken out in Kenya, (al jazeera, 2019).

Netflix is not only pulling subscribers away from local television services, but are buying up content in Africa. While in India, Facebook was forced to cancel its “Free Basics” programme that gave the social media giant control over the Internet experience on mobile phones, she was able to retain its influence in countries like Kenya and Ghana.

This is known as digital colonialism where once former Colonial powers deployed their infrastructural domination in ports, waterways, and railroads across their vast empires, only that at present day neo-colonialism is continued through digital routers and data servers.

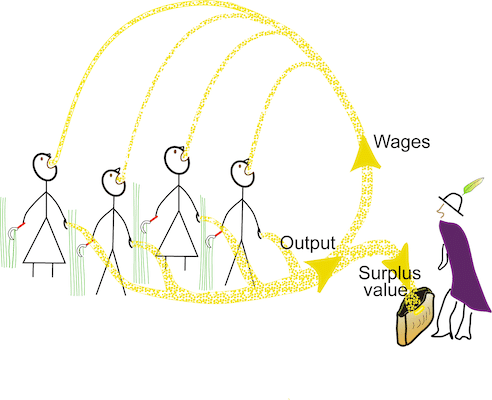

The digital infrastructural platforms are not unlike colonial ‘forward movement’ activities where lands are waiting to be discovered and conquered. Whoever gets there first, and holds fast and tight, shall get their information server-riches. The infrastructural platform kings (colonial-feudal lords) positions themselves above users (the colonised), and their data surfing activities (serfs’ farm cultivation), thereby giving them overwhelming privileged access (lordship) to record and retrieve (dictate and dominate) endusers (the serfs) as and when demanded (as surplus value expropriation) under an information-commodity chained monopoly-capital environment (via routers and cloud servers) .

Thirdly, tech capital flows unencumbered trans-borders where new ecosystem of digital platforms has emerged over the past decade that is transforming the very structures of capitalism. This new business model of large monopolistic digital platforms are capable of extracting immense amounts of data overwhelming legacy enterprises and suppressing labour empowerment, (seePaul Langley and Andrew Leyshon, 2020). This is “netarchical capitalism” , where infrastructure is “in the hands of centralized privately owned platforms”, (Nick Srnicek, Platform Capitalism, 2017).

Information and infrastructural platforms have empowered a new kind of ruling class. Through the ownership and control of information, this emergent class dominates not only labour but capital. It is not just tech companies like Amazon and Google; even Walmart and Nike can now dominate the entire production chain through the ownership of brands, patents, copyrights, and logistical systems – all “soft” elements than physical end-products, all accumulated through financialization capitalism through a neo-imperialism monopoly-capital pathway.

Digital technology has already indeed transformed the world economy; the decade leading up to 2019, the largest 100 firms in the world had increased their total market capitalisation by US$12.7 trillion. A third of that increase (US$4.2 trillion) can be accounted for by just seven firms: Facebook, Amazon, Apple, Alphabet, Microsoft (the famous quintet ‘FAAAM’), Tencent and Alibaba. The aggressive rally of tech stocks during the COVID-19 pandemic had given due recognition that an entirely new model of value creation was enabled, and primarily all enhanced, by digital technology. Tech companies are the new empires of today: Alphabet revenue surpassed Hungary’s GDP, Facebook employs over 15000 content moderators around the world, and Microsoft has built data centers in nearly every corner of our planet, with Google global dominating the infrastructural platform corporate businesses.

Hidden from view, but the most vital part of this Techno-capitalism identity is the convergence of fibre-optics under the strategic blue waterways and sea corridors around the world that connected the various routers and artificial intelligence neural-networked database in a singularity ecosystem:

Since raw data, processed information and uninterrupted communications are of prime importance in a globalised geoeconomic environment, the installation, repairs and maintenance of the underwater cables in the country are with these infrastructural platform players of tech giants such as Google, Amazon and Microsoft, and the national internet exchange body, Malaysian Internet Exchange. However, the conflicting battle between national sovereignty and Global North financialised monopoly capitalism only accentuate the brute reality of intrusive Techno-capitalism and its digitalised colonisation process, (STORM 2023, marine-cabotage-under-netarchical-capitalism; whereas, the neo-imperialism aspects on 5-Eyes, Unmanned Underwater Vehicles, USVs, and the geopolitics involving AUKUS and QUAD are covered in firesstorms, August 2022).

II] TECHNO-CAPITALISM

With the emergence of new capital, the capital-endowed new ruling class extracts the content capacity of information to route around worker and social movements to barricade labour participation and involvement. The emerging ruling class is the digital feudal lords overseeing a common of digital infrastructure where bands of peasantry-labour are the digital gig-slaves to be exploited. In this digitalized business model, returns do not diminish as businesses scale up but increase exponentially. Geared towards the exploitation of digital-dehumanised workers (Yanis Varoufakis) whence they are mere interfacing intermediary conduits to big data storage and retrieval by infrastructural platforms powered by artificial intelligence nowadays that are so overwhelmingly powerful in exploiting surplus value of labour relentlessly, and with brutal efficiency, it is the accumulation of capital, through and thoroughly (Ursula Huws, Labor in the Global Digital Economy: The Cybertariat Comes of Age, 2014; read a case country of digital knights in a kingdom of infrastrutural thrones, in STORM 2020; Big Tech and Large Gig-Labour: STORM, June 2022 and Digital Labour: STORM, December 2020 ; and a related essay on Techno-feudalism, in STORM, August 2022).

It is also becoming but unbelieving for foreign investors – specifically Global North monopoly-capital corporates – not wanting to partner local expertise to provide support and services from their financialised capital. These Global North entities insist on retaining their monopoly investments, especially on the infrastructural platforms varied ecosystems.

As an instance, the country needs local expertise to ensure our national undersea cables are well maintained and not to be wholesomely dependent on Global North monopoly-capital corporations on an unequal economic and inaccessible technological exchanges. That the international infrastructural platforms had once threatened to withdraw in cooperating with the national digital economic aspiration is uncalled for.

At a time of an epidemiological-economic-ecological polycrisis, many national banks accelerated the monetary flow – and the resulting wave of liquidity – leading to substantial increases in corporate wealth in many developed and advanced economies, whereas the emerging and low income economies face external debt distress compounding poverty of the global poors, (World Bank 2022; STORM, 2022, Wealthy Rich, Poverty Poors). As a result of falling income levels, widespread employment losses and widening fiscal deficits, (UNCTAD 2020) – a rakyat-oriented governance should not allow appearance of vulture-capitalism in the guise of infrastructural platforms be roaming the waves of high blue waterways as predatory pirates, (STORM, January 2023) when there is a sea of opportunities for the country in laying submarine cables, too:

And even as the Covid-19 pandemic coursed through the world’s population, Apple, Microsoft, Alphabet, and Meta Platforms – were able to rake in US$255.7 billion in profits in 2022, or 16.4% of the Fortune 500’s total earnings for the year, (Fortune, June 2023). Their capital accumulation revealed grotesque class and racial inequalities and the gross lack of public investment and preparation, (monthlyreview).

To compound developmental efforts, transnational corporations (TNCs) exploit legal loopholes in low-income countries (LICs) to avoid or minimize tax liabilities by applying a practice known as ‘base erosion and profit shifting’ (BEPS). Under such circumstances, tax havens collectively cost governments US$500–600B yearly in lost revenue. Low-income countries will lose some US$200B – more than even the foreign aids of US$150B that they received annually, (Jomo, June 2022). Indeed, TNCs-supported agents, and lobbies, have blocked the International Tax Cooperation initiative, (Anis Chowdhury and Jomo Sundaram, June 2021) to ensure tax equity and revenue intake equality, (see also STORM 2023, International Corporate Taxes – issues of misdeeds).

And whatever financial assistance as rendered, the World Bank category of aid only encourages governments to enable illicit financial outflows to offshore tax havens – where such tax havens could cost countries US$4.7 trillion over the next decade, (icij 2024) – reducing capital controls, thus draining further precious foreign exchange and government resources, (KS Jomo, 2024).

III] DIGITALISED LABOUR

Nested in the platform capitalism model is the software component and the associated IT infrastructural platforms’ solutions. Unlike in the manufacturing sector where labour is kept within borders while capital moves freely, in Big Tech there is this process ability to intrude into a target country to install infrastructural platforms as well as troll the planet for cheap labour in any part of mother Earth at any time.

The resultant, and a transformed economy, is the gig economy, also widely defined as “platform economy”, “on-demand economy” or “sharing economy”, synchronises to the demand and supply of short-term or task-based work activities, and as a part of the national economy where freelancing workers use digital platforms to participate in the national economy, including their connections with the traditional yet formal businesses. According to Emir Research, about four million people in the Malaysian workforce which is about 26% of the labour force work in the gig economy; this is almost double the global average.

This business model is what technology guruAzeem Azhar names as the ‘AI lock in loop’ where, as the tech companies deploy products and services, they also collect data about their consumers’ use of those products and services. Through machine-learning processes performed on those collated data, these business entities envisage in presenting opportunities towards the development of better products and services. It is by integration of multiple data-rich digital assets into a single platform that gives such tech companies access to the entire vertical product chains (examples like Google or Grab siphoning off personal biodata and geographical locations) and the supply-chain capacity to expand horizontally into new products and services with relative ease and effectiveness. For examples: Google, Facebook, WeChat or Grab becoming cloud-servers, WhatsApp as a communications medium and Instagram an media aggregator, (Social Europe, Gig Workers Guinea Pigs of the New World of Work, February, 2021 where ‘bogus’ self-employment workers are left outside of the regulatory framework; Foundation for European Progressive Studies, Governing Online Gatekeepers: Taking Power Seriously, 2021; see also ILO 2021 report on the states of precarious digital labour.

In case country Malaysia, the adoption of digitalisation only deepen the stronghold of the monopoly-capitalised infrastructural platforms that support artificial intelligence domain, in the digital frontier and defranchised digitilased zero-hour gig-labour, (STORM 2023). This informal employment sector not only occupies a sizeable segment of the country’s workforce but inevitably it is without adequate social security safety provisions in place, (read csloh, 2022: Workers; Emir Research: Brain Drain; bernama: gig-economy and Khazanah Research Institute 2020, Shrinking “Salariat” and Growing “Precariat”?):

For AI to bind adhesively within a national economic development initiative, not only must the monopoly-capital-compradore-capital eIements be done away, but the labour exploitation factor be eliminated, too. Labour superexploitation conceptually captures the real condition of the working class in Africa, Asia and south America. It involves three elements: low wages, long hours, and intense work leading to due strenuous exhaustion. Above all, it is characterised by “the greater exploitation of the worker’s physical strength, as opposed to the exploitation resulting from increasing his productivity, and tends normally to be expressed in the fact that labor power is remunerated below its real value.” Ruy Mauro Marini.

An AI class analysis can be by way of applying Nicos Poulantzas concept of class [places] as existing at each of levels of society: economic, political, and technological. The class [positions] of the capitalist fundamental class processes are productive endusers (performers of data entry) and productive capitalists (extractors of processed data in the form of information).

The class relationship where dominating [power] ensues would be identified, therefore, through the stronghold of infrastructural platform [place] which has allied with financialised capital providers [positions] in the provision, control and ownership of software, hardware and process [power].

Capitalists appropriate surplusvalue from the consumption of enduser’s labour activities during the generation of data into processed information. The surplus (monetary and or metadata of say geographical locations in an e-hailing process) is distributed as extracted among beneficiaries of subsumed class positions like the state-enabler, IT vendors, financiers and compradore monopolies.

In essence, historical politico-economic development of a country comes from social practice, the struggle for production, the class struggle, and scientific work.

For the SCRIPT in Madani Malaysia to be successful, in term of implementation and sustainability of an AI-driven progressive politico-economic developmental praxis, working-class unity has to be consolidated. It can only be further solidified if the tenet of divisive divisions by capitalism is better understood both in theory and in practice. Hence, we argue for a comprehensive yet bold project that is based on TAPAO that goes beyond its ethos as a renewal of an socialist ideal with Malaysian characteristics in order to take full account of the struggle of the labour movement.

EPILOGUE

What are the remedies to limit infrastructural platform capitalism dominance, the AI perversion and the digitalised colonisation process?

A global tax on capital or the implementation of the Wealth Tax at the national level, is one way to allow for the creation of a “social state” meeting social needs, (Piketty, Capital in the Twenty-First Century).

Taggling digital labour by putting the most essential needs of people and the environment before profits where provision “jobs…for the unemployed, food for the hungry, houses for homeless, adequate health care and income security and a decent environment for all of us” whereby the highest priority is an implementation of these collective human goals to which all special interests would then be subordinated. (Magdoff and Sweezy, Stagnation and the Financial Explosion, 88–90).

The cacophony on orchestrating the Madani Economic Narrative ( MEN) is overwhelming loud, with the Malaysia Institute of Economic Research (MIER) not likely to hold the baton too soon.

Whether the Madani precepts alone can serve as the pillars of a grand nation-building project when a rumah in a kampung built on a capital-muddied stilted foundation likely to collapse at any time under a neoliberalism policy regime, is due for a conversation.

This is appropriate time because even an neoliberal institution – which was in the country prior to her independence as the International Bank for Reconstruction and Development (IBRD precursor to the World Bank) – has once again expressed the multifaceted problems facing the economic state of a nation:

These uncomfortable situational conditions are further decimated by the MIDF Research data which maintained its forecast that Malaysia’s GDP growth will moderate at 4.2% in 2023 (2022: 8.7%), weighed down by uninspiring external trade performance as real export of goods is predicted to contract by 2.8% (2022: +11.1), reflecting weakness in regional and global demand.

The 2nd August 2023 economic brief indicated that Malaysia’s S&P Global Manufacturing PMI recorded at 47.8 in July 2023 (June 2023: 47.7), marking 11 straight months of contraction which was mainly attributable to a significant dip in new orders, as demand has consecutively paced down for the last 11 months, (theedgemalaysia 2/8/23

The Madani Challenges facing this state of nation were familiar issues covering +65 years in the development of underdevelopment of a nation where poverty, inequality, and marginalisation are predominant. As late as 2015, the Malaysia poverty rate was 4.80% which is the percentage of the population living on less than US$5.50 a day, (World Bank).

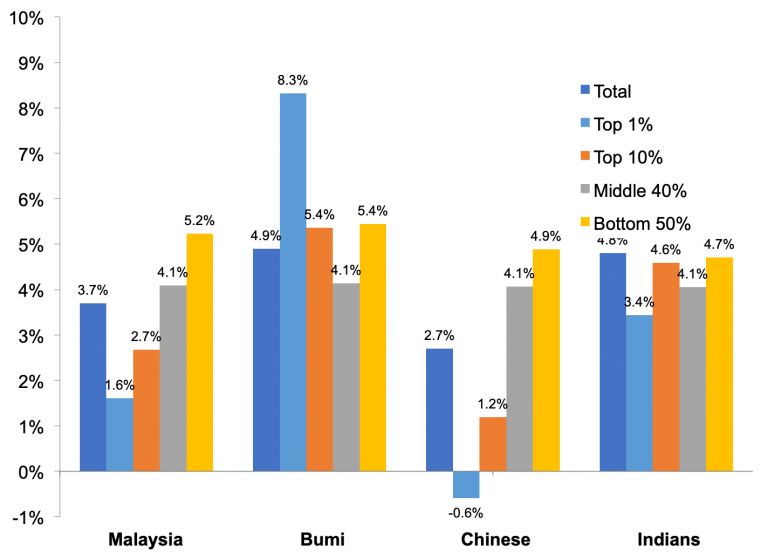

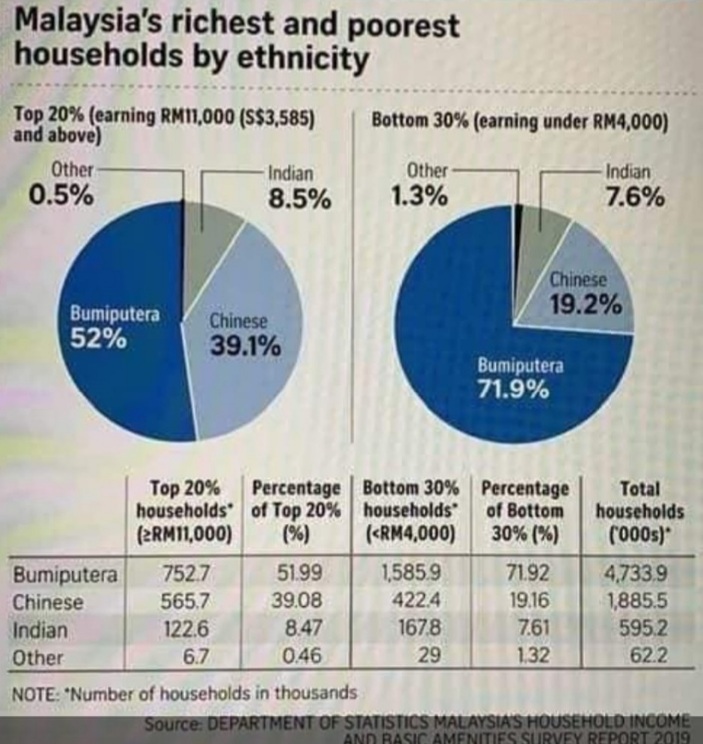

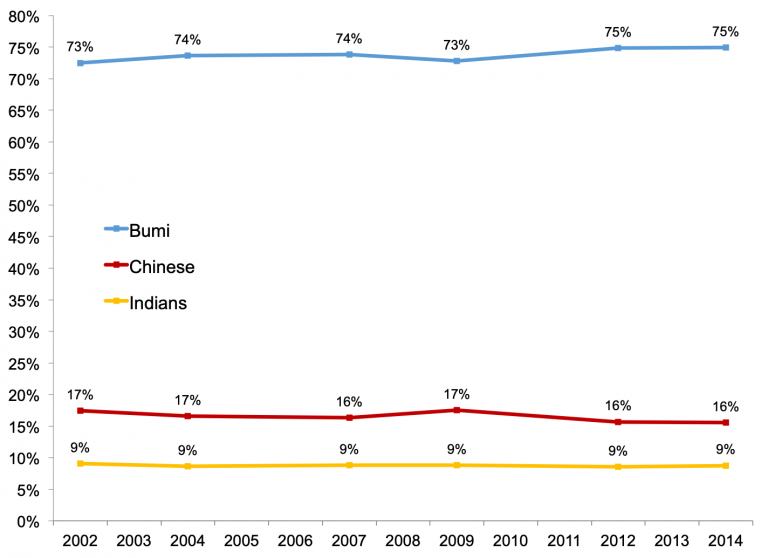

This is ardently expressed by Khalid research paper at the London School of Economics and Political Science, where presented, the disparity among the Malay community – the top 1% – is very much acute then as it is likely to be accentuated:

The most important implication is that although the middle 40 per cent and the bottom 50 per cent benefited significantly from economic growth, the Bumiputera in the top income groups (the top 1 per cent and the 10 per cent) benefited the most from economic growth. In sharp contrast, the income of the Chinese in the top income groups deteriorated. In a way, the strong growth in high-income Bumiputera occurred at the cost of a decrease in Chinese and the slow growth of Indians in the top income groups; Khalid, Income Inequality and Ethnic Cleavages in Malaysia: Evidence from Distributional National Accounts (1984-2014), World Inequality Database, working paper No. 2019/09.

The World Bank Report has this to say:

“The bulk of inequality today can be explained by differences in socio-economic factors within ethnic groups rather than differences across groups. It is time to bring all Malaysians within the ambit of greater economic opportunity.”

The need to update Malaysia’s inclusiveness strategies reflects both new realities and new challenges. The new reality is that poverty is no longer the key issue when thinking about inclusive growth. Poverty still exists—and pockets of poverty remain deep and concentrated—but inequality is now in the spotlight and is presenting a tremendous challenge. The other new reality is that inequality is no longer what it was four decades ago. Nowadays over 90 percent of the level of inequality is explained by differences within ethnic groups rather than differences between these groups. Individual socio-economic characteristics, such as activity status, sector of employment, urban versus rural stratum, and educational levels in different geographical locations are despairingly displayed.

To undertake this task, according to Philip Schellekens, lead author of the Malaysia Economic Monitor, (World Bank, 2010).

“The dual approach in the Economic Transformation Program of combining cross-cutting policies with private sector-led projects provides an excellent platform. The proof of the pudding, however, will be in the consistent execution of policy reforms,” he said. “Also, until solid implementation of policy reforms is seen there is unlikely to be a groundswell of positive sentiment of foreign investors towards Malaysia.” (World Bank 2010, ibid).

The November 2010 issue of the Malaysia Economic Monitor offered another analysis of where Malaysia is today and where it could go tomorrow by updating its inclusiveness strategies. “Our recommendations on this highly charged topic do not come out of the blue — they are based on a detailed analytical study of the latest household income, labour force, and enterprise surveys, which the authorities have made available to our team. We are also leveraging on the experiences of other countries around the world, who have addressed or are coping with similar challenges.”

The implementation of an economic development plan requires the proficiency and professionalism of the public sector. This is where the effectiveness from the public service is under constant, and continuous, doubts.

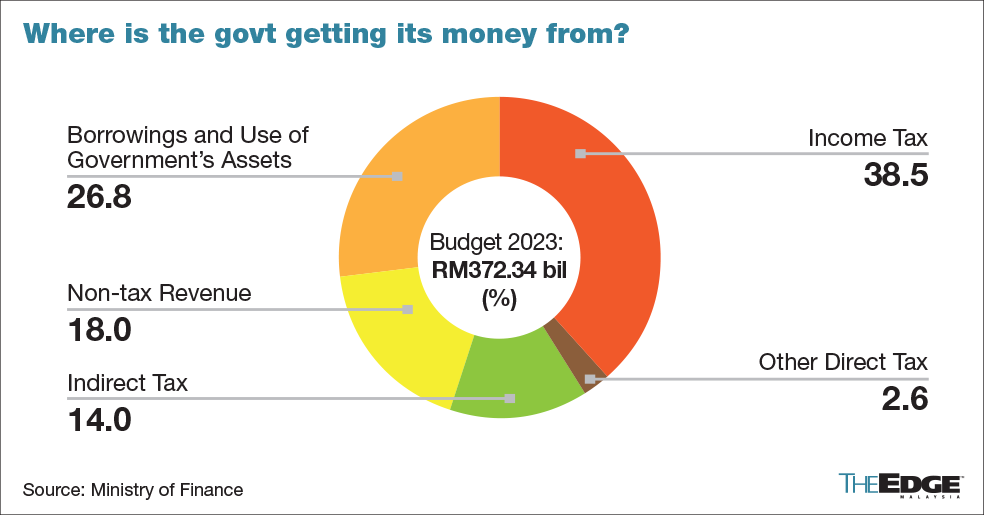

At a time when the emoluments and the retirement charges of the public sector constitute 31.2% of the RM$372.340 million Budget 2023 announced on 7th. October, 2022 (which excludes contingency reserves yet-to-be disclosed) in the operating expenditure which are equivalent to the 32.8% of development expenditure for socio-economic programs and projects, including subsidies and social assistance – there is more than much concern on the performance and productivity of our civil servants whom,some alluded, to performing money-laundering.

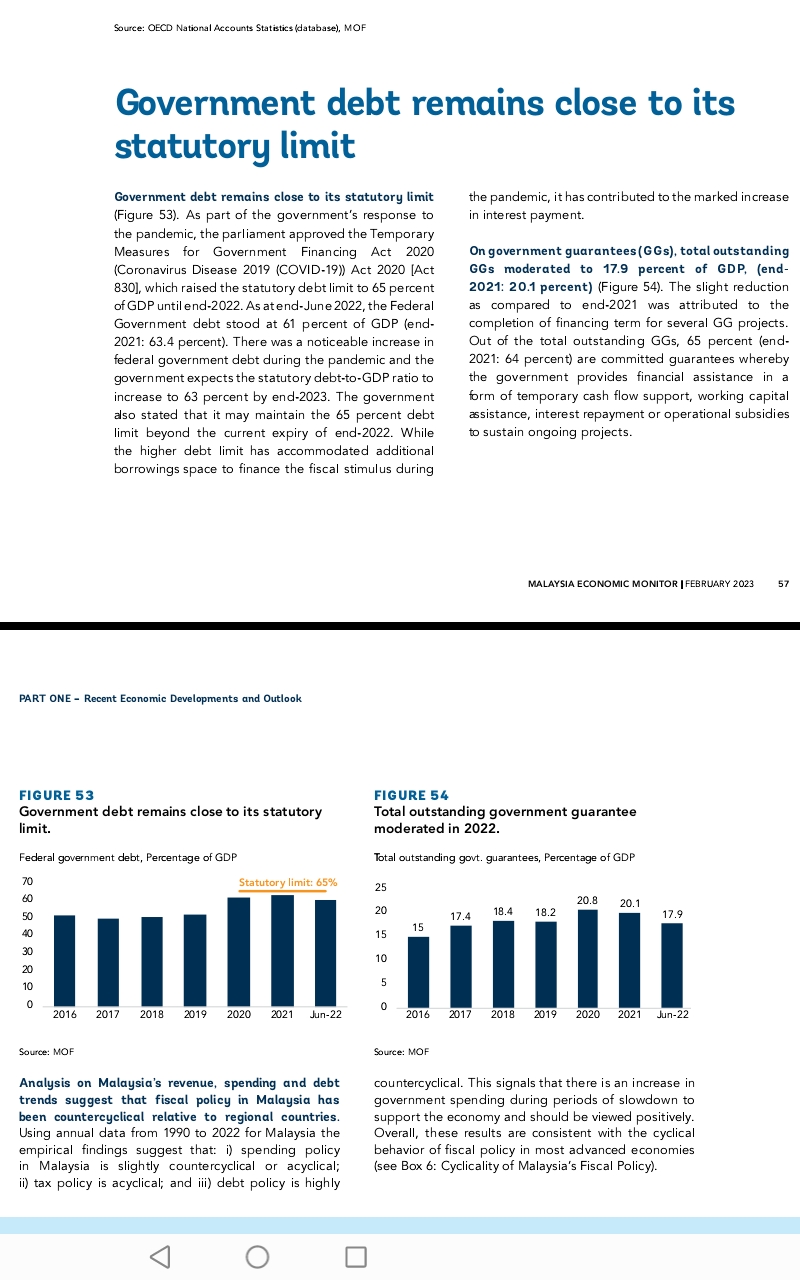

This is heading a grueling question on total government debt and liabilitiesas of June 2022 which is estimated to be at RM$1.42 trillion and will rise further; indeed, it was announced on 17th. January 2023 that the national debt including liabilities has reached RM$1.5 trillion. Total debt and liabilities are already 82 per cent of GDP, (read STORM October 2022, Underdevelopment of Development – consolidation of financial monopoly-capitalism).

As a share of revenue, a review done by the World Bank as far back as in 2011 has had found that Malaysia was spending about 27 percent of its revenues on salaries and wages/personal emoluments in 2009, significantly more than in some of the higher-income countries it aspires to emulate such as Canada (13.7 percent); Norway (12.5 percent); Australia (10.6 percent); and South Korea (9.6 percent).

In fact, by 2018, this percentage has increased to 34.3 percent for Malaysia, (seeWorldBank (2019). Malaysia Economic Monitor: Re-energizing the Public Service).

This is an extract from the World Bank 2019 Report on the challenges Malaysia has to confront to fulfill rakyat2 expections:

Can productivity performance objectives be executable or even achievable?

The second major restructuring requisite is the generation of government revenue to implement economic development programmes whilst supporting a top heavy, and inefficient, public sector – at a time when national fiscal revenue space is narrowing:

III] FINANCING ECONOMIC DEVELOPMENT

With those underlying facts, the key task is to source funds for economic development. This is well explored in (STORM 2023, Debt financing towards progressive economic path) where the nuances of the conversation are that since expenditures are already at high levels; and secondly, other operating expenditures components such as supplies and services, and grants and transfers have been on a declining trend or are already at low levels, therefore, the government’s current fiscal consolidation plan would have to include – besides restructuring Petronas, Khazanah and the GLCs -a higher revenue collection target that should coverage of a windfall tax on industries , according to Khazanah Research Institute senior advisor Professor Dr Jomo Kwame Sundaram.

“This is precisely the time when you must reform taxes as you have it (windfall tax) all the time amid extraordinarily high petroleum prices or palm oil prices.”

This is concurred by Institute of Malaysian and International Studies research fellow Dr Muhammed Abdul Khalid who pointed out that policy-makers tend to ignore the imposition of capital gains tax when it comes to the issue of tax reform.

Even Bank Negara Malaysia (BNM) assistant governor Dr Norhana Endut noted that the government’s tax collection capacity had not kept pace with the economic growth, at a time when the manufacturing sector is moderating on its p erformance:

IV] PRAXIS IN ECONOMIC REJUVENATION

The economic development of a nation demands that its goal to attain high-income and developed nation status while ensuring that shared prosperity is also sustainable.

As one of the many Global South countries, Malaysia is one of the most open economies in the world with a trade to GDP ratio averaging over 130% since 2010. Openness to trade and investment has been instrumental in employment creation and income growth, with about 40% of jobs in Malaysia linked to export activities.

A government is always confronted with difficult decisions about appropriate measures under unforeseenable situations or in a crisis: what restrictions to impose and when to loosen them, where money will be spent and how it will be raised, and how to coordinate tasks between states and enable community cooperation.

These decisions have to take into account public health recommendations, economic considerations, and political constraints. Just as the policy responses varied – from the 2007–08 Global Financial Crisis, the dotcom 2002 burst and the Asian Financial Crisis in 1997 – so do national policy responses to the COVID-19 pandemic should differ for health, economic, and political reasons.

Play Politics

Why does the advice of independent consultants, analysts, and the academic go so often unheeded?

Political economy is about how politics affects the economy and the economy affects politics that Governments try to prime the economy before elections. However, business cycles are also creating ebbs and flows of economic activity and the circuitry of capital distribution around elections whence economic conditions have a powerful impact on elections. Politicians would manipulate these economic parameters to woo voters to gain political advantages, and contesting capital tries to support politicians.

Where are we now?

There is a cohort of powerful interests in favour of international trade and foreign investment. The world’s transnational corporations and international banks depend on an open flow of goods and capital. These are the monopoly-capitalists and the financial capitalists. This is especially the case today, when the world’s largest companies depend on complex global supply chains. A typical transnational corporation produces parts and components in dozens of countries, assembles them in dozens more, and sells the final products everywhere. Trade tariffs create barriers with these supply chains, thus the world’s largest companies are biggest supporters of freer trade.

That is why there is a need for perpetuating the mass of special and general interests in society so that these social institutions play a major role in national policymaking. The ways in which societies organize themselves – through and by economic sector, ethnicity, and importantly at this juncture of our political awareness, the class factor, shall affect how we would like to restructure our politics.

Definitely, political institutions have to mediate the pressures constituents bring to bear on them; even oligarch rulers have to pay attention to at least some part of public opinion. Political economists call this the “selectorate,” that portion of the population that matters to policymakers. In an authoritarian regime, this could be an economic elites or the ruling class or the armed forces. In an electoral democracy it would be voters and interest groups. No matter who matters, policymakers need rakyat2 support to stay in office.

In building an equity society with socialism as the dominant foundation, we must do all we can to develop the productive forces and gradually eliminate poverty, constantly raising the people’s living standards. Only when this outcome is achieved and there is significant prosperity for all will it become possible to begin the shift to advanced stage of an economy that is highly developed and where there is overwhelming material abundance. Only by this process that we shall be able to apply the principle of from each according to his ability, to each according to his needs.

To achieve this process, there is a need on genuine planning and genuine democracy where these are through the constitution of power from the bottom of society. It is only in this way that a progressive socioeconomic society, and its healthy and well-being domain, becomes irreversible.

Towards this process in striving the Socialism with Malaysian characteristics goal, there shall be a combination of planning and markets forming the basic socialist economic system. Second, we need to keep in mind the dialectical relation between ownership and the liberation of the productive forces that shall entail, then

(1) the system contains a multiplicity of components, but public ownership remains the core economic driver, with corporate capitals supplementing capital formation but without undue surplus value extracted from labour;

(2) while both state owned and private enterprises must be viable, their main objective is not profit at all costs, but social benefit that meets ‘people-centred’ needs from appropriate shelter, education equity to community-base healthcare, harnessing modern technologies towards social needs;

(3) it employs the primary socialist principle of from each according to ability and to each according to work, limiting exploitation and wealth polarisation, and ensuring common prosperity and wealth sharing for every rakyat2 wellbeing;

(4) the primary value should always be ‘socialist collectivism’ – gotong royong community-based than bourgeois individualism and inflicted neoliberalism ethos.

Therefore, as applied under a TAPAO approach, it would be sizing and averaging rural per capita income besides focusing on the country’s hinterlands, especially the mountainous interiors of Sarawak and Sabah.

Refining the geographical target of poverty reduction programs is a necessity. The TAPAO needs to shift from daerah² to kampung² including more likely some outside the list of poverty-stricken daerah, too. Collectively, those designated kampung² (villages) may cover a certain high percent of the country’s rural poor. Designated villages could then apply for projects to support local production and infrastructure (including makan-pada-kerja : food-for-work programs, worker training, and agribusiness development comprising technology extension services; not to be neglected, government-linked investments in social infrastructure (schools, clinics, community and recreation centers), with a particular strong participatory community-based self-help gotong-royong approach.

V] MADANI IMPLEMENTATION PRINCIPLES

For the SCRIPT in Madani Malaysia to be successful, in term of implementation and sustainability of a progressive politico-economic developmental praxis, working-class unity has to be consolidated.

It can only be further solidified if the tenet of divisive divisions by capitalism is better understood both in theory and in practice. Hence, we argue for a comprehensive yet bold project that is based on TAPAO that goes beyond its ethos as a renewal of an socialist ideal with Malaysian characteristics in order to take full account of the struggle of the labour movement.

Within the context of Malaysia development of underdevelopment – glaringly as in the cases of northeastern states in semanjung and the Borneo states of Sabah and Sarawak, and the many urban poors in the country as documented by the World Bank and UNICEF, we are witnessing the relational inequality generated. This is further reproduced by labour superexploitation and relational surplus value whence labour superexploitation is the essence of capitalism as neoliberalism is imperialism, too.

For Malaysia politico-economic model to be successful, and sustainable, the core issue of contradiction between capital and labour needs to be resolved with a Madani trustful outreach.

More so, after ethnocapital has owned, controlling and dominated the Malaysia resources, it is appropriate period of a new era under an unity governance to present a new narrative on Malaysian labour working cohesively and collaboratively – at this particular junction of a historical period – with capital to a shared prosperity domain under a common wealth practice for labour, too.

For one main obvious reality of capitalism is that massive poverty across the Global South is not the result of some local insufficiency (resources or skill talent) but rather due to the functioning of neocolonialism perpertuated by liberal economic policies as neoimperialism where the ongoing effects of dependency on financialisation capitalism need to be tamed.

The haemorrhage to present economy is the resulting outcome of those extractive institutional forces since post-independence, accelerated by succeeding regimes in governance with odious practices, and as articulated by Prof Kamal Hassan in Corruption and Hypocrisy in Malay Muslim Politics while Khalid’s London School of Economics and Political Science research has pinpointed the class structure-laden beneficiaries to their enduring enterprises.

The trust between labour and capital has to be firmed up solidly in fulfillment of a Madani Malaysia – more so when 98.5% of businesses are the SMEs contributing 36% of the national GDP where labour is important as capital because it provides employment for 7.3 million people – nearly half of the country’s workforce.

EPILOGUE

In short, we need to modify, adapt, and contextualize a conversation with our preceding political-economic reform agenda, and while trying to calibrate the sequence of, and the dimensions for, economic reforms – we seek to ask the pertinent question: have we really restructured the stagnated, and a doomed, national economy, ever ?

We need to be in the threshold of a new sovereignty re-imaging a New Malaysia positioning an entity adhering a New Narrative to perform New Politics for the generasi muda.

What had been lacking through +6 decades in the economic development of the country is not due to lack of the vision or mission goals, but the inappropriate deployment of resources and the mishandling of allocated resources, overlaid by the socio-anthropological dimension with the burden of privileges that pulled back nation’s growth trajectory.

Glaringly, the civil service servants had been the dreadlocks that entangled the national productivity, then coupled with the trials of systemic odious practices – often enabled and or connivance with public service elements – have hung-dried an Asian tiger, (readSTORM 2023, Place, Position, Power of Public Sector).

To revisit 2010, when trying to meet the growth targets of the 10th Malaysia Plan, “it would require a significant rise in productivity and investment,” so said Philip Schellekens, lead author of the Malaysia Economic Monitor, (World Bank, 2010).

“The dual approach in the Economic Transformation Program of combining cross-cutting policies with private sector-led projects provides an excellent platform. The proof of the pudding, however, will be in the consistent execution of policy reforms,” he said. “Also, until solid implementation of policy reforms is seen there is unlikely to be a groundswell of positive sentiment of foreign investors towards Malaysia.” (World Bank 2010, ibid).

Also, while trying to achieve Malaysia’s Vision 2020 goal of high-income status, at that moment of an era, would require “a higher growth rate than that achieved in recent years,” so said World Bank Sector Director for Human Development, East Asia & Pacific, Emmanuel Jimenez, “the (other) challenge is also to ensure that the benefits are broadly shared across all layers of Malaysia’s society. While Malaysia has made truly impressive reductions in poverty, inequality persists at high levels.” (readfurther on race, class, poverty and inequality in malaysia new left, 2021).

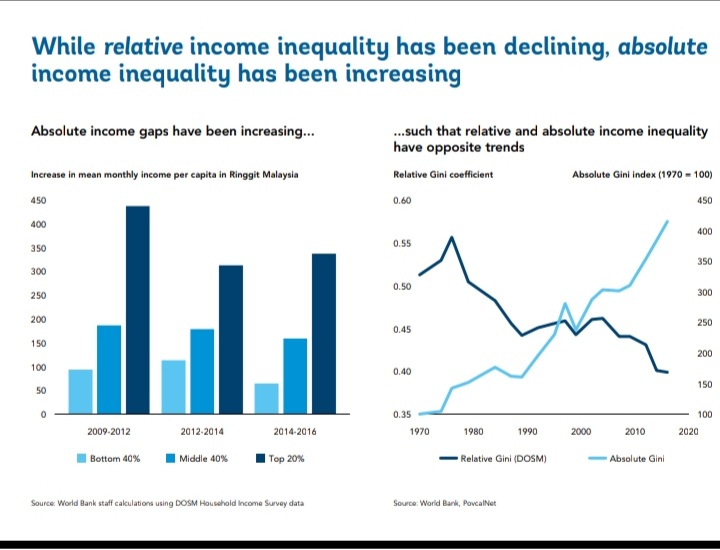

After six and half decades of sustained neoliberalism economic developmental effort, the nation of Malaysia is still as accentuated in absolute income inequality as ever, (seelower right chart below)

Sources: World Bank datasets and DoSM statistics

Further expressing that “The bulk of inequality today can be explained by differences in socio-economic factors within ethnic groups rather than differences across groups. It is time to bring all Malaysians within the ambit of greater economic opportunity.”

This is ardently expressed by Khalid research paper at the London School of Economics and Political Science, where presented, the disparity among the Malay community – the top 1% – is much acute, and accentuated:

Some had articulated that it is the faulty education ecosystems, but while many Malaysians cannot take advantage of income-earning opportunities because they lack the skills to do so, then, despite massive investments in education, for many others, skill needs have changed more quickly than the availability of educational and training opportunities.

It begins to dawn to policy-implementors that as Malaysia seeks to increase knowledge and innovation in its economic activities, it is even more important not to marginalize the unskilled workforce who more likely than not is categorised under as underemployment and or performing zero-hour activities in the gig-economy with all attributes of extractive surplus value being emphasised, and endorsed within a capitalism praxis.

We seems to be living in an era not dissimilar to imperial ownership and control where wage growth remains very low while capital maximized investment returns through extracting surplus-value from labour.

The widening of absolute income gaps between the bottom 40 percent and the top 20 percent of the income distribution have only furthered the angered sentiment of being left behind.

Therefore, in complementary to education is the necessity of labour market reforms that raise the level of employment, streamline the regulatory environment for businesses and remove barriers for new investment.

However, even if income-earning opportunities exist and access to labour, it is still broadly inadequate because some Malaysians will inevitably remain excluded or require temporary support.

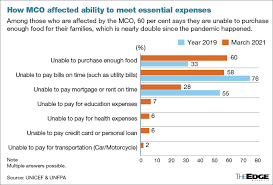

Thus, though important elements of a social protection system are in place in Malaysia, there are still many significant gaps remaining – distinctively displayed during the Covid-19 pandemic when income disparity within populace was further accentuated.

It was also a time when 70% of lower-income households cannot even meet monthly basic needs – indeed, more than 60% of these households reported having no savings at all – not much of a difference than 10 years ago:

and where these household expenditures are expansively spent on food:

But, not every poor, even urban, household has all the requisite food nor valued nutrients (UNICEF 2018):

In the study, Children Without – A study of urban child poverty and deprivation in low-cost flats in Kuala Lumpur, UNICEF unearthed:

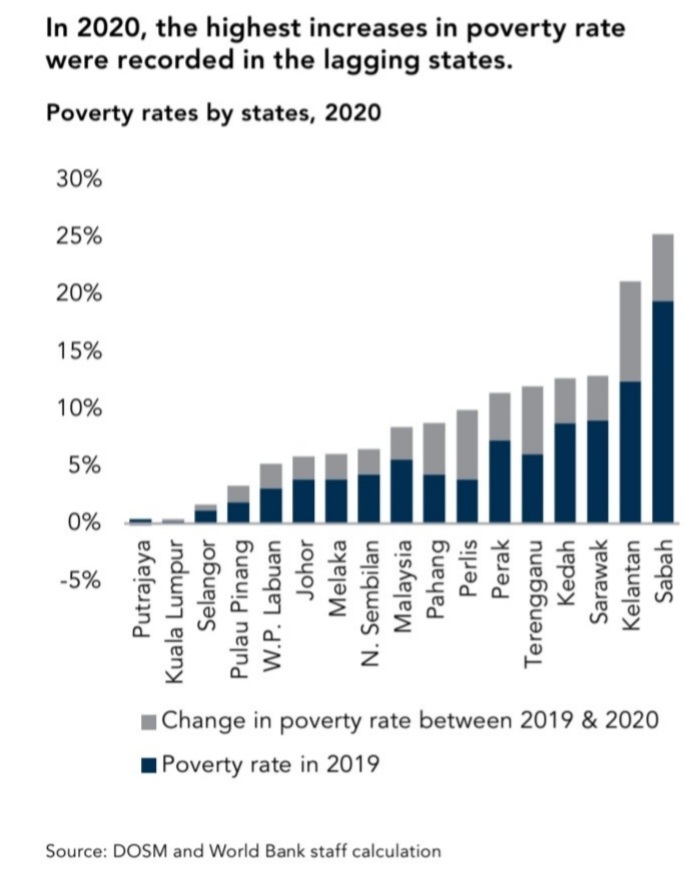

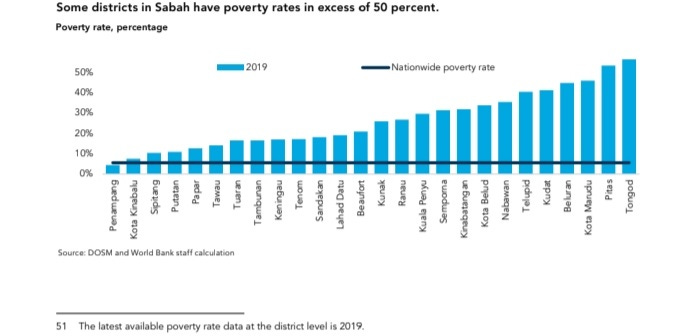

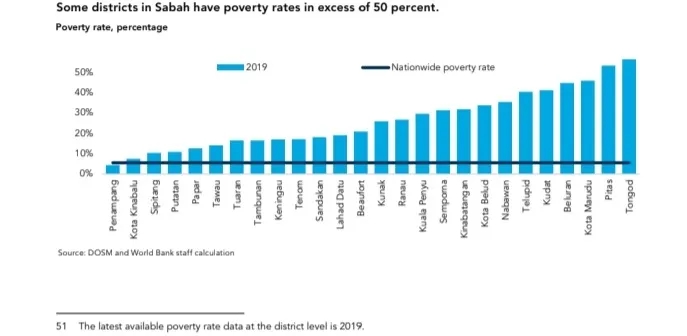

Further, the state of Sabah gross domestic product per capita of RM5,745, compared with the national average of RM7,901, (read csloh , Sabah – a state underdeveloped) where the Borneo state’s poverty rate is three times that of the national average, and there is a high degree of inequality across districts, too:

One way out of this continous poverty trap is that social safety net programs should be more poverty-focus, targeting mechanisms have to be improved and fragmented programs could be replaced by a well-coordinated social protection system, (seeMalaysia Economic Monitor, November 2010 – Inclusive Growth).

Indeed, in the subsequent World Bank Report 2022, the social safety net resurfaced whereby the agency again with an urgency recommended that:

In the short term, financial support for the poor and vulnerable should continue. This includes a more inclusive social insurance framework with improved targeting. The continuation of cash assistance programs to support financially disadvantaged households will provide safety nets and much-needed protection from economic shocks.

The subsequent subsection is a Creative Commons reposted blog by PHILIP SCHELLEKENS, November 08, 2010, where he argued

Why Updating Malaysia’s Inclusiveness Strategies is Key

Compare South Korea and Malaysia in 1970 and compare them again in 2009. South Korea was a third poorer back then and is now three times richer. Even more remarkable has been South Korea’s ability to widely share the benefits of this spectacular feat across broad segments of society. South Korea’s strong focus on broad-based human capital development allowed the country to transform itself into a high-income economy, while at the same time reducing income inequality and improving social outcomes.

Malaysia’s inclusiveness strategies have produced some remarkable successes as well. Malaysia dramatically reduced poverty and has all but eliminated hardcore poverty. But the country has been far less than successful in reducing income inequality which, since 1970, steadily fell for two decades but has stagnated at high levels ever since. The last two decades also saw Malaysia’s growth model of high-volume low-cost production being challenged. Economic powerhouses emerged in the region, which led to more intense competition for talent, trade and FDI. For Malaysia to remain competitive, it became clear that it needs to compete on value, not cost, and this requires a refocusing on getting the incentives right for innovation, creativity and entrepreneurship.

The comparison with South Korea is partly flawed and unfair. For one, South Korea did not need to manage the ethnic tensions Malaysia was facing given the differences in demographic make-up. Also, South Korea was clearly an exceptional success story that few countries around the world have been able to replicate. On the flipside, Malaysia’s economic performance cannot be underplayed either. Indeed, the Commission on Growth and Development identified Malaysia as one in only 13 countries around the world that has since 1950 registered over a period of 25 years or longer an average growth rate of more than 7 percent.

Leaving these caveats aside, the sheer difference in growth performance, as well as South Korea’s remarkable success in improving social outcomes, is nevertheless instructive. The comparison offers some insights on what Malaysia could have achieved, andmore importantly can achieve in the future. This characterization also lies at the core of the recent self-diagnosis undertaken by the Government of Malaysia. The New Economic Model, the Tenth Malaysia Plan and the Economic Transformation Programme all speak to the need to update Malaysia’s inclusiveness strategies so as to realign them with the objective of becoming a high-income economy.

The need to update Malaysia’s inclusiveness strategies reflects both new realities and new challenges. The new reality is that poverty is no longer the key issue when thinking about inclusive growth. Poverty still exists—and pockets of poverty remain deep and concentrated—but inequality is now in the spotlight and is presenting a tremendous challenge. The other new reality is that inequality is no longer what it was four decades ago. Nowadays over 90 percent of the level of inequality is explained by differences within ethnic groups rather than differences between these groups. Individual socio-economic characteristics, such as activity status, sector of employment, urban versus rural stratum, and educational attainment are now the capital explanatory factors, no longer ethnicity.

Malaysia’s high-income aspiration is also raising a whole new set of challenges. High-income economies tilt the demand for labor in favor of the skilled, sharpening income inequality across the skills spectrum. They tend to specialize in product niches and concentrate activity in narrow geographical clusters, raising challenges to retrain people and move them around to where the new jobs are. They are also open to competitive forces, creating challenges for those who are unable to compete or unlucky as a result of such competition.

The November 2010 issue of the Malaysia Economic Monitor, which we are publishing today, offers an analysis of where Malaysia is today and where it could go tomorrow by updating its inclusiveness strategies. Our recommendations on this highly charged topic do not come out of the blue—they are based on a detailed analytical study of the latest household income, labor force, and enterprise surveys, which the authorities have made available to our team. We are also leveraging on the experiences of other countries around the world, who have addressed or are coping with similar challenges.

To fast-forward to the 2023 World Bank’s Malaysia Economic Monitor where the agency is strongly advocating digitalization of a new economy frontier (though critiques are that neoliberalism is modern imperialism assuming a new identity) promoting infrastructural platforms to cater for Global North monopoly-capital, but even then, there are resource limitations and social constraints that could, again, likely pull back the country’s ability and capacity to progress; simplified, it is primarily due to:

a) The lack of financial resources and digital skills have been cited as key constraints towards digitalization;

b) Even smaller formal firms relied on more traditional methods of payment, especially cash; and

c) Vulnerable segments of the population remain unbanked, despite the expansion of digital financial services.

These other matters pertinent to the national digitalisation process and an e-commerce economy shall be explored, and be expanded, in subsequent articles with differential dimensional approaches recommended to be undertaken when aiming for The Big Push.

For a long time it seems – more than two decades – since Olin Liu’s IMF Report is there a structural approach to national economic development that is more strategic and formative in dealing with politico-economic realities faced by the nation in totality.

An analysis on a previous attempt in structural reform under a stagnated economy was explored HERE.

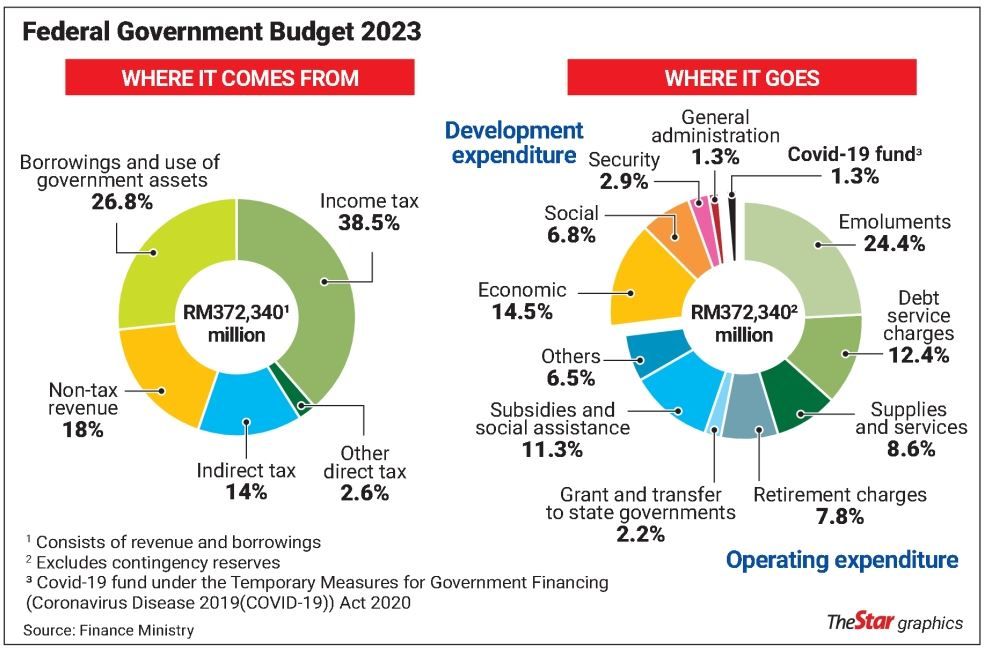

1] THE BUDGET 2023 will allocate RM388.1 billion for spending, of which RM289.1 billion is for operation expenditure and RM99 billion for development expenditure – once again amplifing the dire direction state of nation is heading. Only 25% in budgetary allocation is devoted to sustain developmental endeavours, whereas three-quarters of expenditure are to service day-to-day operations or for every ringgit, 75 sens go to maintain and retain the civil service sector and its pensionable remunerations.

[In the 1960-70s, nearly half of a National Budget is devoted to development purposes towards long-term returns on investment, covering widely upon education, socio-economic services and the health segments]

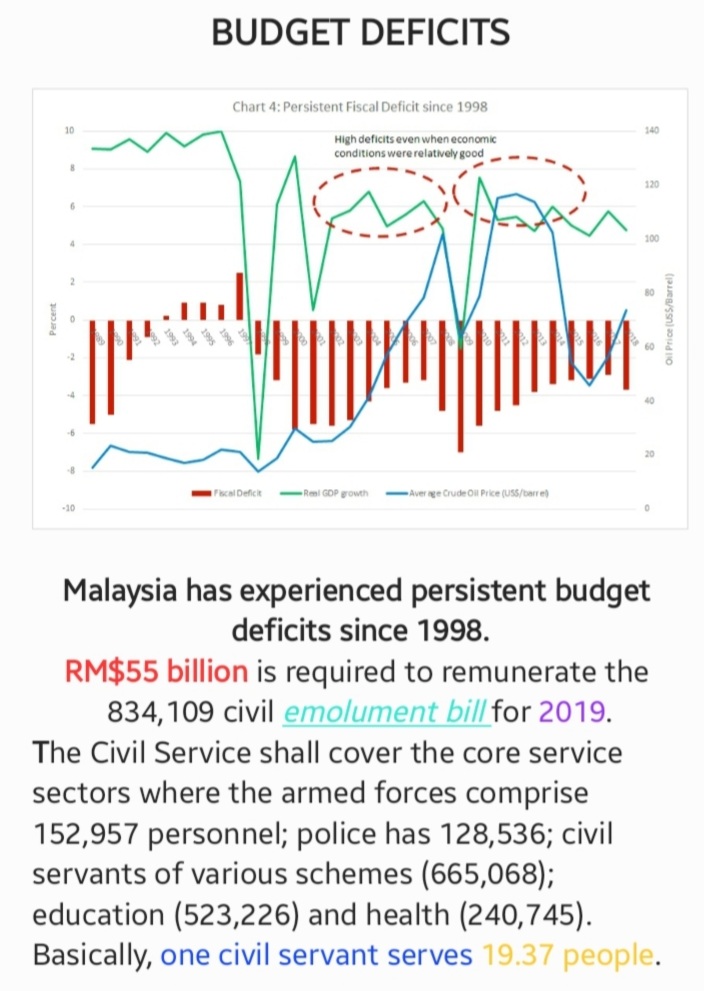

Whereas, nowadays, the national debts are increasing as a resultant outcome of continous high operation expenditure with consistent budget deficits since 1998:

The public sector, through the decades supporting the dastard nature of kleptocractic practices, has not met the performance criteria deemed a necessity to spur economic development, but furnished as an intermediary medium between political master and to rentier capitalism in vested projects’ implementation. Some elements have even aligned with the political kleptocrats and clientele capitalists in helping themselves in gorging unfetted gains.

Not infrequent harsh critique of an ethno-administrative regime is the poor performance of the civil service, its sluggish deliverance of public goods and services, slackness in work productivity, and widening misuse of public funds – as observed by the World Bank consultation teams:Over the years, various efforts have been undertaken to improve public sector productivity in Malaysia, but not unsurprisingly, with limited resultant outcomes. Core difficulties often lie in translating researches on public sector productivity findings into policy actions. The elements constraining effort on improving public sector performance centre on administrative human-resource incapacity, a broadbase corruptive regime with burden of privileges mentality, a lost community soul living in a society laced with serial systemic odious practices, including money-laundering, (read icij, Panama Papers).

The Pandora Papers exposè only widen the mired state of nation politico-economic praxis wherein RM$1.8 Trillion is siphoned abroad by corrupted compradore capitalists and their clientel ethnocapital; this amount is even more than the national debt of RM$1.5 Trillion in 2022!

Singapore has one time or another has a SG$1.57 Trillion in sovereign reserve while Norwegian Sovereign Wealth, accumulated since exploitation of North Sea oil – about the same time that Malaysia started exploration of oil and gas off South China Sea – is a stacked US$1.2 Trillion.

Thus, the country has an outsized public sector which is imperfect in its non-productiveness (reference: World Bank (2019), Malaysia Economic Monitor: Re-energizing the Public Service).

All the above issues are aided and abetted by neoliberalism capital endowment in the guise of foreign advisors to dash any hope of an indigenous contribution to proper economic development but an economic growth praxis that engulfed a state of nation crises after crises with subservient subsidies mentality and those consistent provision supports that inhibit an alternative mode in uplifting the development of a country.

2. THE REVENUE for 2023 is projected to be RM$291.5 billion compared to RM$294.4 billion last year; the nearly +RM$90 billion shortfall is to be covered by debts financing and dividends from Petronas and Khazanah, plus tax base which is already too pit-bottom shallow. (The T20 segment makes up 80% of Employees’ Provident Fund (EPF) contributions; out of 16-million workers, only 2.5 millions are tax-payers).

The deferment in implementation of the capital gain tax and a wealth tax until 2025 only indicate the preference to capital interests than immediate rakyat-rakyat beneficial wellbeing. There is a definite need for reforms towards long-term fiscal sustainability if governance is committed to improving the credibility of the fiscal policy conduct and framework through more holistic reforms which should include revenue enhancement measures and subsidy rationalisation programmes while maintaining macroeconomic stability and safeguarding the wellbeing of the rakyat.

Unfortunately, the social assistance allocation of RM$8 billion to cover the needs of 8.7 million people will amount to a paltry RM$920 per person per annum, (theedgemarkets, 27/02/2023).

Listen to Treasury Secretary General Datuk Johan Mahmood Merican on the thought process that went into drawing up the budget HERE.

3.THE ECOFOOD SECURITY issue is inadequate in tackling daily bread-and-butter problems by not prioritising the maintenance of open and operational food supply chains. Equally in importance is to address other looming threats to food security including climate change that is already damaging food production as temperatures and precipitation patterns fluctuate. Further, the wide-spread urbanisation has caused a proportionate decline in the agricultural labour force as the current cohort of farmers age and fewer young people are interested in taking their place.

Therefore, the country’s land-use practices in catering large-scale agribusiness and real-estate development are unsustainable, especially with introduction of considerable imminent deforestation, loss of biodiversity, and chemical pollution.

Given these challenges, agricultural research and development (R&D) must be a core component of any national food security policy. Climate-focussed research is also needed to develop the various crop varieties that are tolerant against a more uncertain climate and extreme weather events. More appropriately – in any quadrilateral helix operational approach mode (with distinctivearticulated strategic goals) – there is a need for a strategic reorientation in the ability to resolve present and future food scarcity by collaborating with international bodies and countries to mitigate the ecofood insecurity issue, (BowerGroupAsia, 2023).

4] THE NATIONAL DEBTS shall slow the economy growth path for many years to come; it could likely be seized upon by the oppositions ahead of state polls and could dilute the credibility of the Anwar governance, so said BowerGroupAsia senior analyst Arinah Najwa.

Further, economists do not expect the nation’s strong economic growth witnessed in 2022 to continue into 2023 as consumer pessimism weighs significantly on growth which is affected by Global North consumption patterns and the cosmopolitan centres’ inflationary trends. Indeed, many economists believe that domestic consumption will slow significantly by end-2023 due to cumulative inflationary pressure, the waning effect of the Employees Provident Fund’s special withdrawal scheme that was imposed in April 2022, and the expiry of the car sales tax exemption. This could be further impacted by the government’s potentially more restrictive spending as operational expenditures enlarged, (see the report in FitchSolution in Appendix).

For 2023, UOB Kay Hian Research foresees gross domestic product growth halving to about 4 per cent due to a slowdown in domestic consumption in the country in alignment with IMF’s projection. Under the Medium-Term Fiscal Framework (MTFF) 2023-2025, total revenue in the medium-term is projected at RM854.3bil or 14.7% of gross domestic product (GDP), mainly contributed to non-petroleum revenue which is estimated at RM699.5bil or 12% of GDP.

The fiscal policy in 2023 will definitely need to maintain agility, supporting the growth momentum towards achieving the national development agenda. The fiscal resources have to be channelled through a more targeted approach and allocated in priority areas, particularly to enhance economic capacity and country’s competitiveness.

While the government’s budget remains expansionary to provide sufficient fiscal support in ensuring the rakyat’s well-being, the continue undertaking of premier economic reforms has to be sustained to maintain the fiscal consolidation plan. This is more vital since the Federal Government’s revenue collection in 2023 is projected to be lower at RM272.6bil or 15% of GDP due to anticipated lower non-tax revenue collection. The non-tax revenue is expected at RM$67billion, declining 23% from 2022 due to lower dividends from government entities.

A positive way is to emphasis more on the quality and multiplier effects in creating high quality jobs and building key ecosystems to help the development of local capitals and specifically SME entrepreneurship players.

The SMEs are the backbone of Malaysian economy:

The small and medium enterprises (SMEs) make up 99% of the 920,624 business establishments in Malaysia. In 2018, SMEs employed 66.2% of the workforce in Malaysia, contributing RM$522.1 billion, or 38.3%, to the Malaysian GDP. They are classified into three categories: micro, small, and medium, defined by industry, sales turnover, and the number of employees. Micro-enterprises make up 76.5% of Malaysian SMEs. In contrast, medium-sized enterprises comprise only 2.3% of SMEs.

Despite being the backbone of Malaysia’s business environment, “SMEs perform relatively poorly in digitalization. There exists a digital divide among businesses in Malaysia”, write Amos Tong, an economics undergraduate at UCLA, and Rachel Gong, a researcher at the Khazanah Research Institute in Kuala Lumpur. This owes to the fact that the larger pool of micro-SMEs entrepreneurs are marginally unskilled and too underfunded in their enterprises’ administration and daily operations; compounded that there are much to do Catching Up: Inclusive Recovery and Growth for Lagging States in Sabah and peninsula Malaysia which needs wider spread-effect from economic development, (World Bank, 2022).

Related to the bigger picture is the question as to in what ways can the SMEs contribute to the industrial development programme in the country.

How would the New Industrial Master Plan 2030 in the third quarter of 2023 shall emerge has a bearing on cementing the future industrial platform of a nation and what intermediary roles would the SMEs play in the commodity supply (and value) chains?

Shall we revisit the E&E sector to tap upon the peripheral benefits in the West vs China-Korea-Japan Chip War? or we might got submerged within the geopolitical trade-technology warfare?

Can we generate the next generation of New Gen armed with TVET, but without adequate polytechnic knowledge nor polycrisis management skills to confront future geoeconomic scenarios?

Owing to the diverse array of activities in SME and different genres of entrepreneurship, whatever assistance offered may not be enough to aid this vital segment of the national economy. LISTEN to Chin Chee Seong, National Secretary General of the SME Association of Malaysia on his takes.

In the Malaysia Economic Monitor, February 2023, the World Bank is rather persistence in advocating the advancement towards a digital economy. Though while advocating Big IT development as a means of continuing capital deployment – and capital accumulation with extracted value from states – to ensure Global North infrastructural platforms Big Tech benefiting on expansive exploitation, through global labour arbitrage where underemployed labour is truly exploitated, (readSTORM, 2022, Big Tech Large Gig), and STORM 2023, Big Tech in Marine Cabotage where the infrastructural platforms could hold our nation to technical ransom on undersea communication cabling installation and maintenance.

Indeed, the large RM$1.5 billion IT allocation will benefit only wealthy and the well-connected companies – not our local SMEs entrepreneurs – with their huge expenditure for consultancy pservices.

It also highlights the longer term on how to rebalancing towards deregulated finance and foundational service sectors (like infrastructural platforms which are incrementally becoming invasive as techno-feudalism in country) franchised by privatisation and outsourcing to Global North monopoly-capital whereby compradore capital accumulates their capital as functioning intermediaries.

A good prospect is to spur local start-ups, government-linked companies including Khazanah Nasional Bhd and EPF in investing RM$1.5 billion for those that are innovative and have high-growth potential. This model will see a lead company (not as yet identifiable, but capital shall continue to dominate as Jomo observed in a French Embassy-sponsored forum) that shall partially or fully take over the operation of TVET institutions and revamp training programmes so that they meet industry needs: provisio it is free from identity politics but based on Madani politico-economics mantras.

Inheriting such a burgeoning debt burden, sovereign wealth fund Khazanah Nasional Bhd could sell its assets to raise cash for the state of a nation as she is sitting on assets easily worth more than US$30.5 billion (December 2021) that could probably raise over 10% of the government’s +RM$1.5 trillion debt and contingent liabilities.

Another financial resource bulwark is with Petronas as it is financially in a comfortable position to pay, given that its total assets has strengthened to RM$699.5 billion in the first half of 2022.

Alternatively, government-linked companies (GLCs) and government-linked investment corporations (GLICs) would also likely be encouraged to pay higher dividends. The government could tap these state enterprises to help out just as like the recent RM$58 billion stimulus package to counter impact of the Covid-19 pandemic 2020 crisis. The GLCs and the crown-jewel GLICs have to be reformed to endow the national coffers.

An excellent yet viable alternative foundation is the formation of a newsovereign fund to be created with Khazanah and Petronas seedings.

The debt financing of a national economic development shall demands certain structural changes, (see Appendix B). The mere fact that much resistance to change by clientel-capitals to inhibit every rakyat-rakyat to have a share of the common wealth only befalls the stake – and sake – of a nation.

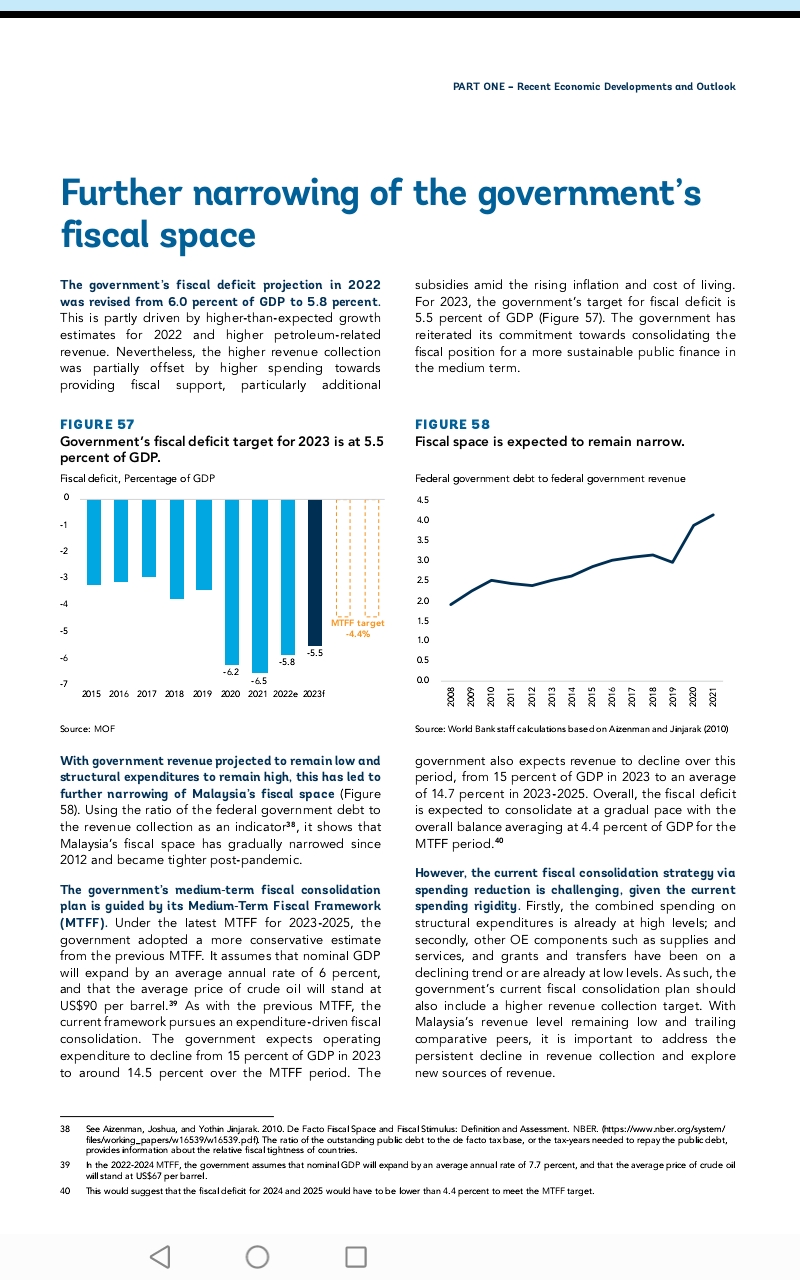

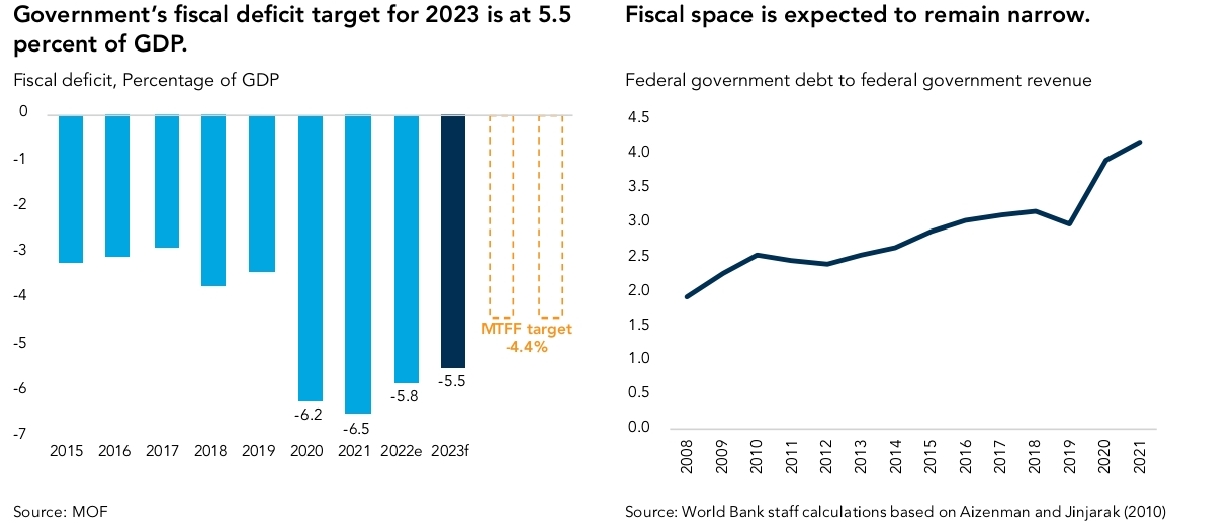

With government revenue projected to remain low and structural expenditures still increasing high, this has led to further narrowing of Malaysia’s fiscal space (see right chart below):

Using the ratio of the Federal Government Debt to the revenue collection as a reference point, the World Bank has indicated that Malaysia’s fiscal space has gradually narrowed since 2012 and became tighter post-pandemic.

The government also expects revenue to decline over this period, from 15 percent of GDP in 2023 to an average of 14.7 percent in 2023-2025. Overall, the fiscal deficit is expected to consolidate at a gradual pace with the overall balance averaging at 4.4 percent of GDP for the MTFF period.

The current fiscal consolidation strategy – via spending reduction – is, to many national economists and political analysts, (bfm.my, IDEAS, O2 Survey, theedgemarkets), rather challenging, given the current tight spending domain. Firstly, the combined spending on structural expenditures is already at high levels; and secondly, other Operating Expenditures components such as supplies and services, and grants and transfers have been on a declining trend or are already at low levels.