12/02/24

[ The approaches were explored in 2023; additional frameworks, tools and techniques are incorporated herein ]

I] INTRODUCTION

The national revenue is remaining low and structural expenditures are expected to continue remaining high, leading to further narrowing of Malaysia’s fiscal space, especially at a time when the activity in Emerging Markets and Developing Economies (EMDE), excluding China, is forecasted to slow from 3.8 percent in 2022 to 2.7 percent in 2023 on account of weaker external demand and tighter financing conditions.

Indeed, Malaysia’s economy only grew 3.7% in 2023, Bank Negara Malaysia reported, coming in below the target of 4% to 5% due to “prolonged weakness” of external demand. The annual result was far off the 8.7% pace recorded for the previous year, (asia-nikkei, 16th. February 2024; as was concurred by AHAM Capital Malaysia.

Using the ratio of the Federal Government Debt to the revenue collection as a reference point, the World Bank has indicated that Malaysia’s fiscal space has gradually narrowed since 2012 and has had even became tighter post-pandemic.

The current fiscal consolidation strategy – via spending reduction – is, to many national economists and political analysts, rather challenging, given the current tight spending domain. Firstly, the combined spending on structural expenditures is already at high levels; and secondly, other Operating Expenditures components such as supplies and services, and grants and transfers have been on a declining trend or are already at low levels.

Thirdly, whereas interest rate hikes are supposed to stem inflation but given that prices have mainly risen due to supply chain disruptions caused by war, sanctions and pandemic, interest rate increases are likely to trigger more debt crises, much worse than before. Therefore, the government’s current fiscal consolidation plan would have to include a higher revenue collection target.

II] SOURCES OF DEVELOPMENT REVENUE

1) Sovereigns often borrow from within their own countries or from abroad.

Domestic borrowing – from local banks and asset managers or directly from households (EPF employees’ money or PNB owners’ saved trust units) could likely be a steady and reliable source of financing. However, there is a limited amount of money available and repayment maturities tend to be short. Not infrequently, governments also borrow from international capital markets, in larger amounts and usually at longer maturities.

Otherwise, there is a wide and diverse range of private sector entities willing to lend to sovereigns, too. Asset managers, such as pension funds, typically hold a large amount of government debt. They need relatively safe long-term assets to match their long-term liabilities.

2) In Big Projects

typically, such infrastructural undertakings have been financed typically through government budgets, either from tax revenue or from government borrowings; some had often been financed through special-purpose vehicles (SPVs) — for example, DanaInfra, which was set up to raise financing for several infrastructure projects. The debts of these SPVs are guaranteed by the government, and hence, can be considered ultimately as government debt.

It needs to be emphasised that many public infrastructure projects have also been privatised, and the private investors would recover their cost of investment through collecting tolls or charges from the users. Examples of these include the toll roads, independent power producers and land-swap projects. In such cases, the government does not carry any liability for these projects unless it has given some form of revenue guarantees to these private investors. This financing model (using private-sector finance and project development expertise) is known as a public private partnership (PPP) which has various governance and operational issues that at high cost and with dubious efficiency, often increased private profits at the public expense, and as such PPPs have proved costly in financing public projects, (KS Jomo, 24/01/2024).

Not often publicised is another variant of PPP, where private investors recover their cost of investment through payments from the government. This is generally known as a private finance initiative (PFI) which has its many odious transactional issues.

PFI payment obligations comprise a large proportion of the PPP debt of RM$201.4 billion, which was only known, and later announced, by the preceeding government in May, 2022, (read PFI,2022).

3) Inevitably, instead of borrowings that incurred interests, a progressive way is to implement a windfall tax on industries that benefit greatly as during the Covid-19 crisis, according to Khazanah Research Institute senior advisor, Professor Dr Jomo Kwame Sundaram.

“This is precisely the time when you must reform taxes as you have it (windfall tax) all the time amid extraordinarily high petroleum prices or palm oil prices.”

This is concurred by the Institute of Malaysian and International Studies research fellow Dr Muhammed Abdul Khalid who pointed out that policy-makers tend to ignore the imposition of capital gains tax when it comes to the issue of tax reform.

Even former Bank Negara Malaysia (BNM) assistant governor Dr Norhana Endut once noted that the government’s tax collection capacity had not kept pace with the economic growth.

Indeed, Malaysia tax to gross domestic product (GDP) ratio, has been on a steady decline over the medium term. It fell to 12% in 2019 from 15.6% in 2012.

Further, Malaysia’s individual income tax also continued to come from a narrow pool of taxpayers. For instance, in 2018, among a labour force of 15 million people, only 2.5 million were taxpayers!

There is a definite need in expanding the tax base be a priority over the medium term, besides existing tax incentives and exemptions should be reviewed on a regular basis as some of them are outdated and ineffective, affecting the beneficial economic development among the marginalized poor’s.

This is also during an era of inflationary trend. Global inflation is expected to fall to 6.6 percent in 2023 and 4.3 percent in 2024, still above pre-pandemic levels, thus socio-economic impacting heavily on the B40 rakyat².

According to Richard Record, one-time the World Bank Group’s lead economist for Malaysia, the country needs to raise more revenue and spend it more effectively. “Malaysia, of course, benefits from having oil and gas revenues as a source of non-tax revenue, but these have tended to be quite volatile,” he tells The Edge.

Present revenue collection is low mostly because rates are low and there are so many allowances and exemptions. Reforming the SST (Sales and Services Tax), and in particular sharply reducing the number of non-essential items that are zero-rated or exempted from.

Indeed, there should be greater effort across tax instruments: to increase the progressivity of personal income tax, re-examine the number and targeting of corporate income tax incentives and to consider new sources of revenue such as environmental taxation and capital gains taxation.

The introduction of capital gains tax, raising the tax rate for those in the top individual tax bracket and imposing a tax on retirement savings above a certain threshold were already among the suggestions on how to enhance revenue in the World Bank Report, 2021.

If the present Government continues to borrowing – the interest rate has to be minimal – then it has to prevent the structure of such debts from becoming too risky. This is because, at one time, we find it cheaper to borrow in US dollars or euros than in our own currency. However, this finanancial method can cause problems if the ringgit depreciates further because this increases the real burden of the debt – as was clearly exemplified proportionately in the 1MDB case:

4) Otherwise, the nation can try to apply traditional methods like using Government bonds issued to finance budget deficits but with a glaring pitfall. If there is a continuous growth of debt, the private sector creditors may become concerned about the government’s initiative to repay it. Over time, these creditors will expect higher interest payments to provide a greater return for their increased perceived risk as it is widely acknowledged that higher interest costs dampen economic growth.

On the other hand, Danaharta uses cash to purchase loans from the domestic banking system by paying sharp discounts of as much as 50 per cent on a loan that was either collateralised by property or shares listed on the stock exchange. The consequence is too much liquidity in the matket, and the country went south can be partly identified to the solidification of financialisation capitalism (see: Southampton’s Lena Rethel Financialisation and the Malaysian Political Economy; STORM, 2023, deepening neo-imperialism penetration).

Danaharta was a national asset management company. The government established Danaharta with the purpose of removing nonperforming loans (NPL) from the financial system and maximizing their recovery, alongside a recapitalization agency, Danamodal, and a debt restructuring body, the CDRC, to address instability in the financial system.

Over its lifetime, Danaharta’s portfolio totaled RM$52.42 billion in face value of NPLs, and it recovered RM$30.35 billion (58 percent), and recognized a net loss of RM$1.14 billion on RM$8.94 billion total invested. When Danaharta ceased operations in December 2005, the remaining residual assets were transferred to a subsidiary of the Ministry of Finance, Prokhas, for collection.

The flooding of money in the market is not to generate wealth but within the circuit of financialization capitalism components of FIREs (finance, interests, real estate) in furtherance of repaying mortgage loans, hire purchases, insurances, real estates tax dues and other debt interests. In Rajah Rasiah, 2011’s article it has ambly demonstrated that with accentuated and expanded monetary instruments circulation, the national economy had impaired, through wide currency circulation, unfavourably:

5) Inheriting such a burgeoning debt burden,

i} sovereign wealth fund Khazanah Nasional Bhd could sell its assets to raise cash for the state of a nation as she is sitting on assets easily worth more than US$30.5 billion (December 2021) that could probably raise over 10% of the then government’s +RM$1.5 trillion debt and contingent liabilities.

ii} Another financial resource lies with Petronas as it is financially in a comfortable position to pay, given that its total assets has strengthened to RM$699.5 billion in the first half of 2022.

iii} Alternatively, government-linked companies (GLCs) and government-linked investment corporations (GLICs) would also likely be encouraged to pay higher dividends. The government could tap these state enterprises to help out just as like the recent RM$58 billion stimulus package to counter impact of the Covid-19 pandemic 2020 crisis.

6) In light of the ongoing Daim’s wealth investigations, it has been proposed that a Truth, Recovery and Amnesty Commission (TRAC) be formed to diligently track and recover the monies where RM$4.5 trillion, as a frugally conservative estimate of the total (direct + opportunity) economic cost of corruption to Malaysia society.

Through TRAC, those who voluntarily return the monies, holiday mansions, moveable and/or immovable assets etc. can be accorded some form of amnesty from prosecution with some restriction from participating and/or being appointed in public office. For those who choose to go through the investigation and prosecution stage and are eventually found guilty of corruption must be brought to justice while given an option for amnesty upon returning the misappropriated assets. Owing to such an enormity of accumulated losses, the recovered funds would be a great source of government revenues to consolidate our huge budget deficit and recalibrate it for productive use.

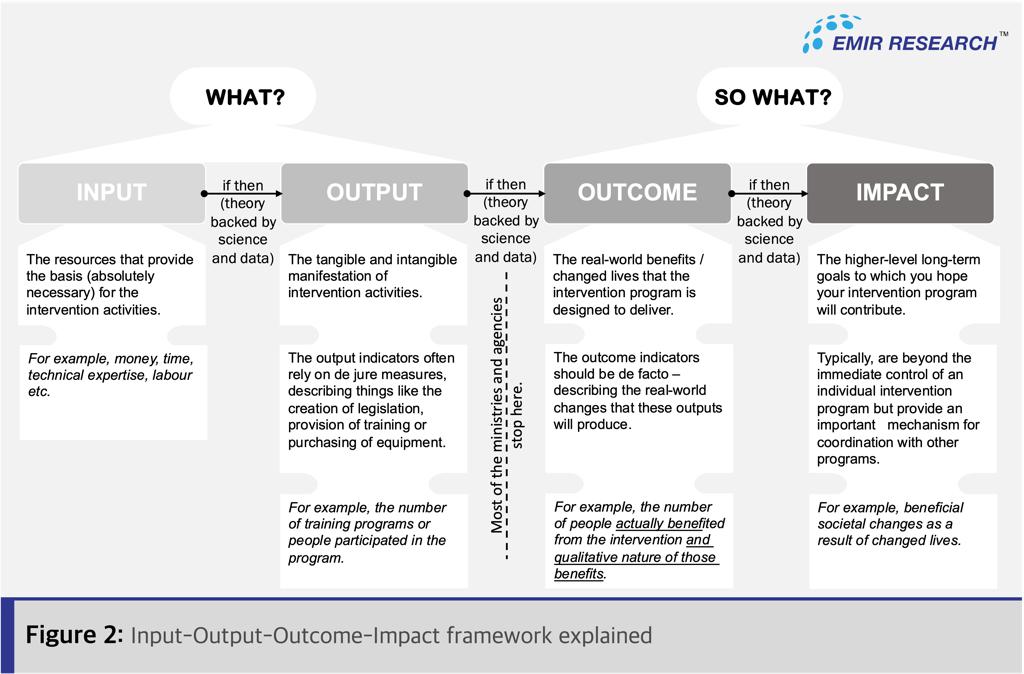

7) Long term, supporting all those tools stated and to be employed, the nation needs to institutionalise the technique of Input-Output-Outcome-Impact (IOOI) framework at every level of decision-making and policy planning — from budget planning to budget execution, thereby “Recalibrating National Budget – Eradicating Leakages and Corruption” and to “Transforming Malaysia from third- to first-world country”, (EMIR Research 2024).

In brief, the IOOI framework is logical and robust reasoning (solely based on data, science and economics) of the entire causal path from inputs (finite resources/capitals) to outputs (tangible and intangible manifestation of intervention activities) to outcomes (real-world benefits/changed lives) and finally to impacts (higher-level intergenerational goals, if we speak in the context of a nation). Importantly, each level comes with a set of metrics to track the progress of transforming inputs into outcomes and impacts; see figure below:

III] CONCLUSION

From The Quest for Growth (World Bank, 2016), and to Surge Ahead (World Bank 2021), the country is still, catastrophically, mired and entrapped within capitalism crisis to crisis in a struggle to Catching Up, (World Bank, 2022) among ASEAN peers:

To undertake an emancipatory project may necessarily has to migrate pass through various revolutionary socio-economic phases such the community-based projects of various scopes, scales and dimensions, (read chi-sigma, Towards a Socialist Community with Solidarity Involvement as one such possible undertaking).

To be successful, therefore,, requires a commitment to a pulsating socio-economic change that seeks to make itself irreversible through the promotion of an organic system directed at genuine human needs, rooted in substantive equality and the rational regulation of the human social metabolism with nature.

In building an equity society with socialism as the dominant foundation, we must do all we can to develop the productive forces and gradually eliminate poverty, constantly raising the people’s living standards. Only when this outcome is achieved and there is significant prosperity for all will it become possible to begin the shift to advanced stage of an economy that is highly developed and where there is overwhelming material abundance. Only by this process that we shall be able to apply the principle of from each according to his ability, to each according to his needs.

RELATED READINGS

Renewal of the Socialist Ideal

You must be logged in to post a comment.