The International Monetary Fund (IMF) has revised the outlook for Malaysia’s real gross domestic product (GDP) by a notch to 4.4 per cent this year from its earlier prediction of 4.3 per cent, (IMF 17 Apr 2024), whilst Bank Negara Malaysia projects 4%-5% GDP growth in 2024 when global growth is expected to rebound in 2024, driven by the technology upcycle, tourism recovery, and low base effects in 2023, (Bank Negara in its annual report released on 20 Mar 2024), primarily underpinned by continued expansion in domestic demand and improvement in external demand.

The IMF growth estimation for the country is based on its World Economic Outlook, April 2024 which is to be Steady but Slow: Resilience amid Divergence. That the baseline forecast for the world economy is to continue growing at 3.2 percent during 2024 and 2025, at the same pace as in 2023. Also, it is based on an expect real (inflation-adjusted) U.S. economic growth of about 2% in 2024, higher than its initial estimate of about 0.5%.

II YEAR 2022 GLOBAL

The present year has a better forecast than whilst in the midst of the COVID-19 pandemic year of 2022 when there were many encountered economic turbulences.

The first headwind is a global financial tightening. The Federal Reserve was then much more aggressive in tightening monetary policy as U.S. inflation remained stubbornly high. This was translated to tighter financial conditions for Asia. Sovereign yields had also risen, and capital outflows in emerging market Asia leaked as voluminous as in past stress episodes, even though they remained limited to a few economies.

The second headwind was the continuing conflict in Ukraine, which inevitably led to a spike in commodity prices. Most countries in Asia had also seen a deterioration of their terms of trade. This situation was an important factor behind currency depreciations insofar as in 2022.

The third headwind was the sharp and uncharacteristic slowdown in China. The IMF have had thus marked down Chinese growth for 2020 with 3.2%, its second lowest level since 1977. This reflected the impact of the zero COVID lockdowns on mobility and the crisis in China’s real estate sector. The slowdown was then estimated to have important spillover to the rest of Asia through trade and financial links. Zee

During the 2022, the headwinds were contributing to a global slowdown compared to the April World Economic Outlook. As such the IMF has had downgraded its forecast for growth in Asia and the Pacific by 0.9 percentage points in 2022 and 0.8 percentage points in 2023. So, the growth was at 4% in 2022 and 4.3% in 2023 while inflation grew more modestly in Asia in 2021. This change follows the sharp volatility in global commodities since the war in Ukraine. This increase reflected both rising food prices, particularly in Asian emerging market and developing economies, but also higher core inflation as region recovered and output gaps had loss. Indeed, core inflation had once again exceeded central bank target in most Asian economies and in most cases by a wide margin. It was argued that there should be a need for further tightening of monetary policy to ensure that inflation returns to target, and inflation expectations would then remain well anchored.

At that time, it was expected that fiscal policy would have to complement monetary policy to fight inflation around the world in Asia. Fiscal consolidation was also advised to be incorporated to stabilize public debt. Asia is now the largest area in the world and so comes at high risk of debt. It was further felt that distress positions and rising interest rates could possibly pose financial volatilities from high leverage and unhedged balance sheets and further risks increases in public debt ratios.

The challenging conjuncture then was aggravating the medium-term economic scars opened by the pandemic, which was expected to be aggravating worsen in Asian. Also, it was assessed that much of the shortfall in growth in Asia relative to other regions could be further explained by lower levels of investment, employment and productivity following the pandemic. While exact policy responses at that 2022 period would expected to depend on country specific circumstances, tackling corporate debt overhang and mitigating human capital losses would also be important for a wide range of countries in the region.

During this period, the prospect of greater geo-economic fragmentation was also a significant risk to the region. In the report, it was stated that worrying early signs of fragmentation and consequences of a destruction of global trade links. One such sign of fragmentation pressures emerged from the crises was elements of trade policy uncertainty. In fact, the spiked in 2018 amid tensions between the United States and China and had further accentuated amid Russia’s trans-border war in Ukraine as sanctions created uncertainty around future trade relations. The IMF analysis at that time had indicated that a typical shock to trade policy uncertainty like the 2018 build up of China-U.S. tensions somewhat reduced investment in the region by about 3.5% after two years. It had also projected a decreased gross domestic product by 0.4% and raised the unemployment rate by 1 percentage point.

In addition to rising uncertainty, the prevalence of harmful trade restrictions was stated to have increased since 2019. The sectoral decomposition of trade restrictions had also been shifting. The shared restrictions that target high tech sectors had also been steadily increasing since the global financial crisis. Since the war in Ukraine, restrictions targeting the energy sector had also increased sharply, while those aimed at high tech sectors had also remained high. During that period, the IMF team had considered the long-term risks of deeper fragmentation scenario, and as such have had articulated the consequences of a purely hypothetical global economy divided along the lines implied by the votes cast on March 2nd, 2022 United Nations General Assembly motion to condemn Russia’s invasion of Ukraine. It was evisaged then if the world would to be demarcated into two separate blocs, then the losses could become significant. Global losses were then expected to be of 1.5% of GDP. Whereas, those in Asia were slightly over 3%, with losses forseen to be especially large for countries with a high level of openness and that have production structures that straddle both blocs.

III 2025 FUTURE

The IMF has earlier raised this year’s gross domestic product growth outlook for the region to 4.5% from the previous 4.2% estimated in October, with China’s figure upgraded by 0.4 percentage point to 4.6%.In the latest regional outlook released, the IMF pointed out that fiscal stimulus enacted over the past several months helped buoy the economy. It added that its China growth forecast for 2024 “may be revised upward,” as the country’s first-quarter growth came in stronger than expected. But it warned of several challenges for Asia’s largest economy. “Chief among risks for Asia’s economy remains a protracted property sector correction in China,” it said in the report, expressing concern that this may weaken demand and make continued deflation more likely. In addition, the IMF raised the issue of industrial overcapacity weighing on industries from steel to automobiles recently. “Policies that boost supply, such as investment subsidies to specific companies and industries, would worsen overcapacity, reinforce deflationary pressures, and potentially provoke trade frictions,” the IMF said. China’s official purchasing managers’ index released had shown the country’s manufacturing activity grew for the second consecutive month in April.

As for Malaysia’s outlook, in its latest World Economic Outlook (WEO) entitled Steady but slow, resilience amid divergence, IMF predicted the GDP growth to remain at 4.4 per cent in 2025. It projected Malaysia’s current account balance at 2.4 per cent in 2024 and 2.7 per cent in 2025.

By ensuring such growth prospects

Characteristic Gross domestic product:

2025: US$477.83 B 2024: US$445.52 B 2023: US$415.57 B 2022: US$407.03 B

would be determined by the GDP growth in the United States which is projected to be 2.6% in 2024, before slowing to 1.8% in 2025 as the economy adapts to high borrowing costs and moderating domestic demand. According to Wang and Tyler, the economic data should “give more confidence that the US economy is recovering in additional sectors” and that “recession fears for 2024 are likely to be pushed into 2025.” On the other hand, GDP in China is expected to reach 18825.00 USD Billion by the end of 2024, according to Trading Economics ( TE) global macro models and analysts expectations. In the long-term, the China GDP is projected to trend around 19673.00 USD Billion in 2025 and 20617.00 USD Billion in 2026, according to TE econometric models.

On Malaysia, the stock market rallies in early May 2024 has given a momentum to the country’s economic wellbeing.

Malaysia’s FBM KLCI climbed to a two-year high on 7th May 2024 as gains of consumer and banking stocks extended the benchmark index’ rally to its fourth straight day.

The KLCI rose as much as 12.93 points or 0.8% to 1,610.32, its highest since May 5, 2022. The index closed at 1,605.68, still up 8.29 points or 0.52%, with 24 out of 30 constituents posting gains.

These gains also propelled Malaysian stocks’ market capitalisation to RM2 trillion in for the first time ever. The gains appear sustainable and on track to hit 1,755 by the end of this year, CGS International has stated. The aggregated 12-month target for the KLCI stands at 1,683 points where Bloomberg data have indicated.

By paying more attention to domestic-driven sectors, it is expected that the domestic economy will be picking up with an improved growth regime in both private consumption, and more importantly better gross fixed capital formation in the country’s economy.

Further, on the the 50th anniversary of diplomatic ties and foster deeper economic collaboration between Malaysia and China, it is envisaged that with the Malaysia’s Madani initiative, launched in January 2023, aligning with the values and principles of the Community Shared Future (CSF) advocated by President Xi Jinping since 2013, Malaysia foresees significant potential for deepened collaboration with China, notably in infrastructure, the digital economy, green development, new energy vehicles, and the rare earth industry – whereby and thereby, the Malaysia Madani economic framework will be able to strengthen her national competitiveness by focusing on fiscal sustainability, excellent governance, and effective service delivery thenceon by 2025.

collated and compiled by the Collective on Geoeconomics

12/04/24

INTRODUCTION

KS Jomo and Ngongo have expressed that since the 2008 global financial crisis, developing nations have to borrow massively from private finance – at exorbitant interest rates – to scale funding up ‘from billions to trillions’. Indeed, servicing external debt now blocks progress whereby governments have cut back spending in line with conditions or advice from powerful foreign economic agencies as such. Onset with the global debt crisis in 1979 the transition and developing Global South economies had paid cumulative US$7.673 trillion in external debt service, seePaulo Nakatani and Rémy Herrera.

In fact, the external debts of developing and transition countries reached 29% of their GDP in 2019. The short-term debts rose to more than one-quarter of the total external debts alone.

The Global South debt even then during the same period has increased from US$618 billion in 1980 to US$3.150 trillion in 2006, according to figures published by the International Monetary Fund (IMF). The external debt of this group of countries, comprising 145 member states, will continue to grow throughout 2007, according to the IMF, to more than US$3.350 trillion. The debt of the Asian developing countries alone could rise to US$955 billion, even though they have already repaid, in interest and capital, far more than the original amount due in 1980!

Malaysia 2019 external debt was RM$231225.9 million, (Asia Development Bank, External Debt Outstanding in Asia and the Pacific, Asian Development Outlook, April 2020).

According to a report to the Asian Development Bank, in September 2020, by Donghyun Park, Arief Ramayandi, Shu Tian stating inter alia that borrowing heavily for fiscal stimulus packages to support growth and provide relief for vulnerable groups whilst at the same time, private companies and households may be forced to borrow more to survive the economic impact of COVID-19…..In addition, the economic downturn challenges their capacity to service their existing debts. Therefore, despite widespread concerns about the current escalation of public debt and its sustainability, we should not lose sight of the potential risk from possible surges of private debt…..

Coupled with a weakening economy, already, as late as July 2023, a IMF Report has projected that under its baseline forecast, growth will slow from last year’s 3.5 percent to 3 percent this year and next – a 0.2 percentage points. Our MIDF Research data have maintained its forecast that Malaysia’s GDP growth would moderate at 4.2% in 2023 (2022: 8.7%), weighed down by uninspiring external trade performance as real export of goods is predicted to contract by 2.8% (2022: +11.1), reflecting weakness in regional and global demand.

Furthermore, the national household debt-to-Gross Domestic Product (GDP) ratio had already surged to a new peak of 93.3% as at December 2020 from its previous record high of 87.5% in June 2020, according to Bank Negara Malaysia (BNM).

Malaysia National Government Debt reached 255.4 USD bn in Dec 2023, compared with 246.4 USD bn in the previous quarter. Malaysia Government debt accounted for 64.3 % of the country’s Nominal GDP in Dec 2023, compared with the ratio of 63.8 % in the previous quarter; seecsloh, Destined to Debts.

We shall define the Global debt as borrowing by governments, businesses and people. Presently, it is at dangerously high levels. In 2021, global debt reached a record US$303 trillion, a further jump from what was record global debt in 2020 of US$226 trillion, as reported by the International Monetary Fund (IMF) in its Global Debt Database,21 Dec 2023.

The IMF must do more to support low-income countries and fragile states, Managing Director Kristalina Georgievasaid on Tuesday at the Center for Global Development (CGD).

Speaking with Masood Ahmed, CGD President, Georgieva called for the Fund to be more representative of the global economy, with a better balance between advanced economies and the voices of emerging and developing countries. She also expressed the need to help countries build resilience to a more shock-prone world.

Georgieva said she sees two equally important tasks for the Fund: “To ensure that we have the financial capacity to operate, and support vulnerable middle-income countries and low-income countries……And to bring our membership together….Despite all the difficulties in cooperation, we will work towards consensus on those issues on which the future of our children and grandchildren depend,” Georgieva said. She also explained the IMF’s role in its work on climate.

During a subsequent conversation with World Bank Group President Ajay Banga at an event on support for low-income countries, Georgieva shared more of the Fund’s thinking. For low-income countries to reduce vulnerabilities and achieve a sustainable and meaningful rise in income levels quickly, it will take the countries themselves to do more to build the strength of their economies, and the international community to be a reliable partner, she said.

“We see that those [countries] that are doing better are countries with strong institutions, rule of law, transparency, and less corruption, and building those strengths is something no one but the countries can take on.”

Domestic laws need updating to ensure that public obligations are transparent

April 2, 2024

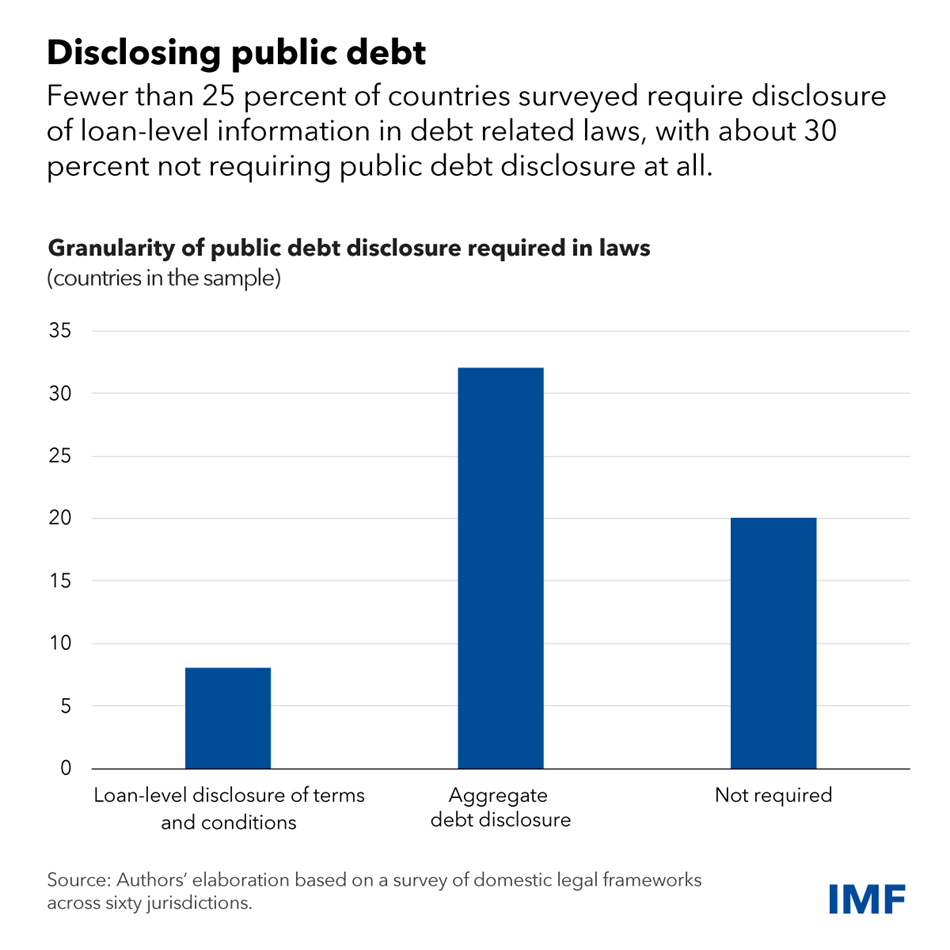

If efforts to address record global public debt are to leave no stone unturned, then weak disclosure laws warrant deep scrutiny. Hidden debt is borrowing for which a government is liable, but which is not disclosed to its citizens or to other creditors. And while this debt—by its nature—is often kept off the official government balance-sheet, it is very real, reaching $1 trillion globally by some estimates.

While these undisclosed obligations are not large when compared to global public debt topping $91 trillion, they pose a growing threat to low-income countries, already highly in debt with annual refinancing needs that have tripled in recent years. The problem is even more pressing amid higher interest rates and weaker economic growth. Accountability, too, is imperiled without accurate information about the extent of borrowing, which heightens the risk of corruption.

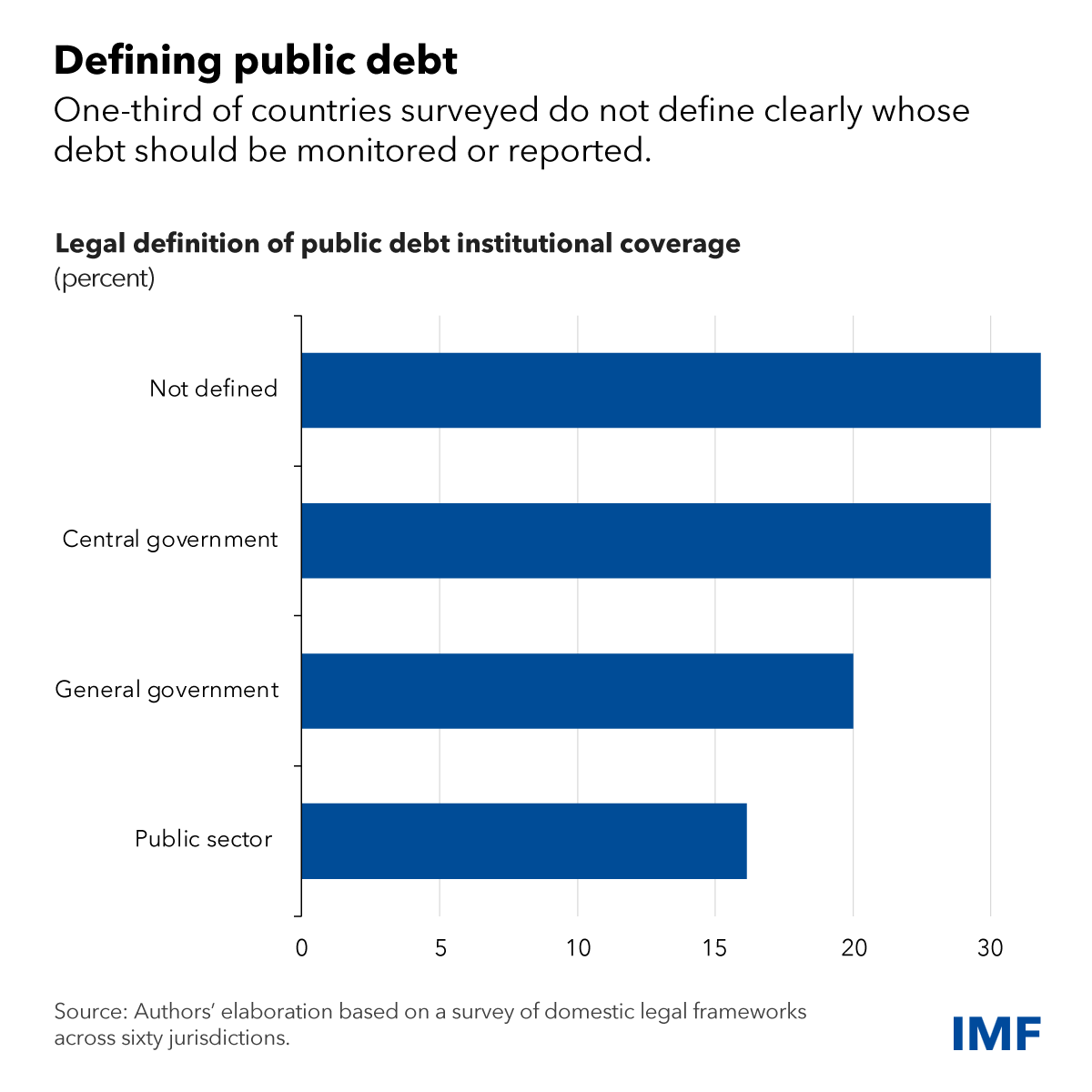

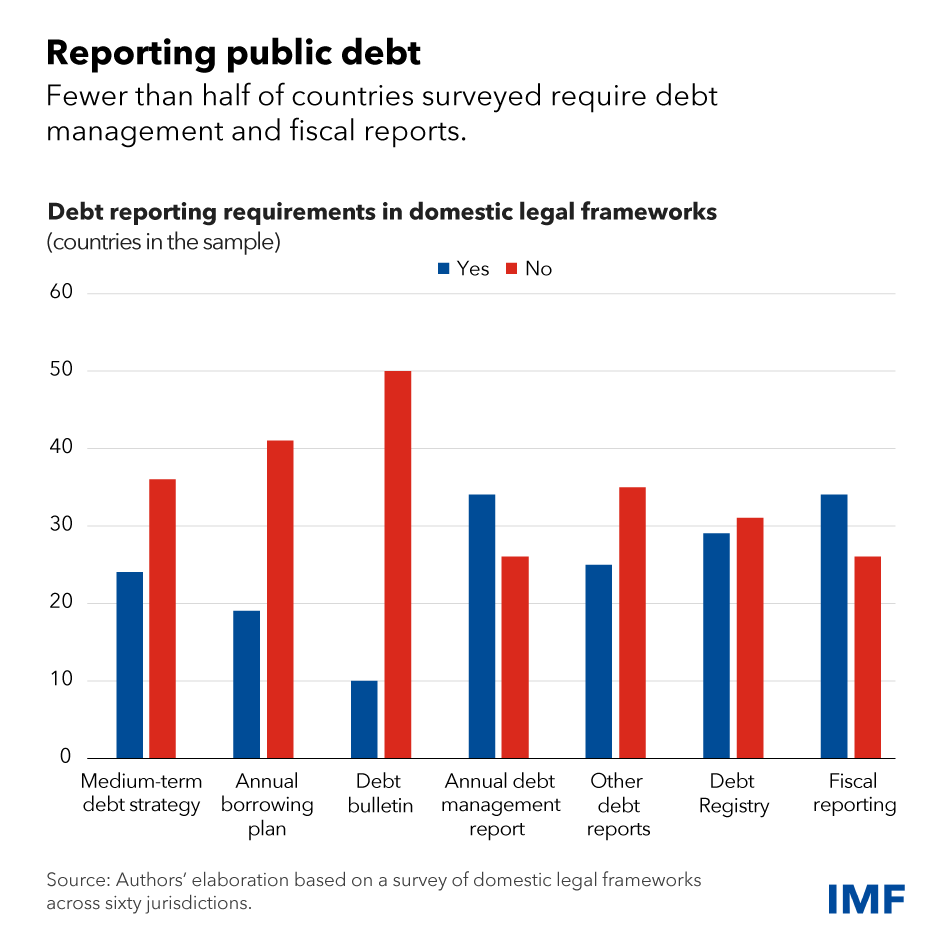

Building on a July 2023 paper, our new research shows that fewer than half the countries surveyed have laws that require debt management and fiscal reports, while less than a quarter require disclosure of loan-level information—key legal features for facilitating transparency. We also identify four noteworthy vulnerabilities in domestic laws that enable debt to be hidden: a narrow definition of public debt, inadequate legal requirements for disclosure, confidentiality clauses in public debt contracts, and ineffective oversight.

Definition

In many countries, a narrow definition of public debt, in one or in multiple laws, permits some forms of sovereign debt to escape oversight. We recommend that the definition of public debt be broad and comprehensive, meaning that it should capture arrears, derivatives and swaps, suppliers’ credit, and assumptions of guarantees as well as loans and securities. The definition should also cover extra budgetary funds, public trust funds (pension funds, for example), and special purpose vehicles.

A good example is found in Ecuador, which pursued legal reform in 2020 to ensure that short-term financing instruments—such as securities or treasury paper with terms of less than one year—were included in debt calculations and statistics. Other good examples include the legal definitions used in Ghana, Jamaica, Rwanda, Thailand and Vietnam, all of which encompass multiple types of debt instruments.

Disclosure

Second, across the globe, legal requirements for debt disclosure are inadequate. A strong legal basis is crucial to signal that there is a clear requirement to report debt data in a manner that is both timely and relevant for policy analysis, transparency and accountability. Strong reporting laws are found in in Benin, Kenya and Rwanda, which define both public debt reporting requirements and the timeframes for these reports.

Confidentiality

Confidentiality in public debt contracts directly hinders transparency. Across the globe, few laws regulate (and limit) the confidentiality of public debt, which hands policymakers wide discretion to label such contracts confidential for national security or other reasons. This is exacerbated by the fact that current debt-related international standards and guidelines provide limited guidance on how to tackle confidentiality issues.

We recommend that the law tightly define exceptions to disclosure and the scope of confidentiality agreements. Legislative oversight and other safeguard mechanisms such as administrative or judicial remedies should also be spelled out in the applicable legal provisions. Laws in Japan, Moldova and Poland are among the few that authorize legislative or parliamentary oversight of confidential information.

Oversight

The disclosure of public debt may also be inhibited where there is ineffective oversight governance by legislatures and supreme audit institutions (national government audit institutions), which are all important guarantors of accountability. Legislative bodies must be able to monitor and scrutinize public debt on behalf of the people, and they need to have staff able to read and grasp highly technical reports.

Several legislatures have a committee system—such as committees on the budget and public accounts—which allows for specialization among legislators. An example is in the United States, where the Treasury Secretary is required by law to send the annual public debt report not to Congress as a whole, but to two specific committees—House Ways and Means and Senate Finance. We also recommend that laws provide supreme audit institutions with the authority and the necessary powers to monitor and audit government debt and debt operations.

IMF role

Debt transparency not only benefits countries directly, but it is also essential for the work of the IMF. Hidden and otherwise opaque forms of debt make it more difficult for the Fund to fulfill its core mandate in a number of ways. For example, collateralized loans, novel and complex forms of financing, and confidentiality agreements make it difficult for the IMF to accurately assess a country’s debt and help bring its economy back on track.

Thus, the Fund works to bring the benefits of debt transparency to countries directly through technical assistance and also addresses the issue in our program engagements.

Well-designed laws make it harder to hide debt. But there are not enough of these laws on the books, despite their demonstrated benefits. Given the critical importance of getting transparency right, countries and their international partners must push for reforms to improve domestic legal frameworks, which in turn benefits both borrowers, legitimate creditors, and the system more broadly. Turning stones has never been more important.

— Kika Alex-Okoh contributed to this blog.

ADDENDUM

By way of confronting China with the peak paradigm by dispelling “Peak China” myths and affirming China’s development trajectory (john ross; Habib al Badawi; the diplomat; CfR; The East is Rising, the West is Declining {东升西降}) is much a discourse that China only wants to export its labour, that China only wants to grab the world’s resources, etc., and is engaged in debt diplomacy suppressing emerging economies in their development endeavours. The Johns Hopkins University’s China-Africa Research Initiative website has exceedingly valuable statistics and reports and blogs about this matter; this site also has a discussion on the China Trap Diplomacy whereas PRC firms are being told to reduce their financial exposures in overseas jurisdictions that could move to seize assets; and there is a good roadmap since the seizures of Russian assets after the invasion of Ukraine; readCounter Sanction Strategies that China Can Learn from Russia,Ding Yifan; Countering Western Sanctions, Yi Yan.

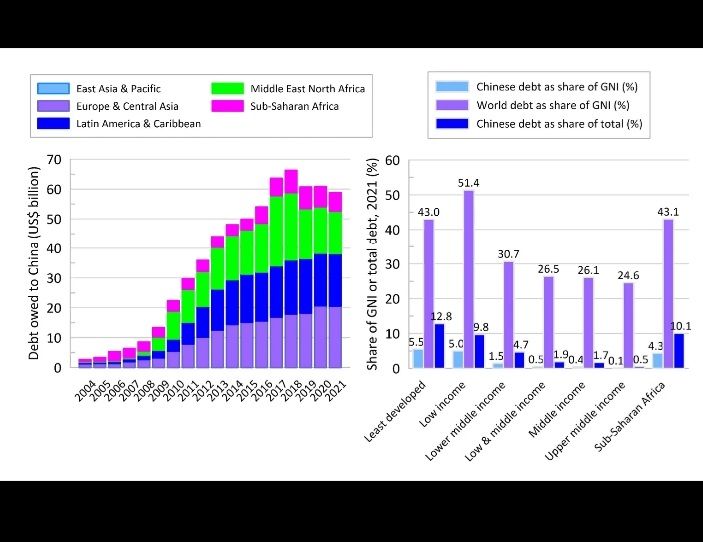

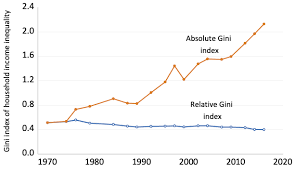

Looking at the chart below:

This chart actually plots Chinese credit, so it’s the debt of the rest of the world, the developing world, to China. And the chart on the left simply indicates the way in which debt owed to China has, of course, increased over the course of time as a result of Chinese development assistance and China’s lending, especially to parts of the Global South; readRISE OF CHINA AND DEMISE OF CAPITALIST WORLD ECONOMY.

One of the very striking things about China is that a large share of its lending is, in fact, to very low income countries. It lends more to the least developed countries in the world than do the multilateral institutions and do the OECD group.

If you see the least developed countries, their total debt to the rest of the world is 43% of their gross national income, which is, nearly one half, a very substantial share. Of that debt, the share owed to China is only 5.5%. And Chinese debt amounts to 12.8% of the total.

China’s share of GNI is 4.3%, and its share of the total debt of sub-Saharan Africa is 10%. So these claims about a debt trap are, in a sense, simply do not stand up empirically.

Malaysia is at a juncture in its politico-economic path crashing into fractious politics headlong on an inequity route with an expanding B40 lower-income class, (mef.org 2023). The socio-economic situations are becoming precarious. This is because of a stagflation risk arising amid sharp slowdown in growth that is accompanied by an accelerated inflation runaway globally, (World Bank, Global Economic Prospects, June 7, 2022) as confirmed by the Bank of International Settlements in its Annual Economic Report, 26 June 2022, and amid subdued external demand could only edge up to 4.3% GDP in 2024 (World BankMalaysia Economic Monitor 2023), though Standard Chartered gave a favourable 4.8% of GDP; while the Madani Malaysia model is trekking slowly along an uneven economic development track that is strewn with global geoeconomic uncertainties and internal socio-economic instability.

Could and would the enlargement, and deepening, of the infrastructural platforms accompanying an artificial intelligence regime therein salvage the state of a nation or the adoption of such advance technology savages the country with further neo-imperial penetrative wounds while accompanying digitalised colonisation process?

I] INTRODUCTION

Standing at a crossroads of techno-capitalism and neo-imperialism, artificial intelligence (AI), with its potential promise though has profound existential problems to the Global South because advances in AI originated in wealthy nations of the Global North — developed in those countries for local users, using local data. Over the past several years, Columbia’sDanielBjörkegren and Berkeley’s JoshuaBlumenstock for Finance & Development have conducted research with partners in low-income nations, working on AI applications for these countries, users, and data. However, AI systems require investment in knowledge infrastructure, especially in emerging and developing economies, where data gaps persist and the poor are often, if not, always digitally underrepresented. Besides, developing nations typically ill-afford such expensive large-scale deep neural networks infrastructure using expensive AI-driven application software.

Afterall, Artificial Intelligence (AI) leverages computers and digital machines to mimic the problem-solving and decision-making capabilities of the human mind.

Frequently, the techno-optimism in the advanced economies (GoldmanSach 2023; and, according to a Bloomberg’s PwC Report, AI would boost the global GDP to US$15.7 trillion by 2030) is at odd with Global South economic development outcomes, (Daron Acemoglu Simon, IMF); where AI technology is in likelihood to destroying jobs and displacing workers, (Andrew Berg Chris, IMF); or where the building block for AI governance is weak (Ian Bremmer, Mustafa, IMF) on system design, project implementation and subsequent operational processes. Indeed, Artificial Intelligence could well widen the gap between rich and poor nations, (Alonso, Kothari and Rehman, IMF Blog Dec 2, 2020; IMF 2018).

Then, on this understanding, to duly acknowledge that in emerging markets such as India, where agriculture plays a dominant role, less than 30 percent of employment is exposed to AI. Brazil and South Africa are closer to 40 percent. In these countries, the immediate risk from AI may be reduced, but on the other hand, there may also be fewer opportunities for AI-driven productivity boosts, (Gopinath, Harnessing AI for global good).

Secondly, Silicon Valley corporations are taking over the digital economy in the Global South with little notice, or for those encouraged by the World Bank – but short-circuiting the rakyat2 – as in Malaysia,(WB 2021; MEM 2023), the domestic infrastructural platform ecosystems are already consolidated by the Global North monopoly-capital Big Tech, (STORM 2023). In case country South Africa, Google and Facebook dominate the online advertising industry, and are considered an existential threat to local media. Uber has captured so much of the traditional taxi industry that drivers have been petrol bombed in the “South African taxi wars”. Similar battles have broken out in Kenya, (al jazeera, 2019).

Netflix is not only pulling subscribers away from local television services, but are buying up content in Africa. While in India, Facebook was forced to cancel its “Free Basics” programme that gave the social media giant control over the Internet experience on mobile phones, she was able to retain its influence in countries like Kenya and Ghana.

This is known as digital colonialism where once former Colonial powers deployed their infrastructural domination in ports, waterways, and railroads across their vast empires, only that at present day neo-colonialism is continued through digital routers and data servers.

The digital infrastructural platforms are not unlike colonial ‘forward movement’ activities where lands are waiting to be discovered and conquered. Whoever gets there first, and holds fast and tight, shall get their information server-riches. The infrastructural platform kings (colonial-feudal lords) positions themselves above users (the colonised), and their data surfing activities (serfs’ farm cultivation), thereby giving them overwhelming privileged access (lordship) to record and retrieve (dictate and dominate) endusers (the serfs) as and when demanded (as surplus value expropriation) under an information-commodity chained monopoly-capital environment (via routers and cloud servers) .

Thirdly, tech capital flows unencumbered trans-borders where new ecosystem of digital platforms has emerged over the past decade that is transforming the very structures of capitalism. This new business model of large monopolistic digital platforms are capable of extracting immense amounts of data overwhelming legacy enterprises and suppressing labour empowerment, (seePaul Langley and Andrew Leyshon, 2020). This is “netarchical capitalism” , where infrastructure is “in the hands of centralized privately owned platforms”, (Nick Srnicek, Platform Capitalism, 2017).

Information and infrastructural platforms have empowered a new kind of ruling class. Through the ownership and control of information, this emergent class dominates not only labour but capital. It is not just tech companies like Amazon and Google; even Walmart and Nike can now dominate the entire production chain through the ownership of brands, patents, copyrights, and logistical systems – all “soft” elements than physical end-products, all accumulated through financialization capitalism through a neo-imperialism monopoly-capital pathway.

Digital technology has already indeed transformed the world economy; the decade leading up to 2019, the largest 100 firms in the world had increased their total market capitalisation by US$12.7 trillion. A third of that increase (US$4.2 trillion) can be accounted for by just seven firms: Facebook, Amazon, Apple, Alphabet, Microsoft (the famous quintet ‘FAAAM’), Tencent and Alibaba. The aggressive rally of tech stocks during the COVID-19 pandemic had given due recognition that an entirely new model of value creation was enabled, and primarily all enhanced, by digital technology. Tech companies are the new empires of today: Alphabet revenue surpassed Hungary’s GDP, Facebook employs over 15000 content moderators around the world, and Microsoft has built data centers in nearly every corner of our planet, with Google global dominating the infrastructural platform corporate businesses.

Hidden from view, but the most vital part of this Techno-capitalism identity is the convergence of fibre-optics under the strategic blue waterways and sea corridors around the world that connected the various routers and artificial intelligence neural-networked database in a singularity ecosystem:

Since raw data, processed information and uninterrupted communications are of prime importance in a globalised geoeconomic environment, the installation, repairs and maintenance of the underwater cables in the country are with these infrastructural platform players of tech giants such as Google, Amazon and Microsoft, and the national internet exchange body, Malaysian Internet Exchange. However, the conflicting battle between national sovereignty and Global North financialised monopoly capitalism only accentuate the brute reality of intrusive Techno-capitalism and its digitalised colonisation process, (STORM 2023, marine-cabotage-under-netarchical-capitalism; whereas, the neo-imperialism aspects on 5-Eyes, Unmanned Underwater Vehicles, USVs, and the geopolitics involving AUKUS and QUAD are covered in firesstorms, August 2022).

II] TECHNO-CAPITALISM

With the emergence of new capital, the capital-endowed new ruling class extracts the content capacity of information to route around worker and social movements to barricade labour participation and involvement. The emerging ruling class is the digital feudal lords overseeing a common of digital infrastructure where bands of peasantry-labour are the digital gig-slaves to be exploited. In this digitalized business model, returns do not diminish as businesses scale up but increase exponentially. Geared towards the exploitation of digital-dehumanised workers (Yanis Varoufakis) whence they are mere interfacing intermediary conduits to big data storage and retrieval by infrastructural platforms powered by artificial intelligence nowadays that are so overwhelmingly powerful in exploiting surplus value of labour relentlessly, and with brutal efficiency, it is the accumulation of capital, through and thoroughly (Ursula Huws, Labor in the Global Digital Economy: The Cybertariat Comes of Age, 2014; read a case country of digital knights in a kingdom of infrastrutural thrones, in STORM 2020; Big Tech and Large Gig-Labour: STORM, June 2022 and Digital Labour: STORM, December 2020 ; and a related essay on Techno-feudalism, in STORM, August 2022).

It is also becoming but unbelieving for foreign investors – specifically Global North monopoly-capital corporates – not wanting to partner local expertise to provide support and services from their financialised capital. These Global North entities insist on retaining their monopoly investments, especially on the infrastructural platforms varied ecosystems.

As an instance, the country needs local expertise to ensure our national undersea cables are well maintained and not to be wholesomely dependent on Global North monopoly-capital corporations on an unequal economic and inaccessible technological exchanges. That the international infrastructural platforms had once threatened to withdraw in cooperating with the national digital economic aspiration is uncalled for.

At a time of an epidemiological-economic-ecological polycrisis, many national banks accelerated the monetary flow – and the resulting wave of liquidity – leading to substantial increases in corporate wealth in many developed and advanced economies, whereas the emerging and low income economies face external debt distress compounding poverty of the global poors, (World Bank 2022; STORM, 2022, Wealthy Rich, Poverty Poors). As a result of falling income levels, widespread employment losses and widening fiscal deficits, (UNCTAD 2020) – a rakyat-oriented governance should not allow appearance of vulture-capitalism in the guise of infrastructural platforms be roaming the waves of high blue waterways as predatory pirates, (STORM, January 2023) when there is a sea of opportunities for the country in laying submarine cables, too:

And even as the Covid-19 pandemic coursed through the world’s population, Apple, Microsoft, Alphabet, and Meta Platforms – were able to rake in US$255.7 billion in profits in 2022, or 16.4% of the Fortune 500’s total earnings for the year, (Fortune, June 2023). Their capital accumulation revealed grotesque class and racial inequalities and the gross lack of public investment and preparation, (monthlyreview).

To compound developmental efforts, transnational corporations (TNCs) exploit legal loopholes in low-income countries (LICs) to avoid or minimize tax liabilities by applying a practice known as ‘base erosion and profit shifting’ (BEPS). Under such circumstances, tax havens collectively cost governments US$500–600B yearly in lost revenue. Low-income countries will lose some US$200B – more than even the foreign aids of US$150B that they received annually, (Jomo, June 2022). Indeed, TNCs-supported agents, and lobbies, have blocked the International Tax Cooperation initiative, (Anis Chowdhury and Jomo Sundaram, June 2021) to ensure tax equity and revenue intake equality, (see also STORM 2023, International Corporate Taxes – issues of misdeeds).

And whatever financial assistance as rendered, the World Bank category of aid only encourages governments to enable illicit financial outflows to offshore tax havens – where such tax havens could cost countries US$4.7 trillion over the next decade, (icij 2024) – reducing capital controls, thus draining further precious foreign exchange and government resources, (KS Jomo, 2024).

III] DIGITALISED LABOUR

Nested in the platform capitalism model is the software component and the associated IT infrastructural platforms’ solutions. Unlike in the manufacturing sector where labour is kept within borders while capital moves freely, in Big Tech there is this process ability to intrude into a target country to install infrastructural platforms as well as troll the planet for cheap labour in any part of mother Earth at any time.

The resultant, and a transformed economy, is the gig economy, also widely defined as “platform economy”, “on-demand economy” or “sharing economy”, synchronises to the demand and supply of short-term or task-based work activities, and as a part of the national economy where freelancing workers use digital platforms to participate in the national economy, including their connections with the traditional yet formal businesses. According to Emir Research, about four million people in the Malaysian workforce which is about 26% of the labour force work in the gig economy; this is almost double the global average.

This business model is what technology guruAzeem Azhar names as the ‘AI lock in loop’ where, as the tech companies deploy products and services, they also collect data about their consumers’ use of those products and services. Through machine-learning processes performed on those collated data, these business entities envisage in presenting opportunities towards the development of better products and services. It is by integration of multiple data-rich digital assets into a single platform that gives such tech companies access to the entire vertical product chains (examples like Google or Grab siphoning off personal biodata and geographical locations) and the supply-chain capacity to expand horizontally into new products and services with relative ease and effectiveness. For examples: Google, Facebook, WeChat or Grab becoming cloud-servers, WhatsApp as a communications medium and Instagram an media aggregator, (Social Europe, Gig Workers Guinea Pigs of the New World of Work, February, 2021 where ‘bogus’ self-employment workers are left outside of the regulatory framework; Foundation for European Progressive Studies, Governing Online Gatekeepers: Taking Power Seriously, 2021; see also ILO 2021 report on the states of precarious digital labour.

In case country Malaysia, the adoption of digitalisation only deepen the stronghold of the monopoly-capitalised infrastructural platforms that support artificial intelligence domain, in the digital frontier and defranchised digitilased zero-hour gig-labour, (STORM 2023). This informal employment sector not only occupies a sizeable segment of the country’s workforce but inevitably it is without adequate social security safety provisions in place, (read csloh, 2022: Workers; Emir Research: Brain Drain; bernama: gig-economy and Khazanah Research Institute 2020, Shrinking “Salariat” and Growing “Precariat”?):

For AI to bind adhesively within a national economic development initiative, not only must the monopoly-capital-compradore-capital eIements be done away, but the labour exploitation factor be eliminated, too. Labour superexploitation conceptually captures the real condition of the working class in Africa, Asia and south America. It involves three elements: low wages, long hours, and intense work leading to due strenuous exhaustion. Above all, it is characterised by “the greater exploitation of the worker’s physical strength, as opposed to the exploitation resulting from increasing his productivity, and tends normally to be expressed in the fact that labor power is remunerated below its real value.” Ruy Mauro Marini.

An AI class analysis can be by way of applying Nicos Poulantzas concept of class [places] as existing at each of levels of society: economic, political, and technological. The class [positions] of the capitalist fundamental class processes are productive endusers (performers of data entry) and productive capitalists (extractors of processed data in the form of information).

The class relationship where dominating [power] ensues would be identified, therefore, through the stronghold of infrastructural platform [place] which has allied with financialised capital providers [positions] in the provision, control and ownership of software, hardware and process [power].

Capitalists appropriate surplusvalue from the consumption of enduser’s labour activities during the generation of data into processed information. The surplus (monetary and or metadata of say geographical locations in an e-hailing process) is distributed as extracted among beneficiaries of subsumed class positions like the state-enabler, IT vendors, financiers and compradore monopolies.

In essence, historical politico-economic development of a country comes from social practice, the struggle for production, the class struggle, and scientific work.

For the SCRIPT in Madani Malaysia to be successful, in term of implementation and sustainability of an AI-driven progressive politico-economic developmental praxis, working-class unity has to be consolidated. It can only be further solidified if the tenet of divisive divisions by capitalism is better understood both in theory and in practice. Hence, we argue for a comprehensive yet bold project that is based on TAPAO that goes beyond its ethos as a renewal of an socialist ideal with Malaysian characteristics in order to take full account of the struggle of the labour movement.

EPILOGUE

What are the remedies to limit infrastructural platform capitalism dominance, the AI perversion and the digitalised colonisation process?

A global tax on capital or the implementation of the Wealth Tax at the national level, is one way to allow for the creation of a “social state” meeting social needs, (Piketty, Capital in the Twenty-First Century).

Taggling digital labour by putting the most essential needs of people and the environment before profits where provision “jobs…for the unemployed, food for the hungry, houses for homeless, adequate health care and income security and a decent environment for all of us” whereby the highest priority is an implementation of these collective human goals to which all special interests would then be subordinated. (Magdoff and Sweezy, Stagnation and the Financial Explosion, 88–90).

In a previous essay, (The New Debt Crisis), we were relating some of the emerging problems of the Global South’s national debts with this introductory exploration:

For more than once, people are waking up to discover that another international debt crisis of enormous proportions looms on the horizon of a scale not seen since the early 1980s, after which Latin America and Africa have had to slog through a “lost decade.” Also, it’s a time when major economists have put forward theories predicting a falling tendency of the rate of profit under capitalism. There is no reason at all why the rate of profit in the economy should fall because of accumulation of capital, (Prabhat Patnaik, 23/07/2023).

Indeed, a paper in the New Political Economy published online in 30 Mar 2021 by Jason Hickel, Dylan Sullivan and Huzaifa Zoomkawala have contended that wealth drain from the Global South remains a significant feature of the world economy in the post-colonial era; rich countries continue to rely on imperial forms of appropriation to sustain their high levels of income and consumption. The researcher-authors further articulated that the Global North appropriated from the Global South commodities worth US$2.2 trillion in Northern prices that were enough to end extreme poverty 15 times over. Over the 1960–2018 period studied, the value drain from the Global South totalled USD$62 trillion (constant 2011 dollars), or USD$152 trillion when accounting for the Global South countries’ lost growth alone, (see STORM 2021, Unequal exchange under neo-imperialism; Jason Hickel and Dylan Sullivan, Capitalism, Global Poverty and the case for Democratic Socialism).

We take up excerpts of Vijay Prashad‘s discussion from here.

2] THE MOROCCO CONFERENCE

Ahead of the meeting in Morocco, Oxfam issued a statement that strongly criticised the IMF and World Bank for ‘returning to Africa for the first time in decades with the same old failed message: cut your spending, sack public service workers, and pay your debts despite the huge human costs’. Oxfam highlighted the economic crisis facing the Global South, pointing out that ‘more than half (57 percent) of the world’s poorest countries, home to 2.4 billion people, are having to cut public spending by a combined $229 billion over the next five years’. On top of this, they showed that ‘low- and low-middle income countries will be forced to pay nearly half a billion dollars every day in interest and debt repayments between now and 2029’. Though the IMF has said that it plans to create ‘social spending floors’ to prevent cuts in government spending on public services, Oxfam’s analysis of 27 IMF loan programmes found that ‘these floors are a smokescreen for more austerity: for every $1 the IMF encouraged governments to spend on public services, it has told them to cut six times more than that through austerity measures’. The fallacy of ‘social spending floors’ has also been demonstrated by Human Rights Watch in its recent report, Bandage on a Bullet Wound: IMF Social Spending Floors and the COVID-19 Pandemic.

In July, the IMF approved a $3 billion stand-by agreement with Pakistan that it claimed would create ‘the space for social and development spending to help the people of Pakistan’. However, the IMF is simply feeding Pakistan the same tired neoliberal package, calling for ‘greater fiscal discipline, a market-determined exchange rate to absorb external pressures, and further progress on reforms related to the energy sector, climate resilience, and the business climate’—all measures that will exacerbate the crisis. To ensure the permanency of these policies, the IMF spoke not only with the government of Caretaker Prime Minister Anwaar-ul-Haq Kakar, but also with former Prime Minister Imran Khan (who was removed from office in 2022 in a move that was encouraged by the United States due to his neutrality on the war in Ukraine). As if this were not enough, through its role facilitating the agreement, the U.S. government pressured the Pakistani government to supply weapons to Ukraine in secret through the disreputable arms dealer Global Ordnance. This makes an already bad deal even worse.

Thus, protests arise

These protests—from Suriname to Sri Lanka—are the latest cycle in a long history of IMF riots, such as those that began in Lima (Peru) in 1976 and sprung up in Jamaica, Bolivia, Indonesia, and Venezuela in the years that followed. When the IMF riots unfolded Indonesia in 1985, long-time CEO of the Bank of America Tom Clausen was presiding over the World Bank (1981—1986). In remarks that he made five years prior, Clausen encapsulated the attitude of the Bretton Woods institutions towards such popular uprisings, stating that ‘When people are desperate, you have revolutions. It’s in our own evident self-interest to see that they are not forced into that. You must keep the patient alive, because otherwise you can’t effect the cure’.

III] THE CLAUSEN CURE

Clausen’s ‘cure’ —privatisation, commodification, and liberalisation — is no longer credible. Popular protests, such as those in Suriname, reflect the broad awareness of the failures of the neoliberal agenda. New agendas are needed that will build upon the following ideas, such as:

Cancelling odious debts, namely those taken by undemocratic governments and used against the well-being of the people.

Restructuring debt and forcing wealthy bondholders to share the burden of debts that cannot be fully repaid (without wreaking devastating and fatal social consequences) but from which they benefited for decades.

Investigating the failure of multinational corporations to pay their fair share of taxes to poorer nations and establishing laws that prevent forms of theft such as transfer mispricing.

Investigating the role of illicit tax havens in allowing elites in the poorer nations to ferret away the social wealth of their countries in these places and procedures to return that money for public usage.

Encouraging the poorer nations to take advantage of new lenders that are not committed to austerity-debt forms of lending, such as the Peoples Bank of China and the New Development Bank.

Developing industrial policies that are geared toward creating jobs, lessening the destruction of nature, and progressively adopting renewable energy sources.

Implementing progressive taxation (especially on profit) and a living wage in order to ensure fair income for workers as well as wealth distribution.

The IMF Report on Malaysia 2023 projects a slower economic growth this year owing to a high global inflation rate and the cross-border conflict between Russia and Ukraine. This institution expects the global economic growth to drop to 2.8 per cent this year, down from its earlier forecast of 2.9 per cent and in comparison to the growth in 2022 of 3.4 per cent. Consequently, a correlated decreasing growth in the country is expected.

2] ECONOMIC GROWTH DIMENSION

The central theme in a capital-driven economy is a system driven by endless economic growth impulse. This mode becomes the root of our multiple, interlinked, and the contributory and accelerating crises become embedded within the socioeconomic system. The consequence of this growth – especially with the Global North excessive material throughput – drives the ceaseless accumulation of capital where it builts upon a constellation of exploitation of labour and extraction of natural resources.

Capitalism – which surges from crisis to crisis – is leading us to ecological collapse, while creating inequality on its capital accumulation process through commodifying essential goods and services. It assumes the replication of neocolonial relations with the Global South, and committed neoimperialism in this endeavour.

One distinguished aspect clearly distinctive is that with globalisation, rentier capitalism compradores begin attaching to neo-imperial monopoly capitalism and their linkages to the global commodity chain dimension because of the multiple roles of rent intermediaries between capital and its accumulation. The consequence is that these capitalists are accentuating wealth disparity with the working class.

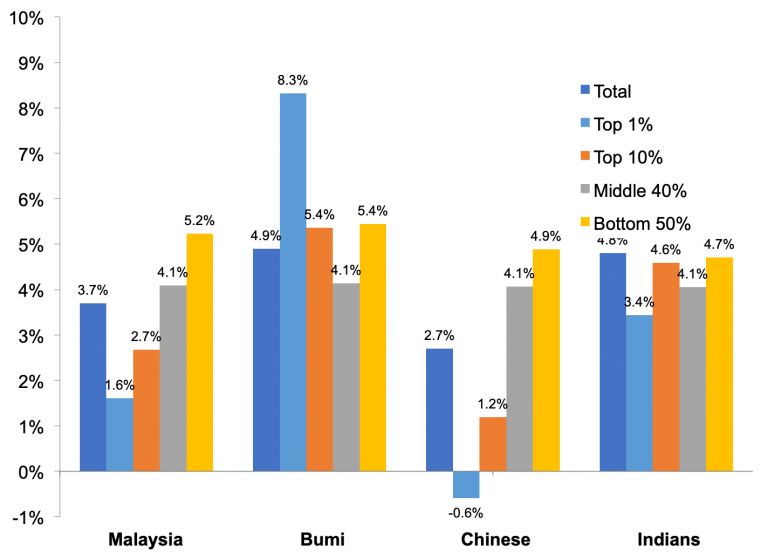

The absolute gap across income groups has increased with the top 20% of population – the T20 – possess 46.2% of the national income share, while M40 have 37.4% but the bottom 40% of population – the B40 – only 16% share of national income.

Compounded with

i) Compared to many other countries that have graduated from middle-income status, Malaysia has a lower share of employment at high skill levels and higher levels of inequality.

The foreign cheap labour is the biggest policy issue in Malaysia because if they are cheap, our young people cannot get their wages up.

ii) There is a growing sense that despite economic growth, the aspirations of Malaysia’s middle-class are not being met and that the economy did not produced enough well-paying and sufficient high-quality jobs. There is a widespread sense that the proceeds of growth have not been equitably shared and that increases in the cost-of-living are outstripping incomes, especially in urban areas, where three-fourths of Malaysians reside. The UNICEF 2020 Report has shown that low income female-headed households are exceptionally vulnerable.

iii) The country shall, increasingly, need to depend upon more knowledge-intensive and productivity-driven growth, closer to the technological frontier and with a greater emphasis on achieving inclusive and sustainable development, yet this generation is not forthcoming.

iv) According to the World Bank’s Human Capital Index, Malaysia ranks 55th out of 157 countries. To fully realize its human potential and fulfil the country’s aspiration of achieving the high-income and developed country status, Malaysia will need to advance further in education, health and nutrition, and social protection outcomes.

v) Key priority areas include enhancing the quality of schooling to improve learning outcomes, rethinking nutritional interventions to reduce childhood stunting, and providing adequate social welfare protection for household investments in human capital formation.

Companies need to organise their training and reskilling programme as part of their business strategy. This is also truism for the civil service, (seeSTORM 2023, Place, Position, Power of Public Sector) because the economic dimensions are changing very rapidly. On one prominent aspect is that lower economic growth translates into lower ROE for FDI which is the Malaysia’s structural weakness of relying on debt-driven domestic consumption to fuel economic growth. Basically, Malaysia’s growth strategy of the last 25 years since the Asian Financial Crisis was a debt-driven domestic consumption story. This is the dominant structural issue that Malaysia now faces conspicuously, and has not only to destruct its legacy and lack lustre entities but to construct a new economic development mode, (seeSTORM April 2023, Structuring lnstitutional Reforms for Economic Development {SIRED}; TAPAO; and Madani Malaysia praxis).

It had once expressed if development in Malaysia is to be self-directed and comprehensively inclusiveness, then traits of such a “developed society should also embrace secularisation, industrialisation, commercialisation, increased social mobility, increased material standard of living and increased education and literacy besides such things as the high consumption of inanimate energy, the smaller agricultural population compared to the industrial, and the widespread social network” (Syed Hussein Alatas, “Erring Modernization: The Dilemma of Developing Societies”, paper presented at the Symposium on the Developmental Aims 1996, pp 70-71).

Therefore, the key challenge for the next two decades, at least, would be to improve the indigenous innovative capacity of domestic firms and to continue to raise the productivity of Malaysian workers and firms whereas succeeding ruling regimes had given preference towards corporate capital than socioeconomic determinants of rakyat2 labour well-being, (seeSTORM, May 2023, MADANI the SCRIPT : labour exploitation and capital accumulation factors).

3] CRITIQUE OF THE IMF REPORT

On the inflation spectre, though it is projected to remain elevated at about 3.25%, there is a likelihood of a persistence in core inflation. Then, there is also an emerging evidence of a build-up of demand-side pressures, adding to higher prices, (see various MIDF Research reports).

Further, with record spending on subsidies, though seen from within the country that the inflation had not surge in tandem with global food and commodity prices, but nevertheless, there was still on the upward trend for most of 2022, reaching 3.3% for the year that may migrate to the later part of year.

Therefore, monetary policy would require further tightening to keep inflation contained and rakyat² expectations well anchored.

Secondly, whether the gradual fiscal consolidation strategy, as set out in the 2023 Budget, can be set to rebuild buffers has yet to he discerned. The national debt is yet to be on a downward path but instead has been tracking upwards. The ability to reduce overall fiscal risks – high budgetary expenditure on top of repayments to 1MDB debt interests, and the efficiency to collect due corporate taxes – is still an unknown uncertainty. Debt repayment is the second highest operational expenditure in the 2023 Budget, where 18.5 percent is designated to repaying public debt.

This owes to the fact the previous governance had not performed due compliance, expecially durable revenue collection measures of high quality and enforced with prudence.

Preceeding regimes had constant, and continuous, budget deficits (meaning it spends more than it brings in through taxes and other revenue), and had inadvertently borrowed huge sums of money to pay its bills.

If these measures are not applied bluntly, then likely there is not much of created space for critical investment needs and, most importantly, for targeted transfers to low-income households. Further, if these revenue-collection tasks are well coordinated, and managed administratively well, this would help market confidence in the country’s strong fundamentals.

Thirdly, the unity government’s commitment to fiscal reforms is highly appreciated by capital and endorsed by labour. As such tabling of the Fiscal Responsibility Act is most welcomed. Further, the planned subsidy reform, and plans to develop a medium-term revenue strategy, would positively tighten the economy, and may bring the currently accommodative stance to neutral. What this means is that the approaches would well be kept inflation contained, and thereby, rakyat² expectations anchored.

MIDF Research has indicated that Malaysia’s growth of gross domestic (GDP) is set to increase 4.5 per cent for this year and 2024. In a sense, the structural reforms initiated by the unity government is on the correct Madani Malaysia pathway to an economic growth, (seeSIRED, 19/04/2023).

However, though the economy is growing but with unbalanced development where geographically some states in semanjung and in the Borneo states of Sabah and Sarawak are still stumped by retarded development.

As an instance, ten years ago, the median household income in Kuala Lumpur was 2.6 times higher than in Kelantan; latest data indicates that this ratio has crept higher to 3 times higher.

In 2016, nearly one in three households living in Kelantan do not have access to piped water in the home, while one in nine households in both Kelantan and Sabah live in houses classified as ‘dilapidated’. In parts of Sabah and Sarawak where connectivity is poor, geographic disparities in access to basic services are more alarming: one in five households in East Malaysia live further than 9-km from the nearest public healthcare facility and secondary school.

Therefore, neoliberalism entity like the IMF’s Executive Board may praise country’s performance to elicit continuing consultation services and financial dispensing from western imperialism .

It is another budge in opening door to Global North domination and exploitation on national economic development – and indebting nations – than an equal exchanges for mutual shared prosperity among common wealth of nations.

This situation is the hallmark of neoliberal economic policies undertaken by country since gaining independence falling into the trap of development of underdevelopment,(read Ruy Mauro Marini, The Dialectics of Dependency).

4] IMF IMPERIAL INITIATIVE

IMF, and its sister entity the World Bank, is well-known for removing foreign exchange restrictions which retard the growth of global trade, with consequential international businesses being adversely affected.

Then, we have IMF’s High interest rates charged on its advances are considered one of the major disadvantages of IMF. So, the debt servicing for the less developed countries is difficult. For example, since 1982 the interest charged for loans out of the ordinary resources of the fund is 6.6 per cent. The interest rates payable on the loans made out of borrowed funds is as high as 14.56 per cent. So, developing countries experience a lot of difficulties in redeeming their loans borrowed from the IMF.

The IMF also often insisted upon that the borrowing countries have to reduce public expenditure in order to tide over their balance-of-payments (BOP) deficits. After 1970, the IMF imposed even stiffer conditional clauses. Among them are periodic assessment of the performance of the borrowing countries with adjustment programmes, increases in productivity, improvement in resource allocation, reduction in trade barrier, strengthening of the collaboration of the borrowing country with the World Bank, etc.

Then, further conditional clauses imposed by the IMF after 1995 are still stiff; just to state a few:

liberalizing trade by removing exchange and import controls;

eliminating all subsidies so that the exporters are not in an advantageous position in relation to other trading countries; and

treating foreign lenders on an equal footing with domestic lenders. The fund maintains a close watch on the activities of the borrowing country related to monetary, fiscal, trade and tariff programmes. IMF’s intervention in the domestic economic matters of the borrowing countries places them in a difficult position.

As an example, of concern is that Malaysia was reported with US$57,566,000,000 of international debts in 2021, according to the World Bank collection of development indicators on International Debt Securities: translated as two hundred fifty-three billion two hundred ninety million four hundred thousand Malaysian Rinngit Debt or RM$7,449 per rakyat owing.

The domination by rich countries is the major weakness of IMF. Though the majority of the members of the IMF are from the less developed countries of Asia, Africa and South Africa, the IMF is dominated by the rich countries like USA and western European nations . It is said that the policies and operations of the IMF are in favour of rich countries so much so that the IMF shall be regarded as “rich countries’ club”. These rich countries are always partial towards the issues faced by poor countries.

As reported in The Hindu (May 2, 2007), Venezuela’s president Hugo Chavez announced his country’s decision to leave IMF and the World Bank. He accused them of exploiting small countries. He branded the IMF and the Wold Bank as “mechanisms of American imperialism“.

Moreover, the OPEC nation’s leader Mr. Chavez said: “we are going to withdraw…. and let them pay back what they took from us”. He then issued an order to his Finance Minister to begin proceedings to withdraw Venezuela from both IMF and World Bank.

5] CONCLUSION

IMF ‘double standard’ displays capitalism’s inherent inhumanity where human lives in the periphery are worth less than human lives in the metropolis.

The IMF’s behavior is thus reflective of the very nature of capitalism, of its essential inhumanity. It does not only mean “inhumanity” merely in the sense that it places profits before people, but also in the sense which follows from it, namely that it does not see all human life as of equal value – that it is surely, and necessarily, applies “double standards” in every sphere of life, (Prabhat Patnaik, 15/05/2023).

According to a World BankReport, extremepoverty has increased. Concurrently, extreme wealth has also dramatically risen since the Covid-19 pandemic began.

The report shows that while the richest 1 percent captured 54 percent of new global wealth over the past decade, this has accelerated to 63 percent in the past two years. US$42 Trillion of new wealth was created between December 2019 and December 2021. US$26 Trillion (63 percent) was captured by the richest 1 percent, while US$16 Trillion (37 percent) went to the bottom 99 percent. According to Credit Suisse, individuals with more than US$1 million in wealth sit in the top 1 percent bracket.

Further, in the Oxfam publication: “Survival of the Richest” indicates that the richest 1 percent grabbed nearly two-thirds of all new wealth worth US$42 Trillion created since 2020, almost twice as much money as the bottom 99 percent of the world’s population.

For the past decade, the richest 1 percent had captured around half of all new wealth. Indeed, billionaires have gained extraordinary increases in their wealth.

Since 2020, during the pandemic and cost-of-living crises, US$26 Trillion (63 percent) of all new wealth was captured by the richest 1 percent, while US$16 trillion (37 percent) went to the rest of the world put together. A billionaire gained roughly US$1.7 million for every US$1 of new global wealth earned by a person in the bottom 90 percent. Billionaire fortunes have increased by US$2.7 billion a day. This comes on top of a decade of historic gains where the number and wealth of billionaires doubling over the last ten years.

2 HOW ARE THE IMMENSE WEALTH ACCUMULATED?

The wide wealth disparity between the ultra-rich and the poverty poors emerges from the coarse profits from the food and energy sectors. Billionaire wealth surged in 2022 with rapidly rising food and energy profits. The report shows that 95 food and energy corporations have more than doubled their profits in 2022. They made US$306 billion in windfall profits, and paid out US$257 billion (84 percent) of that to rich shareholders. The Walton dynasty, which owns half of Walmart, has received US$8.5 billion over the last year. Indian billionaire Gautam Adani, owner of major energy corporations, has seen this wealth soar by US$42 billion (46 percent) in 2022 alone.

It is stated in Oxfam 2023, “Survival of the Richest: the Indian Story” that 5 per cent of Indians own more than 60 per cent of the country’s wealth while the bottom 50 per cent of India’s population possess only three per cent of the wealth. From 2012 to 2021, 40 per cent of the wealth created in India has gone to just one per cent of the population and only a mere 3 per cent of the wealth has gone to the bottom 50 per cent. The combined wealth of India’s 100 richest has touched US$660 billion.

In Spain, the CCOO (one of the country’s largest trade unions) found that corporate profits are responsible for 83.4 percent of price increases during the first quarter of 2022.

Further, in the U.S., the UK and Australia, studies have found that 54 percent, 59 percent and 60 percent of inflation, respectively, was driven by increased corporate profits.

3 WHERE DOES THE INEQUALITY ARISES?

This spectre of inequality, and the immense wide-spread in hunger, occur increasing under an inflationary trend. At a time when at least 1.7 billion workers are living in countries where inflation is outpacing wages, and over 820 million people – that is, one in ten people on Earth – are presently going hungry everyday. Women and girls often eat least and last, and make up nearly 60 percent of the world’s hungry population. As indicated in various reports, the World Bank says we are witnessing the biggest increase in global inequality and poverty since World War 2.

Entire countries are facing bankruptcy, with the poorest countries now spending four times more repaying debts to rich creditors than on healthcare. Three-quarters of the world’s governments are planning austerity-driven public sector spending cuts – including on healthcare and education – by US$7.8 Trillion over the next five years.

In the New Political Economy, 30 Mar 2021 article by the Jason Hickel, Dylan Sullivan and Huzaifa Zoomkawala research team presents that wealth drain from the Global South remains a substantial feature in post-colonial global economy; rich countries continue to indulge in imperial forms of appropriation to sustain their high levels of income and spending.

For instance, prominent transnationals have had an important presence in the Brazilian agrifood industry since its birth; players include: Nestlé, Unilever, Anderson Clayton, Corn Products Company, Dreyfus, and the Argentine transnational Bunge y Borne (now simply Bunge). They were later followed, as different markets matured, by Kraft, Nabisco, General Foods, and Cargill from the United States, and United Biscuits, Bongrain, Danone, Parmalat, and Carrefour from Europe. The immediate consequences are that uneven and often uncoordinated foray of metropolitan corporate capital is subjugating the agriculture and domestic food markets of many developing countries, particularly smaller, peripheral ones undergoing rapid urbanization, to the needs of global agribusiness monopoly-capital; read Ukraine’s Big Farms’ global agribusiness land grab.

Then during the 1990s’, unrestricted movement of international finance capital, public sector enterprises or government-link companies (GLCs) increasingly are subjected under the hound of financialization capitalism. The metropolitan capital-as-finance (Patnaik 1999), gets control over Third World resources and enterprises to see the rise to international finance capital in league with the local neocomprador class becoming crony capitalism through the force of accumulation as articulated by Samir Amin (2019) in The New Imperialist Structure, Monthly Review, July 01, 2019. Anchored upon a capital-market system, this leads to the emergence to, and the pervasion of, financialization capitalism in Malaysia.

With globalisation, rentier capitalism compradores attaching to neo-imperial monopoly capitalism and their linkages to the global commodity chain dimension, the consequence is that these capitalists are accentuating wealth disparity with the working class; seeKhalid 2019 study where the absolute gap across income groups has increased, contributing to big chunk of the poverty poors being left behind. The top 20% of population – the T20 – possess 46.2% of the national income share, while M40 have 37.4% of the national income share.

5 WHAT TO DO?

According to various analyses by the Fight Inequality Alliance, Institute for Policy Studies, Oxfam andthe Patriotic Millionaires, an annual wealth tax of up to 5 percent on the world’s multi-millionaires and billionaires could raise US$1.7 trillion a year, enough to lift 2 billion people out of poverty, fully fund the shortfalls on existing humanitarian appeals, deliver a 10-year plan to end hunger, support poorer countries being ravaged by climate impacts, and deliver universal healthcare and social protection for everyone living in low- and lower middle-income countries.

Oxfam is calling on national governments to:

• Introduce one-off solidarity wealth taxes and windfall taxes to end crisis profiteering.

• Permanently increase taxes on the richest 1 percent, for example to at least 60 percent of their income from labor and capital, with higher rates for multi-millionaires and billionaires. Governments must especially raise taxes on capital gains, which are subject to lower tax rates than other forms of income.

• Tax the wealth of the richest 1 percent at rates high enough to significantly reduce the numbers and wealth of the richest people, and redistribute these resources.

This includes implementing inheritance, property and land taxes, as well as net wealth taxes. There are 80 percent of Indians, 85 percent of Brazilians and 69 percent of citizens polled across 34 countries in Africa are supporting increasing taxes on the rich.

Our leading economists are calling:

“This is precisely the time when you must reform taxes as you have it (windfall tax) all the time amid extraordinarily high petroleum prices or palm oil prices,” according to Khazanah Research Institute senior advisor Professor Dr Jomo Kwame Sundaram.

Institute of Malaysian and International Studies research fellow Dr Muhammed Abdul Khalid pointed out that policymakers tend to ignore the imposition of capital gains tax when it comes to the issue of tax reform. “Taxes must be fair ….. and we never talk about the urgency of imposing capital gains tax, maybe because it is going to affect the very well-off in Malaysia,” he said.

Indeed, there should be greater effort across tax instruments: to increase the progressivity of personal income tax, re-examine the number and targeting of corporate income tax incentives and to consider new sources of revenue such as environmental taxation and capital gains taxation. The introduction of capital gains tax, raising the tax rate for those in the top individual tax bracket and imposing a tax on retirement savings above a certain threshold were among the suggestions on how to enhance revenue in the World Bank Report, 2021, Malaysia Economic MonitorJune 2021: Weathering the Surge.

Recently there are a number of content materials debunking the debt trap diplomacy myths in Sri Lanka and Africa. What is often not stated is the insidious role played by other private capital actors, too.

There are in a number of developing economies today when debt restructuring cannot inevitably occur without the full participation of foreign private creditors.

2. THE BOND-HOLDERS

Indeed, the low- and middle-income economies owed, at the end of 2021, an estimated US$9.3 trillion to foreign creditors, mostly to private creditors and trans-bordering bondholders hovering globally across multiple countries. Since majority of the outstanding payable is private debt, more often than not, bondholders would consciously purchase the right to collect in secondary markets, too, at times very much like vultures in a kill-feed.

Among this flock of bondholders, a small minority are regarded as vulture investors. They tend to focus on the distressed debt of governments, buying their bonds at a deep discount with the ultimate goal of suing a ruling government to collect the full payment.

These investors have little incentive to participate in debt-relief initiatives. To maximize their return, they hold out until other creditors make concessions – in the expectation that concessions from others will free up cash that enables the holdouts to collect the biggest possible payoff.

This is an unadulterated form of free-riding that hurts all other creditors, too.

3. THE GOVERNING BODIES

Governments have an invoking public interest to end this imbalance on such unfair transactions. It is timely, and a long-overdue process, for national governance stepping up to protect rakyat2 from third party monopoly-capital financial capitalism exploitation which directly is an expropriation of national wealth in Global South countries.

Granting distressed governments even a few of the legal protections routinely granted to distressed businesses would fix much of the problem. However, enacting them in just a few jurisdictions – like in Global North New York and London, for example – would only perpetuate the sovereign-debt contracts of developing economies as governed by the laws of these monopoly-capital financial centres.

The Common Framework – the debt restructuring program endorsed by the G-20 for 73 of the world’s poorest countries – might be one good approach to try out their alternative techniques.

Under the terms determined by the Paris Club, non-ODA (Overseas Development Aids) claims can be written off in whole or in part, while ODA claims are restructured.

However, ODA poses more problems than it solves.

First, the amount. Since 1970, developed advanced country (DAC) members had committed themselves to devote a minimum of 0.7% of their gross national income (GNI) to ODA. However, this threshold has never ever been reached. In 2019, total ODA was estimated at $155 billion, that is, only 0.3% of DAC GNI. This amount pales in comparison with the $485 billion remitted by the diasporas to developed countries during the same period.

Second, its composition. Contrary to what its title would suggest, ODA is not unconditional, disinterested and “humanistarian” aid. It is composed of grants but also of so-called “concessional loans”. It is therefore not uncommon for the annual net transfer of ODA for a “recipient” country to be negative. Similarly, the country is not free to use these sums as it sees fit, but is subject to a programme defined by the donor countries and/or international institutions.

Finally, its opacity. According to the data provided by the OECD, it is not possible to separate aid in the form of grants from aid in the form of loans. In order to artificially inflate its figures, the OECD has created a “grant-equivalent” category that includes not only said grants, but also low-interest loans with a long repayment period in order to supposedly better “reflect the real effort made by donor countries”.

In fact, the application of large-scale statutory process such as the Sovereign Debt Restructuring Mechanism is most of the time regarded as being defeated by its own ambition. Indeed, those recommendations by the World Bank and the International Monetary Fund are no more than loan-sharking along2preying on unfortunate victims.

4. THE DEBTORS

2021: low- and middle-income economies owed an estimated $9.3 trillion to foreign creditors, mostly to private creditors and bondholders

Sub-Saharan Africa is the region of the World that is the hardest hit by the IMF and its austerity policies ¹imposed through structural adjustment plans since the 1980s, the HIPC initiative since 1996 and since April 2020 the Debt Service Suspension Initiative (DSSI). Among the worst hit countries are Côte d’Ivoire, Madagascar, Niger, Senegal, Congo (Democratic Republic) Togo and numerous Central African countries.

In a significant number of developing economies today, debt restructuring cannot occur without the full participation of foreign private creditors. Most of the private debt, moreover, is owed to bondholders who often, explored above, purchase the right to collect in secondary markets.

About 40 low-income economies and six middle-income economies are either in debt distress or at high risk of it. For both types of economies, there is only one pathway towards restructuring unsustainable debt. This is either through the Paris Club for middle-income economies and the G-20’s Common Framework for Debt Treatments for low-income economies

However, both approaches have certain process hurdles. Typically, In return for debt relief from foreign government creditors, borrowing countries would have to wrangle equivalent concessions from foreign private creditors – the vulture capitalists – over whom they have no bargaining power.