By financialization capitalism we shall mean an emerging form of capitalism that increasingly uses finance, and apply financial tools and means, in the operations of capitalism (John Bellamy Foster, The Financialization of Accumulation, Monthly Review vol:62, issue 05 October 2010), or simply as the financialization of the accumulation of capital process (Paul Sweezy, “More (or Less) on Globalization,” Monthly Review 49, no: 4 (September 1997).

The defining process of accumulation in financial capital would involve the investment of money or any financial asset to increase the initial monetary value of said asset as a financial return whether in the form of profit, rent, interest, royalties or capital gains.

This shift in economic activity from production, and in the service sector, to financial activities that generate high private rewards disproportionate to their social productivity (James Tobin, Nobel Prize in Economics 1981) is one central aspect whereby the surplus value, that is, the added value created by workers in excess of their own labour-cost is being appropriated by the new financial capitalists as profits, (Marx, The Capital, chapter 8). This surplus value as the source of society’s accumulation of fund or investment of fund, part of is re-invested, but part of it appropriated as personal income, and used for consumption purposes by the owners of capital assets. The workers cannot capture this benefit directly because they have no claim to the means of financial creation or its final production.

2] MONOPOLY-FINANCE CAPITALISATION

The creation of monopoly-finance capitals in the neoliberalism economy of Malaysia is no more than the hegemonic economic ideology of the Thatcher and Reagan regimes reflecting the new imperatives of capital – advancing IT-geared financial globalization planted in Malaysia as the engine of financialization capitalism model (Lena Rethel, Malaysian Capitalism, Rents, and Financialisation, University of Southampton, 2010).

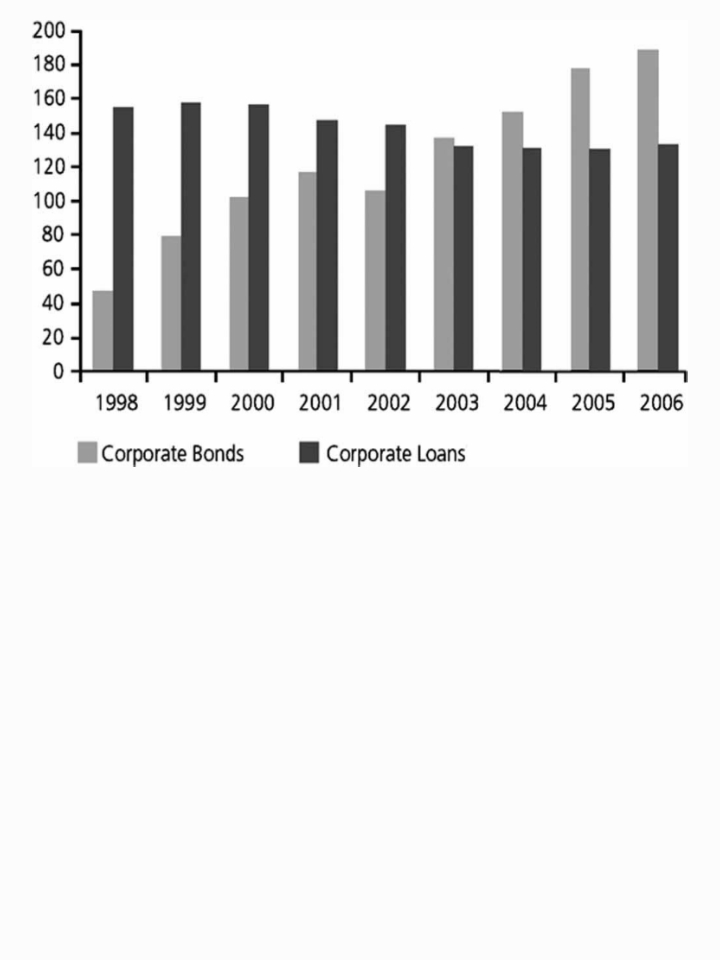

In the early 1990s, Malaysia corporations sought funds from the domestic equity market while non-financial enterprises relied on bank debt and the issuance of bonds abroad. Since 2003, however, the corporate bond market has reached an unprecedented size of RM$190 billion, while similarly since 1999 the total private sector bonds outstanding have surpassed that of public sector bonds (Bank Negara, 2007). This expansion of bond finance favours bigger corporations linked to the government – much to the disadvantage of the Chinese and Indian capitals’ SMEs that do not have the sizeable funding resources.

The ensuing financialization of Malaysian capitalism led to the emergence of a new politics of debts, and it also coincides with rising levels of household indebtedness. It reconfigures society where share ownership and shareholder value take preeminence, a growing influence from capital market-based financial system, the further entrenchment of the political renter class power as well as the polarization of wealth and income, and the explosion of financial innovation and trading that led an economy more towards “speculation” than the engenderment of production to be equally shared by rakyat (Costa Lapavitsas, “The financialization of capitalism”, SOAS abstract).

The above processes occurred when the existing relationship between the various forms of capital rent-seekers collude. Under the New Economic Policy (NEP) with state capitalism this process only accentuated with increased financialization, reinforcing the existing strand of an ethnically divided capitalism (Searle 1999, Riddle of Malaysian Capitalism, Asian Studies Association of Australia). The country’s economic initiative was to be in alliance with the private sector, especially while in collaboration with Chinese capitals during the early 1980s, was also evidently prominent in the collusion of the privatization of state assets at that period, (Heng Pek Koon, The New Economic Policy and the Chinese Community in Peninsular Malaysia, The Developing Economics, 1997).

Whereas the majority of businesses built during the prewar period were found in the tin and rubber industries that comprised illustrious family firms built by Low Yat, Loke Yew, Chong Yoke Choy, H.S, Lee, Tan Chay Yan and Lau Pak Khuan who colluded with imperial British plantation interests to build their empires, the “new money-capital” entities like YTL Corp’s Yeoh Tiong Lay, Berjaya’s Vincent Tan, Genting’s Lim Goh Tong, Sunway’s Jeffrey Cheah, Lion’s William Cheng and the Ananda Krishnan groups and business stables attempted the forging of more Sino-Indo-Malay corporations, that is, a co-opetition strategy whereby Chinese and Indian capitals can compete as well as co-operate with Malay interests, (see Neo Yee Pan “The Role of Chinese Business in the Context of Our National Objective” paper delivered at the MCA Economic Congress, March 3rd. 1974; Jesudason 1989, Ethnicity and the Economy: the State, Chinese Business, and Multinationals in Malaysia, Oxford University Press, Singapore; Heng, op.cit.).

Those Chinese capitals and Indian compradors would, by forming joint ventures with Malay capitals, tap upon the vast capital resources of State agencies such as PERNAS, PNB and Peremba Bhd, besides

UMNO-controlled corporations like the Fleet Group and Media Prima

Institutional funds such as Lembaga Urusan Tabung Haji (LUTH or Islamic Pilgrims Management and Funds Board) and Lembaga Tabung Angkatan Tentera (Armed Forces Funds Board)

Private sector capital held by new class of Malay millionaires such as Tun Daim Zainuddin, Tun Sri Azman Hashim, Tan Sri Wan Hamzah and Tun Sri Rashid Hussein as well as royal entrepreneurs like Tunku Imran ibni Tuanku Ja’afar of Negeri Sembilan

Then, the ordinary category of depositors are redefined as fee-paying consumers of financial products such as car and motor-cycle hire-purchase loans and credit cards payment to consumer products besides those remitting housing mortgages.

Thus, in 2005, the ratio of total household debt to GDP amounted to 72.6%, of which nearly 85% was provided by banks (Bank Negara Annual Report 2006), and that between 1999 and 2006, total Malaysian household debt grew at an annualized rate of 15%. From a base in 2000 over RM$160 billion in household debt, this amount had risen over a short period to nearly RM$400 billion by 2006.

Consequently, the national domestic and external debt, between 1991 and 2011 soared:

What is beginning to happen is that compared to the NEP period, between 1970-1980, the bank-based development state model was that the consumption needs of households had been subordinated to the financing needs of the industrial sector as well as the ethnic-based distributive policy, whereas post-economic downturn 1980s had seen private consumption (and thus household borrowing) is increasingly seen as the important driver of domestic growth. This also means that bank lending is much about sustaining consumption than that of production.

The fifth point is that the passing of the buck-ringgit, so to say, is the “individualization of risk” had meant a high incidence of household debts arising from marketed consumption patterns whereby April 2006 the Credit Counseling and Debt Management Agency (AKPK) has to be established as part of the government approach – to develop a personalised debt repayment plan in consultation with financial service providers – to confront the ever increasing consumer debt that was primary affecting many in the Malay (youthful) community. Unfortunately, AKPK had often portrayed these debtors as “innocent victims of circumstances” or as “hapless” or being “foolish” whereas the main underlying and real reason is that the rising household debt owes too much kleptocratic capitalistic instinct to empower capitalism, and more recently the financialisation of capitalism by ethnocapital rentiers.

As of March 2016, more than 148,000 borrowers have joined the debt management programme conducted by AKPK (Malaysian Reserve, May 25th. 2016).

Finally, public interest rates were driven to very low rate to enable such banks to make secure guaranteed profits by lending to their customers and households at higher rates. In short, the financialization of Malaysian capitalism had only encouraged public funds being injected into private and kleptocratic banks to boost capital and enlarge capital formation, and further where this public liquidity was to enable these banks to sustain their continuous siphoning operations.

Therein highlights the contradictions of poverty and inequality within society.

The second key point is that the rise of a ‘mass investment culture’ has strengthened the ‘dominance of finance capital’ (Harmes 2001, Mass investment culture?, New Left Review, 9, pp 103-24), and is a contributing trend in the financialization of capitalism in Malaysia today. Take as an example, PNB has also nowadays invests in bonds and structured instruments, thus assisting in the reproduction of a sustainable capital market-based financial system – a collateral vulnerabilities of increasing individual exposure to the capital market whereby inevitably “households had become financialized, too” (Costas Lapavitsas, Financialised Capitalism: Crisis and Financial Expropriation, Historical Materialism 17 (2009), School of Oriental and African Studies, London).

In effect, the evolution of unit trust investment, on one side though deviating from NEP redistributive schemes, has on the other hand, turns the capital markets as part of social policymaking, too. By October 2008, the ruling regime borrowed RM$5 billion to shore up the credit-crunch-affected equity market, with the money provided by EPF but disbursed by Khazanah jointly owned by EPF, PNB and Khazanah itself.

Thirdly, this shore up of government interests (not dissimilar to crony capitalism in the early stage of the NEP implementation during the 1970s) that only act as a political behaviour to protect the up-and-coming Malay middle class (Embong, State-led Modernisation and the New Middle Class in Malaysia) and the Barisan Nasional clientel, but also as a conduit on preserving the wellbeing of the capital market so as to be used to bail out Malaysian corporations and favoured individual capitalists.

As the state’s role was being transformed to meet the new imperatives of financialization, the kleptocratic governance had to assume as lender of last resort –bailing out crony capitalists like Malaysian Airline System’s Tajudin and Halim Saad’s United Engineers Malaysia (UEM) and the Renong Group (the largest bumiputera-owned conglomerate then) when in August 2001, Syarikat Danasaham – the wholly subsidiary of state-owned investment house Khazanah Nasional – made a conditional voluntary offer to purchase the entire shares and warrants of UEM, including Renong’s stake.

Lastly, PNB evolution from changing state investment practices to assume increasingly a role as ‘market players’ where the investment strategy has become more neoliberal following financial considerations on return-oriented basis, there is a competitive stance in maintaining, and retaining, share of the market than that of a distributive expression as articulated within the 1970s’ NEP objectives. It started as a state investment vehicle to strip off government assets for private Bumiputera interest. Using these ill-gotten funds, by 1981 PNB became one of the leading Bumiputera investment institutions acquiring RM$487 million shares in 60-odd companies.

3] ECONOMIC DEVELOPMENT REVISIONISM

With this expanded capital base, the 1980s economic development revisionism only contributed to the seedling of fund that eventually induced the introduction of financialization capitalism in the country. For example, PNB has together with Khazanah, implicated in the launch of the “transformation programme for government-linked companies”. For instance, Pemandu (Performance Management Delivery Unit) was set up under the Prime Minister Department on Sept 16, 2009 to oversee the implementation of the Economic Transformation Programme (ETP) and the Government Transformation Programme (GTP), the two key pillars of the government’s New Economic Model (NEM) introduced in 2010.

Secondly, the reforms heralded by Prime Minister Najib in 2009 and implemented by Idris Jala, Minister in the PM’s Department heading the Performance Management and Delivery Unit (Pemandu) have been lackluster, and not as successful in their implementation as often propogated (Research for Social Advancement (REFSA), A Critique of the ETP, Part I and Part II, January 2012). According to other analyses of the 12 national key economic areas that Pemandu targeted upon, they averaged lower gross national income growth than non-key sectors between 2011 and 2014 at 4.99 percent against a national average at 8.77 percent.

These state-funded vehicles, instead of overseeing the New Economic Model progress, have willingly driven public funds being routed into the banking system to boost capital. With the availability of ready liquidity of public fund, the consolidated domestic banks nowadays are able to more than sustain their profitable operations.

The third pointer is that public interest rates – by which the central bank in hoarding dollar reserves, Bank Negara is able to “sterilize the reserves” – are being driven down to enable the banking system to make secured profits by lending to their clienteles at higher rates.

4] GROWTH OF FINANCIALISATION OF WORLD ECONOMY lies in the deeper imperial penetration into underdeveloped economies with wider financial dependence, (see Magdoff 1978, Imperialism: From the Colonial Age to the Present and Magdoff, 1969, The Age of Imperialism; also refer to Foster “The New Imperialism of Globalized Monopoly-Finance Capital – An Introduction”, Monthly Review, Vol:67, Issue 03), like in Brazil where the domination of global monopoly-finance capital has attracted portfolio investment, and to pay off its external debts to international capital, including the IMF that accrued high interest rates, de-industrialization, a slow growth in its economy, and the continuance vulnerability to the often rapid movements of global finance (IMF, World Economic Outlook, 2015).

The daily average volume of foreign exchange transactions, even from old data set had indicated the magnitude the seriousness and depth of neo-imperial financialization penetration: US$570 billion (1989) had increased to US$2.7 trillion by 2006, and US$5.7 trillion in 2013 (Bank of International Settlements, various reports). Therefore, the agglomeration of wealth, and its continuous transferring across the globe, had pointed to the increasingly related to finance transactions than the physical material mode of production. It also indicative in some ways through transfer-pricing by trans-national corporations (TNCs) that there is a constant leaking of investment fund from Malaysia, and there is consultancy advisory on how to minimize it (see Juliana Tan Ming Qing, Malaysia: Transfer pricing aspects of restructuring, KPMG 2014; Bob Kee and Mei Seen Chang, Malaysia: Malaysia’s evolving transfer pricing landscape, KPMG 2014).

5] THE FINANCIAL SUPERSTRUCTURESTRANGLING HOMEOWNERS

The financial superstructure’s demand for new cash infusions to keep speculative financial derivatives expanding (seeFoster “The Financialization of Capitalism”, op.cit.), has meant that it encourages homeowners to maintain their lifestyles even with stagnant real wages that are causing the Malaysia’s household debts being the highest in Asia – as at August 2015, the country’s household debt-to-GDP ratio stood as high as 88.1% (The Edge 22/02/2016; by March 2016, the total household debt in Malaysia stood at 89% of the Gross Domestic Product or RM$1 trillion, consisting 80% from the banking system, with 20% from non-banking financial institutions, Malaysian Reserve, 26th. May 2016); whereas, collectively, the 9 richest men in Malaysia have a total capital asset of RM$175 billion (Forbes 2016).

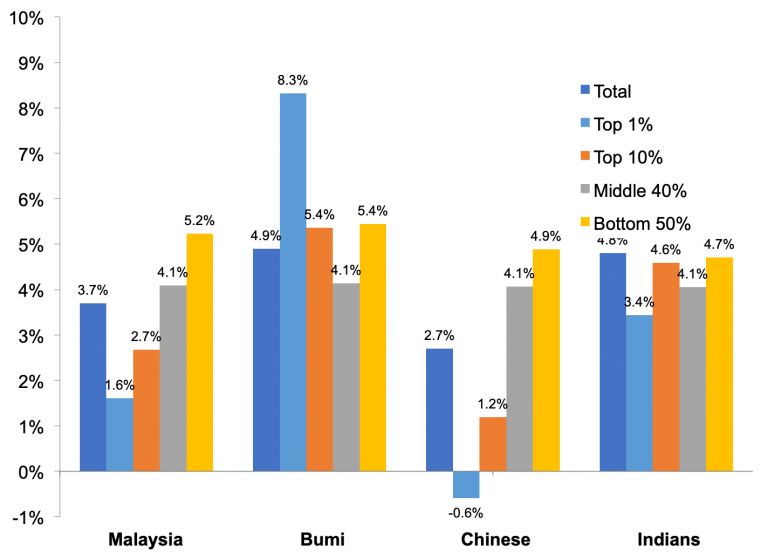

Existing data have also signified that the rapid increase in inequality have become built-in necessities of the monopoly-finance capital phase in the neo-imperialism system. The wealth gap among Malay Malaysians has grown larger significantly with the Gini Coefficient among the bumiputeras having the highest inequality (Hwok-Aun Lee and Muhammad Abdul Khalid, Is inequality in Malaysia really going down?, Faculty of Economics Administration Working paper 2014/09, University of Malaya).

This is duly noted by the Khalid research paper at the London School of Economics and Political Science, where presented, the disparity among the Malay community – the top 1% – is much acute, and accentuated as ever.

After six and half decades of sustained neoliberalism economic developmental effort, the nation of Malaysia is still as disparity in absolute income inequality as ever, (see lower right chart below)

Sources: World Bank datasets and DoSM statistics

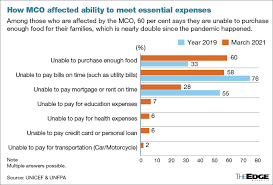

It is also an era of a generation when 70% of lower-income households cannot even meet monthly basic needs – indeed, more than 60% of these households reported having no savings at all – not much of a difference than 10 years ago:

According to the Employees Provident Fund, over two million contributors aged between 40 and 54 have less than RM10,000 in their retirement savings accounts; and

where increasingly these household expenditures are expansively spent on food:

Thus, the nation of Malaysia is still encasted in acutely absolute income inequality as ever:

As an instance, Bantuan Tunai Rahmah, the cash aid scheme, reportedly has 8.7 million recipients – a quarter of the population – which gives a damning statement on the extent of low incomes among our workers.

As global growth is likely to decelerate sharply to 1.7 percent in 2023 synchronous with policy tightening, worsening financial conditions, and continued disruptions from the Russia near-border conflict, the activity in Emerging Markets and Developing Economies (EMDE), excluding China, is forecasted to slow from 3.8 percent in 2022 to 2.7 percent in 2023 on account of weaker external demand and tighter financing conditions.

2] STATE OF NATION

With government revenue projected to remain low and structural expenditures still increasing high, this has led to further narrowing of Malaysia’s fiscal space (see right chart below):

Using the ratio of the Federal Government Debt to the revenue collection as a reference point, the World Bank has indicated that Malaysia’s fiscal space has gradually narrowed since 2012 and became tighter post-pandemic.

The government’s medium-term fiscal consolidation plan is guided by its Medium-Term Fiscal Framework (MTFF). Under the latest MTFF for 2023-2025, the government has adopted from the previous MTFF estimate, based on a projection that nominal GDP will expand by an average annual rate of 5.5 percent, and that the average price of crude oil will maintain at US$90 per barrel. As with the previous MTFF, the current framework pursues an expenditure-driven fiscal consolidation, (see chart above: left side).

The government expects operating expenditure to decline from 15 percent of GDP in 2023 to around 14.5 percent over the MTFF period.

The government also expects revenue to decline over this period, from 15 percent of GDP in 2023 to an average of 14.7 percent in 2023-2025. Overall, the fiscal deficit is expected to consolidate at a gradual pace with the overall balance averaging at 4.4 percent of GDP for the MTFF period.

The current fiscal consolidation strategy – via spending reduction – is, to many national economists and political analysts, rather challenging, given the current tight spending domain.

Firstly, the combined spending on structural expenditures is already at high levels; and secondly, other Operating Expenditures components such as supplies and services, and grants and transfers have been on a declining trend or are already at low levels.

Therefore, the government’s current fiscal consolidation plan would have to include a higher revenue collection target.

Through preceeding regimes’ gorging and siphoning – and depleting – of national wealth, whereupon revenue level has remained low and is still trailing comparative peers. It is more than ever importantly to address the persistent decline in revenue collection and explore new sources of revenue, more so under an inflationary trend that affect every poor people of the low-incoming developing countries.

3] SOURCES OF DEVELOPMENT REVENUE

A) Sovereigns can borrow from within their own country or from abroad.

Domestic borrowing – from local banks and asset managers or directly from households (EPF employees’ money or PNB owners’ saved trust units) could likely be a steady and reliable source of financing. However, there is a limited amount of money available and repayment maturities tend to be short. Not infrequently, governments also borrow from international capital markets, in larger amounts and usually at longer maturities.

Otherwise, there is a wide and diverse range of private sector entities willing to lend to sovereigns, too. Asset managers, such as pension funds, typically hold a large amount of government debt. They need relatively safe long-term assets to match their long-term liabilities.

B) In big ticket projects, they have been financed typically through government budgets, either from tax revenue or from government borrowings, some had often been financed through special-purpose vehicles (SPVs) — for example, DanaInfra, which was set up to raise financing for several infrastructure projects. The debts of these SPVs are guaranteed by the government, and hence, can be considered ultimately as government debt.

Many public infrastructure projects have also been privatised, and the private investors would recover their cost of investment through collecting tolls or charges from the users. Examples of these include the toll roads, independent power producers and land-swap projects. In such cases, the government does not carry any liability for these projects unless it has given some form of revenue guarantees to these private investors. This financing model (using private-sector finance and project development expertise) is known as a public private partnership (PPP).

Not often publicised is another variant of PPP, where private investors recover their cost of investment through payments from the government. This is generally known as a private finance initiative (PFI) which has its many odious transactions. PFI payment obligations comprise a large proportion of the PPP debt of RM$201.4 billion, which was only known, and later announced, by the preceeding government in May, 2022, (readPFI, 2022).

C) Inevitably, instead of borrowings that incurred interests, a progressive way is to implement a windfall tax on industries that benefit greatly during the Covid-19 crisis, according to Khazanah Research Institute senior advisor Professor Dr Jomo Kwame Sundaram.

“This is precisely the time when you must reform taxes as you have it (windfall tax) all the time amid extraordinarily high petroleum prices or palm oil prices.”

This is concurred by Institute of Malaysian and International Studies research fellow Dr Muhammed Abdul Khalid who pointed out that policy-makers tend to ignore the imposition of capital gains tax when it comes to the issue of tax reform.

Even Bank Negara Malaysia (BNM) assistant governor Dr Norhana Endut noted that the government’s tax collection capacity had not kept pace with the economic growth.

Indeed, Malaysia tax to gross domestic product (GDP) ratio, has been on a steady decline over the medium term. It fell to 12% in 2019 from 15.6% in 2012.

Further, Malaysia’s individual income tax also continued to come from a narrow pool of taxpayers. For instance, in 2018, among a labour force of 15 million people, only 2.5 million were taxpayers!

There is a definite need in expanding the tax base be a priority over the medium term, besides existing tax incentives and exemptions should be reviewed on a regular basis as some of them are outdated and ineffective, affecting the beneficial economic development among the marginalized poor’s.

This is also during an era of inflationary trend. Global inflation is expected to fall to 6.6 percent in 2023 and 4.3 percent in 2024, still above pre-pandemic levels, thus socio-economic impacting heavily on the B40 rakyat².

According to Richard Record, one-time the World Bank Group’s lead economist for Malaysia, the country needs to raise more revenue and spend it more effectively. “Malaysia, of course, benefits from having oil and gas revenues as a source of non-tax revenue, but these have tended to be quite volatile,” he tells The Edge.

Present revenue collection is low mostly because rates are low and there are so many allowances and exemptions. Reforming the SST (Sales and Services Tax), and in particular sharply reducing the number of non-essential items that are zero-rated or exempted from.

Indeed, there should be greater effort across tax instruments: to increase the progressivity of personal income tax, re-examine the number and targeting of corporate income tax incentives and to consider new sources of revenue such as environmental taxation and capital gains taxation.

The introduction of capital gains tax, raising the tax rate for those in the top individual tax bracket and imposing a tax on retirement savings above a certain threshold were among the suggestions on how to enhance revenue in the World Bank Report, 2021.

If the present Government continues to borrowing – the interest rate has to be minimal – then it has to prevent the structure of such debts from becoming too risky. This is because, at one time, we find it cheaper to borrow in US dollars or euros than in our own currency. However, this finanancial method can cause problems if the ringgit depreciates because this increases the real burden of the debt – as was clearly exemplified proportionately in the 1MDB case:

D) Otherwise, it is to apply traditional methods like using Government bonds issued to finance budget deficits but with a glaring pitfall. If there is a continuous growth of debt, the private sector creditors may become concerned about the government’s initiative to repay it. Over time, these creditors will expect higher interest payments to provide a greater return for their increased perceived risk as it is widely acknowledged that higher interest costs dampen economic growth.

On the other hand, for Danaharta it uses cash to purchase loans from the domestic banking system by paying sharp discounts of as much as 50 per cent on a loan that was either collateralised by property or shares listed on the stock exchange.The consequence is too much liquidity in the matket, and the country went south can be partly identified to the solidification of financialisation capitalism (see: Southampton’s Lena Rethel Financialisation and the Malaysian Political Economy.

The flooding of money in the market is not to generate wealth but within the circuit of financialization capitalism components of FIREs (finance, interests, real estate) in furtherance of repaying mortgage loans, hire purchases, insurances, real estates tax dues and other debt interests.(Rajah Rasiah, 2011) has ambly demonstrated that with accentuated and expanded monetary instruments circulation, the national economy had impaired, through wide currency circulation, unfavourably:

E) Inheriting such a burgeoning debt burden, sovereign wealth fund Khazanah Nasional Bhd could sell its assets to raise cash for the state of a nation as she is sitting on assets easily worth more than US$30.5 billion (December 2021) that could probably raise over 10% of the government’s +RM$1.5 trillion debt and contingent liabilities.

Another financial resource lies with Petronas as it is financially in a comfortable position to pay, given that its total assets has strengthened to RM$699.5 billion in the first half of 2022.

Alternatively, government-linked companies (GLCs) and government-linked investment corporations (GLICs) would also likely be encouraged to pay higher dividends. The government could tap these state enterprises to help out just as like the recent RM$58 billion stimulus package to counter impact of the Covid-19 pandemic 2020 crisis.

4] PROGRESSIVE PATHPROCESS

From The Quest for Growth (World Bank, 2016), and to Surge Ahead (World Bank 2021), the country is still, catastrophically, mired and entrapped within capitalism crisis to crisis in a struggle to Catching Up, (World Bank, 2022) among ASEAN peers:

To undertake an emancipatory project may necessarily has to migrate pass through various revolutionary socio-economic phases such the community-based projects of various scopes, scales and dimensions, (see chi-sigma, Towards a Socialist Community with Solidarity Involvement as one such possible undertaking).

To be successful, therefore, requires a commitment to a pulsating socio-economic change that seeks to make itself irreversible through the promotion of an organic system directed at genuine human needs, rooted in substantive equality and the rational regulation of the human social metabolism with nature.

In building an equity society with socialism as the dominant foundation, we must do all we can to develop the productive forces and gradually eliminate poverty, constantly raising the people’s living standards. Only when this outcome is achieved and there is significant prosperity for all will it become possible to begin the shift to advanced stage of an economy that is highly developed and where there is overwhelming material abundance. Only by this process that we shall be able to apply the principle of from each according to his ability, to each according to his needs.

To achieve this process, there is a need on genuine planning and genuine democracy where these are through the constitution of power from the bottom of society. It is only in this way that a progressive socioeconomic society, and its healthy and well-being domain, becomes irreversible.

Towards this process in striving the Socialism with Malaysia characteristics goal, there shall be a combination of planning and markets forming the basic socialist economic system. Second, we need to keep in mind the dialectical relation between ownership and the liberation of the productive forces that shall entail; thus

(1) the system contains a multiplicity of components, but public ownership remains the core economic driver, with corporate capitals supplementing capital formation but without undue surplus value extracted from labour;

(2) while both state owned and private enterprises must be viable, their main objective is not profit at all costs, but social benefit that meets ‘people-centred’ needs from appropriate shelter, education equity to community-base healthcare, adequate nutrient food, harnessing modern technologies towards social needs;

(3) it employs the primary socialist principle of from each according to ability and to each according to work, limiting exploitation and wealth polarisation, and ensuring common prosperity and wealth sharing for every rakyat2 wellbeing;

(4) the primary value should always be ‘socialist collectivism’ – gotong royong community-based than bourgeois individualism and inflicted neoliberalism ethos.

5 CONCLUSION

The emergence of such socialist democratic political practice shall embrace an organic unity of the components of socialist democracy which entails that the people are masters in, and within, the community supervising the servants of society through the socialist rule of law and the Federal institutional guarantees.

We need to be in the threshold of a new sovereignty re-imaging a New Malaysia positioning an entity adhering a New Narrative to perform New Politics for the generasi muda.

This is the moment of great re-imaging of the Malaysia nation and possibly the greatest challenging changes to be seen since independence gained. This is the basic starting point of all planning work and the tasks ahead.

This is that moment of the momentum of a movement.

“Last nail in the coffin” as stated by a prince against a recalcitrant’s Proclamation of Emergency proposal to the King indicates the depth of corporate capital and the width of financialization capitalism stronghold in the country.

Financialization capitalism uses finance tools and instruments in the operations of capitalism (John Bellamy Foster, The Financialization of Accumulation , Monthly Review vol:62, issue 05 October 2010), or simply as the financialization of the accumulation of capital process (Paul Sweezy, More (or Less) on Globalization, Monthly Review 49, no: 4 (September 1997). The defining process of accumulation in financial capital would involve the investment of money or any financial asset to increase the initial monetary value of said asset as a financial return whether in the form of profit, rent, interest, royalties or capital gains.

1] FINANCIALISATION CAPITALISM shifts economic activity from production to the service sector where financial activities generate high private rewards disproportionate to their social productivity (James Tobin, Nobel Prize in Economics 1981). This is one central aspect of surplus value. The surplus value is the added value created by workers in excess of their own labor-cost but being appropriated by the new financial capitalists as profits, (Marx, The Capital, chapter 8). This surplus value is the source of society’s accumulation of fund or investment of fund, part of is re-invested, but part of it appropriated as personal income, and used for consumption purposes by the owners of capital assets. The workers cannot capture this benefit directly because they have no claim to the means of financial creation or its final production.

The country is submerged in financialization capitalism without much current consciousness because it is the “invisible-soft” part in capital accumulation; it’s not Petronas Tower nor swathes of FELDA oil-palms. The initialisation of financialization capitalism started way back in 1983 when Prime Minister Mahathir Mohamad brought forth a privatization policy that represented a drastic reversal of the idealogical New Economic Policy (NEP) and the 1975 Industrial Coordination Act’s industrialization with preferences to an economy resting on capital-market platform (Jomo Sundaram and Tan WooiSyn, Privatization and re-nationalization in Malaysia – a Survey, 2005, an unpublished working paper). It led to the emergence to, and the pervasion of, financialization capitalism in Malaysia. The aftermath of the 1997-1998 financial crisis reinforced the creation of monopoly-finance capitals in advancing IT-geared financial globalization in Malaysia as the engine of financialization capitalism model (LenaRethel, Malaysian Capitalism, Rents, and Financialisation, University of Southampton, 2010).

Many Malay pensioners are nowadays dependent on their ASN and ASB dividends to supplement their pensions; Malay entrepeneurs dependent on these stock holdings to apply for bank loans because any lose in value as a result of a capital market crash following a Declaration of Emergency, these stock collaterals cannot be honoured. There are about 15 million Malays who have invested their savings in ASN, ASB and EPF. Government link investment companies (GLICs) like PNB, Khazanah, Tabung Haji and EPF would likely see their billions of ringgit being wiped out, too.

There are many stakeholders and vested interests.

In the early 1990s, Malaysia corporations typically sought funds from the domestic equity market while non-financial enterprises relied on bank debt and the issuance of bonds abroad. Since 2003, with an unprecedented cachè of RM$190 billion then, the size of Malaysia’s corporate bond market has reached a staggering RM$653 billion at the end of September 2018, which included RM$493 billion worth of sukuk (Sukuk is the Arabic name for financial certificates, also commonly referred to as “sharia compliant” bonds). Since 1999, the total private sector bonds outstanding have surpassed that of public sector bonds (BankNegara, 2007). Bonds expansion in the form of bond finance favors bigger corporations linked to the ethnocratic government – much to the disadvantage of the Chinese and Indian capitals’ small manufacturing enterprises (SMEs) that do not have the sizeable funding resources. Even as such, the increasing demand from the private sector for innovative forms of finance continues to fuel the development of Malaysia’s corporate bond market. Growth has also been spurred by the increasing presence of corporate capital investors, such as pension funds, unit trust funds and insurance companies. The Malaysian corporate debt market has enjoyed enormous growth, rising from MYR 4.1 billion in private debt securities (PDSs) outstanding in 1989 to approximately MYR 188 billion in 2004, an increase of 45 times. In addition, the Malaysian corporate bond market represents 37% of the country’s GDP – by this measure, one of the largest in the world according to an IMF (2005) report. As it were, by 2004, the Malaysian bond market accounted for 8% of the total Asian bond market (excluding Japan).

Under such corporate endowments and environment, capital reconfigures the national society where share ownership and shareholder value take preeminence in a growing influence from the capital market-based financial system. Also, it consolidates the entrenchment of the political renter class power besides polarising the holders of wealth and the earners of income. The explosion of financial innovation and trading gears a neo-liberal economy more towards “speculation” than the engenderment of production to be equally shared by all rakyat (CostaLapavitsas, The financialization of capitalism, SOAS).

2] COVID19,anditsspikes, in an epidemiological and ecological spread has introduced new dimensions to the political economy of nation. The civil disgust and oppositions to leaders seeking political entitlements have only prised open the can of capitalism to display the vagaries of financialization capitalism : the enrichment of political appointees in the non-government companies (GLCs), the extravagance remunerations of non-government organisations (NGOs) board members, and the ruling regime seeking a declaration of Emergency to avoid debating on the 2021 Budget fearing outvoted whereby the PM has to resign; the creation of 5 billionaires within a 6-month lockdown period just as many precarious workers are unemployed, underemployed or seeking employment in the gig economy as drivers for Grab or Shopee; the poorer M40 householders depleting their savings or selling off prematurely their family trust units; the partial operations of small manufacturing enterprises as the Global North monopoly-capital supply chain got disrupted, and some are closing their factories whereas bigger players are strategizing to list overseas from the given government-handout stimuli fund to earn better returns on investment with financialization capitalism model than to rely on a production model.

The pathogens in Covid19 have become much more prevalent in the last decade or so because of the increasing connection between human beings into the remote parts of the world including forests and mountainous caves, which are home to wildlife, particularly wildlife that has held many of these pathogens for thousands of years.

Now through the inexorable expansion of human activity – uncontrolled commercial logging, fossil fuel explorations and exploitations, extension of highways construction, industrial zones opening and urbanisation in general – these wildlife animals carrying pathogenic species have come much closer-in-contact to human beings than ever before.

The onslaught of COVID-19 pandemic, has only accentuated the inter-connection of ecological, epidemiological, and economic vulnerabilities as imposed by monopoly capitalism. This is because the transnational corporation is not only a product but the process of concentration and centralization of capital that had created monopoly capital itself. One need to understand that the accumulation of capital has always meant expansion – commercially and politically. This process of growing and spreading on a global scale has an imperialistic movement characteristics besides the qualitative transformation in the organization and dominance of monopoly capital based on financialization. Concurrently, the wide exploitation of peripheral countries’ natural resources and the comparative advantages derived from global labour arbitrage accentuates this imperial initiative. Through the significant wage differentials between various countries in different geographical regions, monopoly-capital is exploiting the precarious of labour. Monopoly-capital is moving assembly plants from one region to another as fabricators of component parts rather than as a thoroughly manufacturing entity in one location. This restructuring of monopoly capital on a wide-world scale has given contemporary imperialism a new dimensional appearance (Suwandi and Foster, 2016), where the internationalization of capital allows for the substantial control of economy. The result is an enormous expansion of monopoly power, as giant monopolistic and oligopolistic corporations were able to take advantage of low wages, capital shortages, and weak states to leverage their profit margins – and in the process. siphoning massive amounts of surplus from countries in the Global South. The transnational corporation becomes the key instrument of finance capital in the second half of the 20th century, (Magdoff and Sweezy, “Notes on the Multinational Corporation, Part I,” 13; “Notes on the Multinational Corporation, Part II,” 6–7.) especially as most manufacturing production occurs in the periphery and its value is largely captured rather than created in the Global North core.

The financial sector remains a key industry in developed economies, in which it represents a sizable share of the GDP and an important source of highly-skilled employment. Financial services (banking, insurance, leasing, investment, brokerages, real estates) are, and have been, for a long time a powerful sector of the economy in many economically developed countries. Those activities have also played a prime role and significant thrust in facilitating monopoly-capital globalization process. Where there is a widespread international movement of goods, capital, services and technology-induced information, it increases economic integration and interdependence of national, regional, and local economies across the world through an intensification of transborder mobility of such produces and products that the imprint of neo-imperialism is clearly seen everywhere in Global South.

Of course, this whole economic process has to be completed through the intermediation of financial instruments facilitating goods and services (and their associated risks) to be readily exchangeable for currency, and thus make it easier for people to rationalize their assets and income flows.

Financialization capitalism thus emerges in the development of those processes during the period from 1980 to present, in which debt-to-equity ratios increased and financial services accounted for an increasing share of national income relative to other sectors in both the advanced industrial countries as well as Global South economies like Malaysia.

The consequent impact is painful.

3] IMPACT OF FINANCIALISATION CAPITALISM are that suites of investment-capital vehicles introduced to lead the political business class horning on high-end securisation as well as an emergence of a mass investment in Malaysia’s state-led unit trust industry. Deliberating in the thrust of broadening the capital base were corporations targeting the development of capital markets for both debt and equity (Zainaletal, Financial Reform in Malaysia, 1966).

A: State investment vehicles used as conduits in the promotion of financialization capitalism can be seen in such entities like Pernas (Perbadanan Nasional Berhad – the National Corporation set up in 1969) and PNB (Permodalan Nasional Berhad – National Equity Corporation established in 1978), the former to buy Chinese and foreign (mainly British) owned companies, the latter is to transfer shares held by government to individual bumiputera shareholders. PNB become eventually the second biggest institutional investor after state-run Employees Provident Fund (EPF) and has accumulated deposits, by April 2008, of RM120 billion (25% of GNP). Presently, its accumulated fund is RM$267 billion targeting towards RM$350B by 2022; under its stables, PNB holds 48% of Maybank, 52% in Sime Darby, 58% in UMW, 70% in CCM, 66% (Setia) and 59% (MNRB).

B: Then, Financial Disintermediation leading to a new politics of debt with banks lending for private consumption, property and the purchase of securities (Wong Sook Chinget al, Malaysian ‘Bail-out’? Capital Controls, Restructuring and Recovery, Singapore University Press, 2005). There was a vast amount of local surplus that was pitted into the FIRE (finance, investment and real estate) cauldron, just as was evidently present in developed countries, (Foster, The Financialisation of Capitalism, Monthly Review, Vol:58, issue 11, April 2007) to flame the mass financialization mania in a developing country like us in the 1980s.

Indeed, firms were choosing to invest in real estate and other forms of financial assets rather than in productive capital, and would even migrate to other places wherever the unit of labor cost is lower (Lim Mah Hui, Globalization, Export-led growth and inequality: The East Asian Story, South Centre, November 2014). This is an instance when multinational corporations will seek to lower and suppress the wage worldwide and thereby increase their profits by upholding a system of trans-border competitiveness among workers. The eventual consequence is an increase in the rate of workers’ exploitation, globally (seeFoster and McChesney, The Endless Crisis, Monthly Review Press, 2012). The manufacturing sector, which used to be the primary pillar of Malaysia’s economy, would contribute only a quarter to her GDP by 2014; the three-quarters in major economic activities are financialization capitalism-based.

C: Rise of a ‘MASS INVESTMENT CULTURE“. The other key point is that the rise of a ‘mass investment culture’ has strengthened the ‘dominance of finance capital’ (Harmes 2001, Mass investment culture?, New Left Review, 9, pp 103-24), and is a contributing trend in the financialization of capitalism in Malaysia today, too. Take as an example, PNB has also nowadays invests in bonds and structured instruments, thus assisting in the reproduction of a sustainable capital market-based financial system – a collateral vulnerabilities of increasing individual exposure to the capital market whereby inevitably “households had become financialized, too” (CostasLapavitsas, Financialised Capitalism: Crisis and Financial Expropriation, Historical Materialism 17 (2009), School of Oriental and African Studies, London).

In effect, the introduction, and eventual evolution of unit trust investment, on one side – though deviating from NEP redistributive schemes – has on the other hand, turns the capital markets as part of social policymaking, too. By October 2008, the ruling regime borrowed RM$5 billion to shore up the credit-crunch-affected equity market, with the money provided by EPF but disbursed through itself PNB and Khazanah; right-hand-to-left-hand circuit (or circus) of capital.

D: DEBTS whereas in 2005, the ratio of total household debt to GDP amounted to 72.6%, of which nearly 85% was provided by banks (Bank Negara Annual Report 2006), by early 2020, Malaysia’s household debt accounted for 82.7 % of the country’s Nominal GDP as in December 2019, compared with the ratio of 82.0 % in the previous year (data as last extracted on May 13, 2020). Already, between 1999 and 2006, total Malaysian household debt grew at an annualized rate of 15%. From a base in 2000 over RM$160 billion in household debt, this amount had risen over a short period to nearly RM$400 billion by 2006 already.

What is beginning to happen is that compared to the NEP period, between 1970-1980, the bank-based development state model was that the consumption needs of households had been subordinated to the financing needs of the industrial sector as well as the ethnic-based distributive policy, whereas post-economic downturn 1980s had seen private consumption (and thus household borrowing) is increasingly seen as the important driver of domestic growth. This also means that bank lending is much about sustaining consumption than that of capital reproduction.

E: UNEMPLOYMENT becomes a major problem as under a covid19-induced lockdown situation the treble concerning issues are unemployment, underemployment and employment prospects. The present conditions are the perceivable creeping in wage reduction for workers (working at home or 3-day shared shifts) giving raise to household indebtedness (paying interest on mortgages) and higher cost-of-living due to consumption borrowings (mostly by heighten medical fees and charges on pension funds and insurances; and also where depositors are redefined as fee-paying consumers of financial products such as outstanding car and motor-cycle hire-purchase loans and credit cards payment to consumer products besides those supporting a just bought habitat in housing mortgages).

Malaysia’s unemployment, which for the longest time hovered below 4%, spiked to 5% in April and climbed further to 5.3% in May compared with 3.9% in March. This was the highest rate in 30 years since 5.7% in 1989. The official statistics revealed that there were 826,100 unemployed in May, an increase of 6% from 778,800 in April, 2020. In May, 47,000 more people became classified outside the workforce, pushing the total number of Malaysians not actively looking for work to 7.39 million. This is near the highest level, (theedgemarkets.com, 31/07/2020),

That is the hallmark of consumptive financialization capitalism.

F: “INDIVIDUALISATION OF RISKS” assumes an insidious aspect of financialization capitalism when it contributes a high incidence of household debts arising from marketed consumption patterns that by April 2006 the Credit Counseling and Debt Management Agency (AKPK) has to be established as part of the government approach – to develop a personalised debt repayment plan in consultation with financial service providers – to confront the ever increasing consumer debt that was primary affecting many in the Malay community. Unfortunately, AKPK had often portrayed these debtors as “innocent victims of circumstances” or as “hapless” or being “foolish” whereas the main underlying and real reason is that the rising household debt owes too much kleptocratic capitalistic instinct to empower capitalism, and more recently the financialization of capitalism that impoverished precarious workers or those presently out of jobs. Through sophisticated promotions and online direct personalised marketing, more financial instruments to cater holiday loans to time-delay repayments, many borrowers become defaulters during this Covid19-lingering time.

As of March 2016, more than 148,000 borrowers have joined the debt management programme conducted by AKPK (Malaysian Reserve, May 25th. 2016). Since its inception in 2006 and up to Sept 30, 2018, now it is a total of 817,851 individuals attended AKPK’s counselling services and from that, 243,699 participants applied to enrol in its debt management programme. Around 85% of the participants of Agensi Kaunseling dan Pengurusan Kredit’s (AKPK) debt management programme earn less than RM5,000 a month.

G: PUBLIC INTEREST RATES are driven to very low rate to enable such banks to make secure guaranteed profits by lending to their customers and households at higher rates. In short, the financialization of Malaysian capitalism had only encouraged public funds being injected into private and kleptocratic banks of NGOs to boost capital and enlarge capital formation, and further where this public liquidity was to enable these banks to sustain their continuous siphoning operations.

H: SHORE-UP KLEPTOCRATES (not dissimilar to crony capitalism in the early stage of the NEP implementation during the 1970s) that only act as a political behaviour to protect the up-and-coming Malay middle class (Embong, State-led Modernisation and the New Middle Class in Malaysia and the existing Barisan Nasional clique. The mechanism also act as a conduit on preserving the wellbeing of the capital market so as to be used to bail out Malaysian corporations and favoured individual capitalists by likely present ruling regime.

As the state’s role was being transformed to meet the new imperatives of financialization, the kleptocratic governance had to assume as lender of last resort – bailing out crony capitalists like Malaysian Airline System’s Tajudin and Halim Saad’s United Engineers Malaysia (UEM) and the Renong Group (the largest bumiputera-owned conglomerate then) when in August 2001, Syarikat Danasaham – the wholly subsidiary of state-owned investment house Khazanah Nasional – made a conditional voluntary offer to purchase the entire shares and warrants of UEM, including Renong’s stake. What would be the demanding status of MAS or FVG now?

As a sideline, PNB evolution from changing state investment practices to assume increasingly as ‘market players’ where the investment strategy has become more neoliberal following financial considerations on return-oriented basis, there is a competitive stance in maintaining, and retaining, share of the market than that of a distributive expression as articulated within the 1970s’ NEP objectives. It started as a state investment vehicle to strip off government assets for private Bumiputera interest. Using these ill-gotten funds, by 1981 PNB became one of the leading Bumiputera investment institutions acquiring RM$487 million shares in 60-odd companies.

I: HEALTHCARE at time with a pandemic in our midst, the health system in our country mirrors the society’s class structure through control over health institutions and their professions (see an alternative approach: HowardWaitzkin, A Marxist View of Medical Care, Ann Intern Med, August 1978), with increasing financialization capitalism (funded by medical insurance coverage) contributing to the growth of medical centers and involving financial penetration by large corporations like the Sime Darby conglomerate and KPJ Healthcare Berhad, part of Johor Corporation (JCorp) or Perbadanan Johor, and the “medical-industrial complex” (Pharmaniaga Berhad – the largest pharmaceutical company in Malaysia with a paid capital of RM$130 million). In a way, the privatization in health care in the country, with state investment-fund and local Chinese “new money-capitals”, only protect the capitalist economic system and the privatized medical sector with a neoliberalism medical ideology that helps to maintain existing class structure and paternalistic patterns in domination. It is not resolving the Sabah clusters of Covid19 with a community-based approach like in Cuba, and indeed, the deficiency in medical care and health services in Sarawak and Sabah is an economic outcome of the development of underdevelopment.

J: Like FINANCIAL COMPANIES, financialization capitalism in Malaysia has witnessed a business cycle phenomenon where the industrial and commercial enterprises rather than simply look more on bank finance they have taken their own retained profits and begun to behave like financial companies (CostasLapavitsas, The Era of Financialization, Part 3, TripleCrisis). Rather than plowing back profits into investment onto their core businesses, they have instead funding different categories of business. Sime Darby Berhad started as plantation estates, but went into real estates and the construction of medical centers and their management; at one time, it even had a Sime Bank (to finance its real estate owners:). GRAB registered in Singapore, devoted more talents to it’s Big Data enterprise; Top Glove is strategizing its RM$1 billion listing on the Hong Kong stock exchange, the largest by a Malaysian company, when it is flushed with RM$70 billion revenue – more than well-endowed to build new sites or upgrade existing plants without practising financialization capitalism to retain corporate positioning.

Financialization capitalism has facilitated big businesses in the country to become more independent of banks. This is because the less one borrows from the bank, you become more independent. This new business situation encourages banking system to create innovative finance products to entice consumers. The borrowing of funds towards privatization is one area. However, privatization since late 1980s had little evidence in demonstrating that it has enhanced economic growth, but on the other hand, the provision of financialization capitalism has captured new productive capacities where financial resources were diverted to buy over assets from the government at discounted prices, that is, at the expense of the state and the public.

In conclusion, with a neoliberal “growth” policy regime, stressing unshackled profit-making as the driving force in capitalist expansion – and exploitation of Malaysian workers – redirecting an economy towards consumption but with underlying household debts. The continuance of a neo-liberalism economic management shall mean that financialization capitalism would continue to exist, and supranational states with neo-imperialism behavior shall continue to intrude, and eventually penetrate even deeper, into the daily lives of our rakyat2.

EPILOG

Lenin’s theory of imperialism

In 1919 Lenin referred in his “Address to the All-Russia Congress of Communist Organizations of the East” to the global struggle between “all dependent countries” and “international imperialism.” But the real foundations of the broad dependency perspective were first introduced within the Comintern, in its Second Congress in 1920, which included representatives from the periphery (particularly Asia), “Draft Theses on the National and Colonial Questions,” to which the Comintern appended its “Supplementary Theses” on imperialism and underdevelopment.

This theoretical perspective was later expanded upon by Mao Zedong in China in 1926, and in the Sixth Comintern Congress in 1928, which declared—as summarized by the Research Unit for Political Economy—that “colonial forms of capitalist exploitation transfer surplus value to the metropolis and hinder the development of productive forces.”

Similar Third Worldist views were developed after the Second World War at the famous Bandung Conference of 1955, in PaulBaran’s The Political Economy of Growth (1957), and in the 1957 dissertation (later to be published as Accumulation on a World Scale) of Samir Amin, then a young Egyptian scholar studying in France. Dependency theory became closely identified with the Latin American left in the 1960s and ’70s, where there was already a long history of such analysis (notably the work of José Carlos Mariátegui in the 1920s), and where it was heavily influenced by the Cuban Revolution and the ideas of Che Guevara – as well as Andre Gunder Frank’s Capitalism and Underdevelopment in Latin America (1967). Hence, the dependency perspective can be seen as having developed in all three continents of the Global South

As Baran and Sweezy observed: “One can only conclude that foreign investment, far from being an outlet for domestically generated surplus, is a most efficient device for transferring surplus generated abroad to the investing country.”

{ Marx, who in volume 3 of Capital, drafted in the 1860s and 1870s, had marveled already at bankers’ ‘fabulous power’ (1981: 678) vis-a-vis industrial capital }.

At the center of the capitalist economy the tendency to economic stagnation has been increasingly asserting itself since the mid-1970s. This induced repeated attempts to stimulate the system through military spending, with the United States as the engine. This strategy proved to be limited, however, since a big enough boost to the capitalist economy by these means in today’s environment would need to assume the dimension of a world war.

Under these circumstances, as corporations in the 1970s and ’80s sought to hold onto and expand their growing economic surplus in the face of diminishing investment opportunities, they poured their massive surpluses into the financial structure, seeking and obtaining rapid returns from the securitization of all conceivably ascertainable future income streams. Increased concentration (“mergers and acquisitions”) and its attendant new debt, securitizations representing the income stream of already-existing mortgages and consumer debt that piled new debt on old, and new issues of debt and equity that capitalized the potential future monopoly income of patent, copyright, and other intellectual property rights, all followed one another. The financial sector provided every sort of financial instrument that could arguably be serviced by a putative income stream, including from the trading in financial instruments themselves. The result, as Magdoff and Sweezy already documented in the early stages of the process from the late 1970s to the ’90s, was a vast increase in the financial superstructure of the capitalist economy

This financialization of the economy had three major effects. First, it served to further uncouple in space and time—though a complete uncoupling is impossible—the amassing of financial claims of wealth or “asset accumulation” from actual investment, i.e., capital accumulation. This meant that the leading capitalist economies became characterized by a long-term amassing of financial wealth that exceeded the growth of the underlying economy (a phenomenon recently emphasized in a neoclassical vein by ThomasPiketty)—creating a more destabilized capitalist order in the center, manifested in the dramatic rise of debt as a share of GDP. Second, the financialization process became the major basis (together with the revolution in communications and digitalized technology) for a deepening and broadening of commodification throughout the globe, with the center economies no longer constituting to the same extent as before the global centers of industrial production and capital accumulation, but rather relying more and more on their role as the centers of financial control and asset accumulation. This was dependent on the capture of streams of commodity income throughout the world economy, including the increased commodification of other sectors—primarily services that were only partially commodified previously, such as communications, education, and health services. Third, “the financialization of the capital accumulation process,” as Sweezy called it, led to an enormous increase in the fragility of the entire capitalist world economy, which became increasingly prone to asset bubbles that periodically burst, threatening the stability of global capitalism as a whole—most recently in the Great Financial Crisis of 2007–2009. Given its financial ascendancy, the United States is uniquely able to externalize its economic crises on other economies, particularly those of the global South. As YanisVaroufakis notes in The Global Minotaur, “To this day, whenever a crisis looms, capital flees to the greenback. This is exactly why the Crash of 2008 led to a mass inflow of foreign capital to the dollar, even though the crisis had begun on Wall Street.”

The phase of global monopoly-finance capital, tied to the globalization of production and the systematization of imperial rent, has generated a financial oligarchy and a return to dynastic wealth, mostly in the core nations, confronting an increasingly generalized (but also highly segmented) working class worldwide. The leading section of the capitalist class in the core countries now consists of what could be called global rentiers, dependent on the growth of global monopoly-finance capital, and its increasing concentration and centralization. The reproduction of this new imperialist system, as Amin explains in Capitalism in the Age of Globalization, rests on the perpetuation of five monopolies: (1) technological monopoly; (2) financial control of worldwide markets; (3) monopolistic access to the planet’s natural resources; (4) media and communication monopolies; and (5) monopolies over weapons of mass destruction. Behind all of this lie the giant monopolistic firms themselves, with the revenue of the top 500 global private firms currently equal to about 30 percent of world revenue, funneled primarily through the centers of the capitalist system and the core financial markets. As Boron points out with respect to the world’s 200 largest multinational corporations, “96 percent…have their headquarters in only eight countries, are legally registered as incorporated companies of eight countries; and their boards of directors sit in eight countries of metropolitan capital. Less than 2 percent of their boards of directors’ members are non-nationals…. Their reach is global, but their property and their owners have a clear national base.”

The internationalization of production under the regime of giant, multinational corporations thus follows a pattern first explained by Stephen Hymer, and recently underscored by Ernesto Screpatini, who writes that “the great multinational companies” are characterized by “decentralized production but centralized control…. As a consequence the process of expansion of foreign direct investments involves a constant flow of profits from the South to the North, that is, from the Periphery to the Center of the imperial power of multinational capital.”

A 41- year old man from Selangor – on a special Air Asia flight bringing Malaysians and non-citizen family members home from epic centre Wuhan landed in KLIA at 5:57 am Tuesday 4 February 2020 – became the first Malaysiam tested positive for Covid19.

INTRODUCTION

After a local largest cluster linked to a Tablighi Jamaat religious gathering held in Sri Petaling, Kuala Lumpur in late February and early March, leading to massive spikes – then, the largest cumulative number of confirmed COVID-19 infections in Southeast Asia – a nationwide Movement of Control Order (MCO) was promulgated on 16th March 2020, that eventually with the Conditional MCO, also cover the federal territory island of Labuan.

Across the South China Sea, in the month of September 2020, public health experts sounded the alarm that the coronavirus may have begun to reside not only in, but beyond, Sabah where outbreaks initially started at a police lock-up and prison in the east coast, had began to spread to Sarawak, and the rest of the country in peninsular Malaysia.

IN THE BEGINNING

With the intrusion of British colonialism into then Malaya in the 19th. century, the introduction of rubber to Singapore in 1877 via Brazil, Kew Gardens in London and Sri Lanka that within a decade after it was introduced, slash-and-burn local farmers in this part of Southeast Asia planted the Devil’s Milk trees (“dripping from head to foot, from every pore, with blood and dirt” as the most adept in describing the long, grim history of rubber) to become the replacement to their subsistence crops. The tale of how one Henry Wickham purloined Brazil’s rubber patrimony is one of the romantic legends of the British Empire. By his own account, in 1876 Wickham collected over 70,000 hevea seeds from the forests along the Tapajós River. Then, he smuggled the seeds to Joseph Hooker, the eminent botanist who served as director of the Royal Botanic Gardens.

By the 1930s, Malaysia produced half of the world’s rubber. Majority of the Chinese and Indians that live in Malaysia today are descendants of coolie and indenture laborers brought to work on these rubber plantations which were owned by Guthrie, Sime Darby and Golden Hope until they were, in a bout of economic nationalism, taken over in a dawn raid in 1981. They helped transform Malaysia into Britain’s richest colony,whereas in the 1990s, a typical rubber tapper, who spent six hours a day tapping 400 trees, made just about RM$131 a month, and even with the increase of rubber production due to Covid19, 2.25 million people or an average of five people per family, who live off the commodity, these smallholders still live below the poverty line income that was only recently revised from a monthly household income of RM980 to RM2,208.

At times, we wonder whether the country has progress because decades ago, the Guyanese scholar Walter Rodney sketched adroitly How Europe Underdeveloped Africa where human bondage was the driving and animating force of this abject horror in survival.

England had, at one period of time, a 33 percent share of the slave trade in the Caribbean around 1673, and 74 percent by 1683. Of that dreadful total, the Royal African Company, under the thumb of the Crown, held a hefty 90 percent share in 1690.

As scholar William Pettigrew has argued forcefully, the African slave trade rested at the heart of what is still held dear in capitalist societies: free trade, anti-monarchism, and a racially sharpened and class-based democracy.

BIG PLANTATIONS BIG PROBLEMS

The replacement of subsistence crops to plantation-estate type of capitalist agriculture presupposes a division of industrialized town and the rural countryside that inadvertently infertile the soil in the interest of fertilizing producers’ profits. This mode in capitalist production was accompanied by profound ecological degradation. Indeed, Marx had warned that the development of productive forces and technology under capitalist relations of production does not automatically prepare the conditions for human emancipation, but on the contrary, causes a deep alienation of human beings from their environment in the form of a “metabolic rift”, that is, there would be an ecological disruption in their interrelations with nature, (John Bellamy Foster, Marx’s Ecology, New York: Monthly Review Press, 2000).

In a sense, the Big Farms of corporatised agricultural entities enable, through the circuit of capital under late imperialism period of globalization, the etiology of disease via agribusiness. The zoonotic diseases (or zoonoses) such as SARS, MERS, and H1N1 transmitted to humans from nonhuman animals, wild or domesticated; they are assisted by these Big Farms deforestation of virgin terrains to plant commercially high-yielding crops, including durians. Pandemics in the contemporary global economy are connected to the circuits of capital – Global North opening up “commodity corridors” planting coffee trees and soya plants in South America for instances or the palm-oil plantations along the Kalimantan-Sarawak borders as another example that are rapidly changing environmental conditions – a consequential ecological-epidemiological resultant is the imminent propogation of the COVID-19 pandemic.

The dire consequence is that forest disease dynamics, the pathogens’ primeval sources, are no longer restricted to the hinterlands of semi-urban or kampung-kampung villages alone. Their associated epidemiologies have spread across time and into space where every pathogenic SARS carrier bat from Batu Caves could easily leeches on abang or adik in the federal capital of Kuala Lumpur a flight minute away.

More outlooks and outcomes can be found in COVID-19 and Circuits of Capital (by Rob Wallace, Alex Liebman, Luis Fernando Chaves, and Rodrick Wallace) in the May 2020 issue of Monthly Review.

THE ECONOMY

Six plus decades after an independence gained from British colonial master, the country still rests on a neo-liberal economic platform which is supply chaining-latched to transnational corporations that, with the onslaught of the COVID-19 pandemic, has only accentuated the inter-connection of ecological, epidemiological, and economic vulnerabilities as imposed by monopoly capitalism. This is because the transnational corporation is not only a product but the process of concentration and centralization of capital that had created monopoly capital itself. The accumulation of capital has always meant expansion – commercially and politically. This process of growing and spreading, on a global scope and along corporate scale, has an imperialistic in its characteristics besides the rather deep qualitative transformation in the organization and dominance of monopoly capital on the exploitation of peripheral countries’ natural resources and the comparative advantages derived from global labour arbitrage through the continuation of significant wage differentials between various countries in different geographical regions. These binary processes deepen the opening of financialization capitalism in penetrated state-regimes.This restructuring of monopoly capital on a wide-world scale has given contemporary imperialism a new dimensional appearance under emergence of the Covid19 scenario, (Foster and Suwandi, COVID-19 and Catastrophe Capitalism, Commodity Chains and Ecological-Epidemiological-Economic Crises, Monthly Review, June 2020). Now through the inexorable expansion of human activities – commercial logging, fossil fuel exploration, industrial land development, extensive extension in highway construction and urbanisation in general – these wildlife species carrying pathogens have come much closer in contact to human beings.

MALAYSIA has been a place where many, and large, fortunes were amassed. Whereas the majority of businesses built during the prewar period were found in the tin and rubber industries that comprised illustrious family firms built by Low Yat, Loke Yew, Chong Yoke Choy, H.S, Lee, Tan Chay Yan and Lau Pak Khuan who collude with colonial British plantation interests to build their empires, the “new money-capital” entities like YTL Corp’s Yeoh Tiong Lay, Berjaya’s Vincent Tan, Genting’s Lim Goh Tong, Sunway’s Jeffrey Cheah, Lion’s William Cheng and the Ananda Krishnan groups and business stables attempted the forging of more Sino-Indo-Malay corporations, that is, a co-opetition strategy whereby Chinese and Indian capitals can compete as well as co-operate with Malay interests. Those Kuoks, Tehs and Queks were the pioneers in the sugar and palm oil, property and banking sectors during the British Empire, whereas the YTLs’ and Berjayas’ and Annans’ were maintained and retained by transnational connections in the post-independence neo-colonialism period, and the GLCs (government-linked companies) and NGCs (non-government corporations) formulated were sustained with and by various ethnocracy kleptocratic regimes since.

On 18th August 2020, Top Glove Corp Bhd became the second most valuable stock on Bursa Malaysia, having displaced Public Bank Bhd. Now, the gap between Top Glove and the local bourse’s No. 1 spot Malayan Banking Bhd (Maybank) is narrower than ever. At the closing bell on Wednesday, 21st October 2020, Top Glove’s shares gained 4.06 per cent to RM27.14 with 26.13 million units traded, pushing its market capitalisation (market cap) to RM73.47 billion.

Yet at a time of overall national calamity, a convergence of ecological, pandemic and economic proportions, Knight Frank estimates Malaysia capital accumulation of wealth-creation is the 10th fastest in the world – while the mean income was RM$7,901 last year – the firm’s 2020 Wealth Report projects that the number of Malaysians with more than US$30 million will swell by 35 percent between 2019 and 2024, compared with mere 2 per cent between 2018 and 2019. This is happening during a shift in economic activity from manufacturing production to more financial activities – where business focuses on financial transactions and stock-share tradings – that often generate higher private rewards disproportionate to their social productivity according to Nobel Prize economist, James Tobin.

One central aspect of this observed phenomenon lies in the insurgence of financialization capitalism in operation – which primarily embraces finance, insurance and real estate transactions (FIRE) – where the surplus value, that is, the added value created by workers in excess of their own labor-cost is being appropriated by the new financial capitalists as profits, (Marx, The Capital, chapter 8). This surplus value as the source of society’s accumulation of fund or investment of fund, part of is re-invested, but part of it appropriated as personal income, and used for consumption purposes by the owners of capital assets. The workers cannot capture this benefit directly because they have no claim to the means of financial creation or its final production. Firms would likely be choosing to invest in real estate and other forms of financial assets rather than in productive capital, and would even migrate to other places wherever the unit of labour cost is lower (Lim Mah Hui, Globalization, Export-led growth and inequality: The East Asian Story, South Centre, November 2014). This is an instance when transnational corporations, and even indigenous capital, will seek to lower and suppress the wage of labour, and also directly increase their profits by uploading to Global North the capital onto a new company listed overseas or through schemes with transfer pricing elements.

To desert from production when its share price is rising, Top Grove intends to open its second overseas accounts in Hong Kong, besides Singapore, even when its engendered market capitalisation during this year (+RM$70 billion) is profoundly more than enough to upgrade, or build new, production plants, without necessarily seeking for more investors fund, (theedgemarkets.com October 2020). At US$1 billion, Top Glove’s listing would be the biggest ever by a Malaysian company in Hong Kong, according to data compiled by Bloomberg. Meanwhile, the firm has also earmarked RM3 billion for CAPEX to build 450 new lines, creating new capacity of 60 billion pieces of gloves from CY2020 to CY2026.

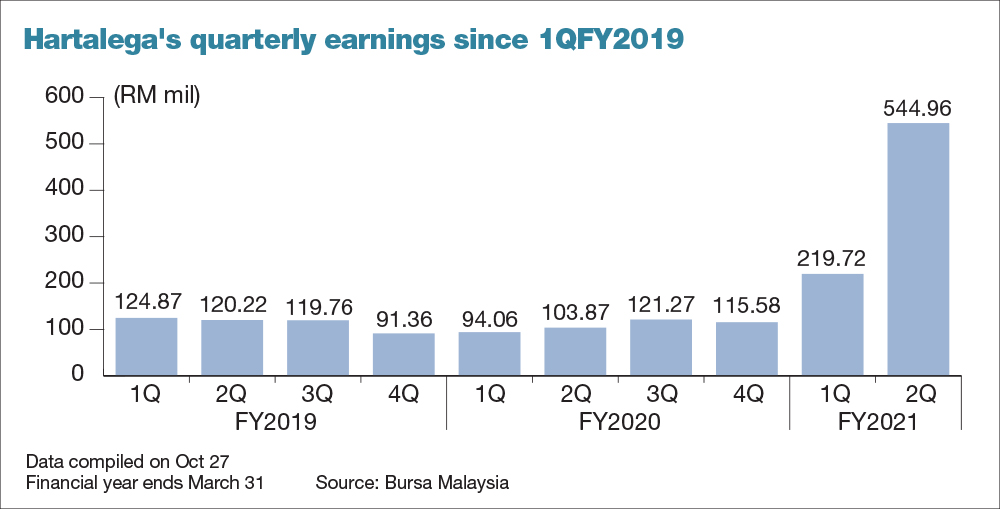

The quantum leap on the quarterly net profits of two glove makers — Hartalega Holdings Bhd and Supermax Corp Bhd — is just eye-popping.

Hartalega’s net profit jumped five times to a record high of RM544.96 million in the second financial quarter ended Sept 30, 2020 (2QFY21) from RM103.87 million a year ago, an evidence of the strongest-ever demand for disposable rubber gloves as a result of the Covid-19 pandemic.